US Economic Resilience Amidst Inflation, Global Risks, and a Data-Dependent Path

The US dollar's future is uncertain, with periods of strength and weakness. Informed Forex traders will navigate the uncertainty and seize opportunities.

Tuesday, August 27, 2024, Week 35

Welcome to this in-depth analysis of the US macroeconomic landscape, tailored specifically for forex traders seeking to understand the forces driving the US dollar. This report provides a comprehensive overview of the key factors shaping the US economy, including the intricate interplay of geopolitics, fiscal policy, economic indicators, and monetary policy.

This week's report focuses on the Federal Reserve's delicate balancing act as it grapples with persistent inflation while aiming to avoid a sharp economic slowdown. We will delve into the latest economic data, including the recent uptick in the unemployment rate and the mixed signals from manufacturing and services PMIs. We will also analyse the implications of the potential for a shift towards a more dovish stance from the Federal Reserve.

Navigating the Global Crosscurrents: Geopolitics and the US Dollar

The geopolitical landscape remains a critical factor for forex traders, as it can significantly impact currency valuations. The previous report highlighted the ongoing conflict in Ukraine, the escalating rivalry between the United States and China, and the potential for a currency board in Libya as key geopolitical risks. Since then, several developments have further complicated the global landscape.

Irpin, Kyiv Oblast, Ukraine -Andrew Petrischev

The war in Ukraine continues to rage, with Russia launching its largest air attack against Ukraine on August 26th, targeting energy infrastructure with over 100 missiles and drones. This escalation underscores the ongoing risk of disruptions to global energy markets and the potential for further sanctions against Russia, which could impact global trade and investment flows.

Tensions between the US and China remain elevated, with both sides taking actions that could further escalate the trade war. The US recently imposed a 100% tariff on Chinese-made electric vehicles, as reported by Bloomberg on August 26th. This move, along with ongoing investigations into European subsidies for dairy products by China, highlights the potential for further trade disruptions and retaliatory measures.

Adding to the geopolitical uncertainty are incidents in the South China Sea, where the Philippines accused a Chinese aircraft of "unsafe manoeuvres" on August 24th. These incidents highlight the ongoing territorial disputes in the region and the potential for escalation, which could disrupt trade routes and impact regional stability.

These geopolitical developments create a complex and uncertain environment for forex traders. The potential for further escalation in any of these areas could trigger risk aversion, leading to a flight to safety and impacting currency valuations.

Geopolitical Risks on the Horizon

In the short-term, market participants are closely monitoring the situation in Ukraine, the US-China trade relationship, and developments in the South China Sea. Any further escalation in these areas could trigger volatility in currency markets.

In the mid-term, the focus will be on the potential for a currency board in Libya, which could disrupt oil production and exports, impacting global energy markets. Additionally, the upcoming US presidential election in November could introduce further uncertainty into the geopolitical landscape, depending on the outcome and the potential for policy shifts.

A Balancing Act: US Fiscal Policy

The US fiscal landscape is characterised by a delicate balancing act between addressing pressing needs and managing a growing budget deficit. The previous report highlighted the Biden administration's significant investments in infrastructure, clean energy, and social programs, which have contributed to a widening deficit. The Fiscal Responsibility Act of 2023, enacted earlier this year, aims to address this issue by enacting roughly $1 trillion in savings over the next decade. However, the long-term sustainability of US public finances remains a concern, particularly as interest rates rise and the cost of servicing the debt increases.

U.S. Capitol Building, Washington, DC, USA -Tim Mossholder

Market traders are closely monitoring the government's spending and revenue projections, as outlined in the US Treasury's budget for fiscal year 2025. The government's ability to address pressing needs while maintaining fiscal discipline will be crucial for ensuring long-term economic stability and maintaining confidence in the US dollar.

A Delicate Balance

In the short-term, the focus will be on the recently released US second-quarter GDP and PCE data. These data provide a comprehensive picture of the US economy's performance in the second quarter and offer insights into the impact of recent fiscal policies.

In the mid-term, the focus will be on the development of the US budget deficit and the government's debt management strategies. Any signs of fiscal slippage or difficulty in financing the deficit could trigger concerns about the sustainability of US public finances and weigh on the US dollar.

