AUD, CAD, JPY: Decoding the Forex Market's Response to Central Bank Moves

Tuesday, 24 September, Week 39

This report provides a comprehensive analysis of three key currency pairs – AUD/USD, USD/CAD, and GBP/JPY – amidst a volatile market environment shaped by central bank policies and economic data releases. Last week saw significant fluctuations, including a risk-on rally sparked by the Federal Reserve’s surprise rate cut, pushing the USD lower and boosting commodity-linked currencies like the AUD. The RBA's decision to hold rates steady at the meeting earlier today, alongside persistent concerns about the global economic outlook and the impact of a slowdown in China, are key factors influencing currency markets.

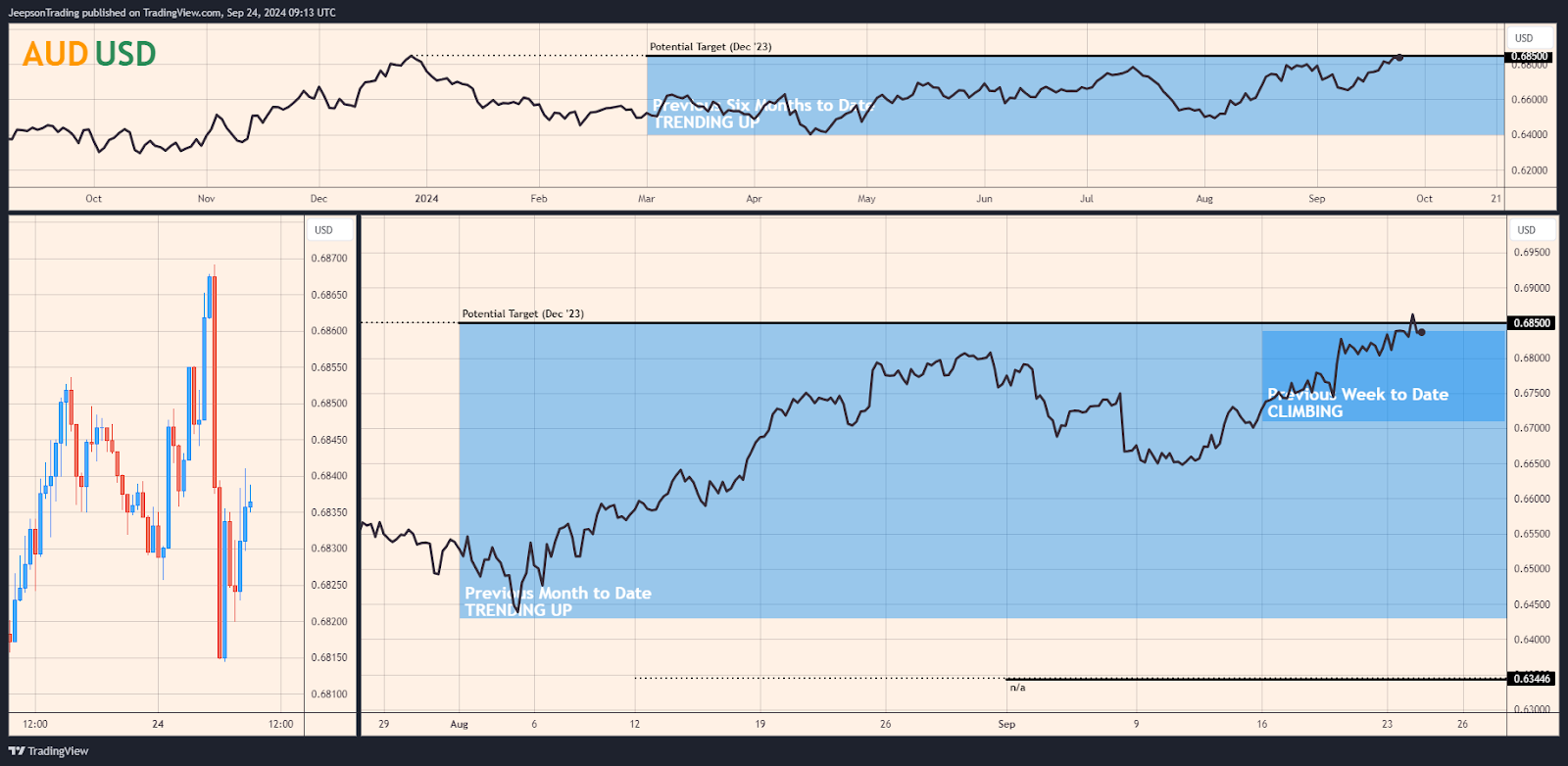

AUD/USD: Aussie Strengthens as RBA Holds Rates Steady

The AUD/USD pair is frequently traded by commodity producers and consumers, hedge funds, and central banks. Fluctuations in iron ore prices, a major Australian export, are a key driver of liquidity in this pair. The AUD/USD pair typically exhibits a positive correlation with iron ore prices, reflecting the demand for this crucial steelmaking ingredient.

The RBA decided to hold the cash rate steady at 4.35% at its meeting on Tuesday, September 24th. While acknowledging persistently high underlying inflation, the central bank's statement suggested a prolonged period of holding rates at current levels. This decision pushed back market expectations for a rate cut to December at the earliest. As a result, the Australian dollar (AUD) appreciated to its highest level of the year, trading above 0.685.

An emerging market theme that could further influence the AUD/USD pair is the impact of China’s slowing economy on Australian exports. The AUD is typically sensitive to Chinese economic data. Continued weakness in Chinese demand for Australian commodities could create headwinds for the AUD/USD pair.

Looking ahead to the upcoming week, the bullish thesis for the AUD/USD pair holds moderate conviction. The continued weakness in the USD, fuelled by expectations of aggressive Fed rate cuts, is likely to provide support for the AUD. The RBA's decision to hold rates steady, while suggesting it is in no rush to cut rates, could be interpreted as a relatively hawkish stance, potentially boosting the AUD/USD pair further in the short term. However, uncertainties surrounding the global economic outlook and the potential for a slowdown in Chinese demand pose significant risks. A continuation of the uptrend throughout the upcoming month, while possible, will depend on the trajectory of these factors.

Conversely, a number of factors could trigger a decline in the AUD/USD pair. Should the USD rebound, driven by stronger-than-expected economic data from the US, this could put downward pressure on the AUD. Additionally, if concerns about China's economic slowdown intensify, it could weigh on the AUD. The bearish thesis for the AUD/USD pair, however, has a low conviction level. Despite the potential for a USD rebound and anxieties about China's economy, the current market dynamics and the AUD’s sensitivity to risk appetite suggest a sustained downtrend is less likely.

Key Indicators / Events to Watch

Wednesday, 25th September, Week 40: Australian CPI Indicator (Australia). The forecast is for a reading of 3.800. An actual reading in line with this forecast would likely have a muted impact, confirming moderating inflation.

Thursday, 3rd October, Week 40: Balance of Trade (Australia). The market anticipates a surplus of AUD 8.20 billion. A larger-than-expected surplus could support the AUD/USD pair.

USD/CAD: Loonie Caught Between Oil's Surge and BoC's Dovish Tilt

The USD/CAD pair is primarily traded by institutional investors, corporations engaged in cross-border trade, and central banks. Oil prices