The Current State of the US Economy

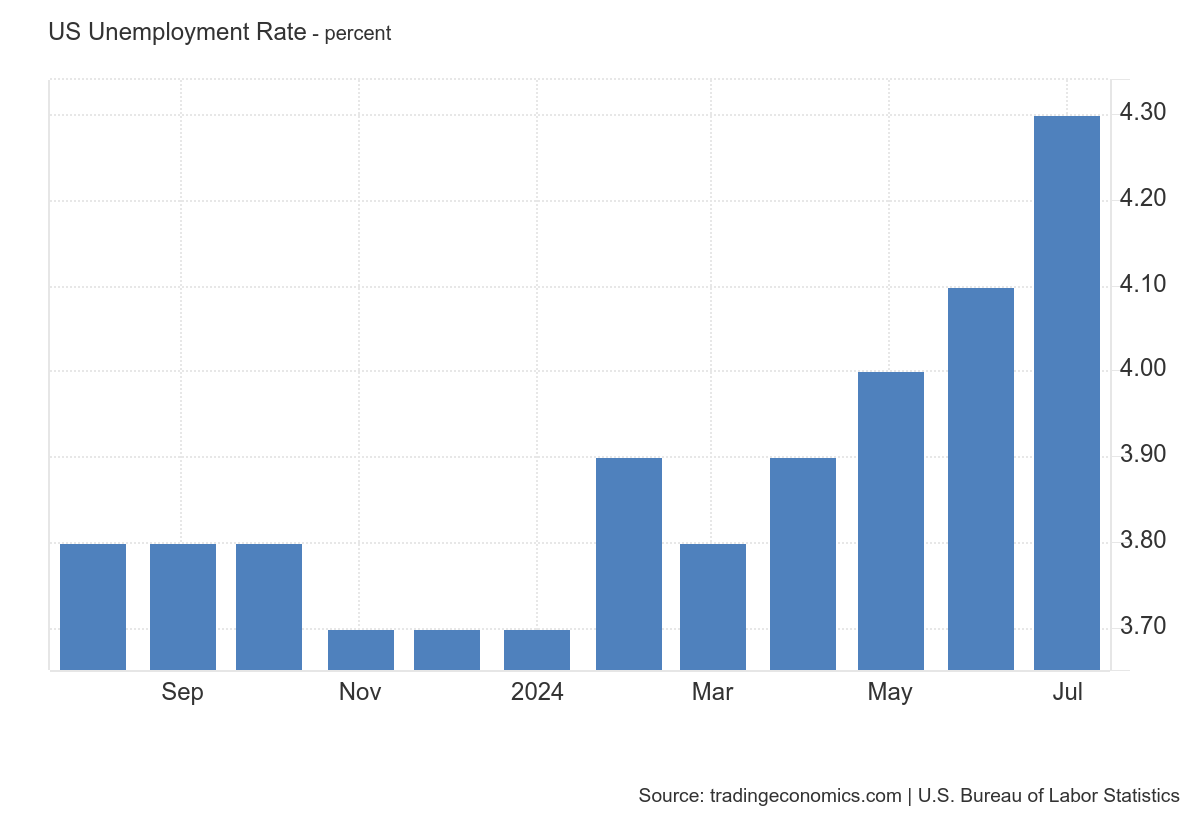

The US economy continues to send mixed signals, with some indicators pointing to continued strength while others suggest a potential slowdown. The labour market, while still robust, is showing signs of cooling, with the unemployment rate ticking up to 4.3% in July. Inflation, while down from its peak, remains stubbornly high, eroding consumer purchasing power. The housing market has cooled significantly, with rising mortgage rates and high home prices weighing on affordability.

Market traders are closely monitoring a range of economic indicators, seeking to gauge the health of the economy and its resilience in the face of multiple headwinds. The recently released US second-quarter GDP and PCE data provide a key update on the economy's performance and offer insights into the potential for a recession.

Economic Outlook

In the short-term, the risks to the economic outlook are tilted to the downside. The lagged impact of the Fed's aggressive tightening cycle could begin to weigh more heavily on economic activity, increasing the risk of a recession. Additionally, persistent inflation could erode consumer confidence and further dampen spending. The release of the US jobs report for August on September 6th will be crucial for gauging the health of the labour market and assessing the risk of a recession.

In the mid-term, the outlook hinges on the Federal Reserve's ability to navigate a delicate balancing act. The central bank needs to bring inflation down to its 2% target without causing a sharp slowdown in economic activity. A soft landing, while challenging, is still possible, but it will require careful monitoring of incoming data and a flexible approach to monetary policy.

The Fed's Tightrope Walk: US Monetary Policy

The Federal Reserve is facing a challenging environment as it seeks to balance its dual mandate of maximising employment and maintaining price stability. Inflation, while down from its peak, remains stubbornly high, prompting the Fed to maintain its restrictive monetary policy stance at its July meeting. However, there are growing expectations for a potential shift towards a more dovish stance in the mid-term, as inflation shows signs of cooling and the labour market begins to moderate.

Chair Powell answers reporters' questions at the FOMC press conference on July 31, 2024.

Chair Powell's recent speech at Jackson Hole provided valuable insights into the Fed's thinking, emphasising a data-dependent approach to policy decisions. Market participants are closely monitoring economic data and Fed communications, seeking to anticipate any shifts in the central bank's stance and their potential impact on financial markets.

In the short-term, the Federal Reserve is expected to maintain its hawkish stance, keeping interest rates elevated until there are clear signs of disinflation. The release of the US jobs report for August on September 6th will be a key data point for the Fed, as it will provide insights into the strength of the labour market and the potential for wage-push inflation.

In the mid-term, the outlook for monetary policy is more uncertain. If inflation continues to cool and the labour market shows further signs of moderation, the Fed could begin to shift towards a more dovish stance, potentially cutting interest rates later in the year. However, it is crucial to emphasise that the timing and magnitude of any rate cuts will be heavily dependent on incoming economic data. As Chair Powell stated at Jackson Hole, "the timing and pace of rate cuts will depend on data, outlook, balance of risks."

A Data-Dependent Path Ahead

The US macroeconomic outlook is currently characterised by a high degree of uncertainty, with the path ahead heavily dependent on incoming economic data and the Federal Reserve's response to those data. While the economy has shown resilience, with solid consumer spending and a robust labour market, persistent inflation and the lagged effects of the Fed's aggressive tightening cycle pose significant risks.

In the near-term, the US economy is expected to continue expanding, albeit at a slower pace. The labour market is likely to remain strong, supporting consumer spending. However, inflation is expected to remain elevated, keeping the Federal Reserve on a hawkish path, at least until there are clear signs of disinflation. The recently released US second-quarter GDP and PCE data provide a key update on the economy's performance and offer insights into the potential for a recession.

In the short-term, the risks to the economic outlook are tilted to the downside. The lagged impact of the Fed's aggressive tightening cycle could begin to weigh more heavily on economic activity, increasing the risk of a recession. Additionally, persistent inflation could erode consumer confidence and further dampen spending. The release of the US jobs report for August on September 6th will be crucial for gauging the health of the labour market and assessing the risk of a recession. This report will be particularly important in light of Chair Powell's comments at Jackson Hole, where he emphasised the importance of the labour market in the Fed's policy decisions.

In the mid-term, the outlook hinges on the Federal Reserve's ability to navigate a delicate balancing act. The central bank needs to bring inflation down to its 2% target without causing a sharp slowdown in economic activity. A soft landing, while challenging, is still possible, but it will require careful monitoring of incoming data and a flexible approach to monetary policy. The development of the trade war between the US and China will also be a key factor to watch, as any further escalation could have significant implications for global trade flows, economic growth, and currency valuations.

Risks to the Outlook

The US macroeconomic outlook faces several potential obstacles. A sharper-than-anticipated slowdown in China, driven by persistent woes in its property sector, could hinder global growth and reduce demand for American exports. The ongoing trade conflict between the US and China could escalate further, disrupting global supply chains, fueling inflation, and discouraging business investment. Furthermore, a resurgence of geopolitical tensions, particularly a direct confrontation between NATO and Russia, could lead to a flight to safety and dampen investor confidence. Additionally, political instability in Argentina poses a risk, as President Javier Milei's intention to veto a pension reform bill, reported on August 23rd, could trigger social unrest and negatively impact the country's economic prospects.

Economic Indicators of the United States

Economic Growth

Gross Domestic Product (GDP): The US economy expanded an annualised 2.8% in Q2 2024, up from 1.4% in Q1. The short-term outlook for GDP growth is uncertain, with the potential for both continued expansion and a downturn. The mid-term outlook is highly dependent on the Federal Reserve's ability to tame inflation without triggering a recession.

Industrial Production: Industrial production in the US fell by 0.6% from the previous month in July of 2024, the most in six months. The short-term outlook for industrial production is weak, with the potential for further declines in the coming months. The next release of Industrial Production data is scheduled for September 17th.

Price Changes (Inflation)

Consumer Price Index (CPI): The annual inflation rate in the US slowed for a fourth consecutive month to 2.9% in July 2024, the lowest since March 2021. The short-term outlook for inflation is uncertain, with the potential for both continued disinflation and a resurgence of inflationary pressures. The next CPI release is scheduled for September 11th.

Producer Price Index (PPI): Factory gate prices in the US increased 0.1% month-over-month in July 2024, following a 0.2% rise in June. The short-term outlook for producer price inflation is uncertain, with the potential for both continued increases and a moderation in price pressures. The next PPI release is scheduled for September 12th.

Core PCE Price Index MoM: The US core PCE price index rose by 0.2% from the previous month in June of 2024, above market expectations of a 0.1% increase. The short-term outlook for core PCE inflation is uncertain, with the potential for both continued increases and a moderation in price pressures. The July PCE data will be released on August 30th.

Labor

Non-Farm Payrolls: Non Farm Payrolls in the United States increased by 114 thousand in July of 2024. The short-term outlook for the labor market is uncertain, with the potential for both continued job growth and a slowdown in hiring. The next Non-Farm Payrolls report is scheduled for September 6th.

Unemployment Rate: Unemployment Rate in the United States increased to 4.30 percent in July from 4.10 percent in June of 2024. The short-term outlook for the unemployment rate is uncertain, with the potential for both continued increases and a stabilisation or decline in the jobless rate. The next Unemployment Rate release is also scheduled for September 6th.

Housing

Building Permits: Building Permits in the United States decreased to 1,396 Thousand in July from 1,454 Thousand in June of 2024. The short-term outlook for the housing market is weak, with the potential for further declines in building permits in the coming months. The next Building Permits release is scheduled for September 17th.

Housing Starts: Housing starts in the United States fell by 6.8% from the previous month to an annualised rate of 1.238 million in July of 2024. The short-term outlook for housing starts is weak, with the potential for further declines in the coming months. The next Housing Starts release is also scheduled for September 17th.

Business Confidence

ISM Manufacturing PMI: The ISM Manufacturing PMI fell to 46.8 in July of 2024 from 48.5 in the previous month. The short-term outlook for manufacturing activity is weak, with the potential for continued contraction in the coming months. The August ISM Manufacturing PMI will be released on September 3rd.

Consumer Sentiment

Michigan Consumer Sentiment: The University of Michigan consumer sentiment for the US rose to 67.8 in August 2024, up from 66.4 in July. The short-term outlook for consumer sentiment is uncertain, with the potential for both continued improvement and a decline in confidence. The final Michigan Consumer Sentiment for August will be released on August 30th.

Trade

Balance of Trade: The trade deficit in the US narrowed to $73.1 billion in June of 2024 from the revised 20-month high of $75.0 billion in the previous month. The short-term outlook for the trade deficit is uncertain, with the potential for both a further narrowing and a widening of the trade gap. The July Balance of Trade data will be released on September 4th.

Conclusion: The US Dollar at a Crossroads

The US economy is at a crossroads, with the potential for both continued expansion and a downturn. The Federal Reserve's data-dependent approach to monetary policy, the government's fiscal policies, and the evolution of the geopolitical landscape will continue to shape the trajectory of the US dollar in the coming months and years.

Key Takeaways for Forex Traders:

August 30th: The release of the July PCE data will provide further insights into the trajectory of inflation and could influence the Fed's decision on the magnitude of a potential rate cut in September.

September 3rd: The August ISM Manufacturing PMI will be released, offering insights into the health of the manufacturing sector.

September 6th: The release of the US jobs report for August will be a key event for gauging the health of the labour market and assessing the risk of a recession.

September 11th: The release of the CPI data for August will provide further insights into the trajectory of inflation.

September 12th: The release of the PPI data for August will offer additional clues about price pressures at the producer level.

The US dollar's path ahead is likely to be volatile, with periods of both strength and weakness. Forex traders who stay informed about key economic indicators, policy decisions, and geopolitical developments will be best positioned to navigate this uncertainty and capitalise on emerging trading opportunities.

Sources

U.S. Bureau of Economic Analysis (BEA)

Federal Reserve

U.S. Census Bureau

Institute for Supply Management (ISM)

National Association of Home Builders (NAHB)

Standard & Poor's

Trading Economics

Newsquawk

Stratfor Worldview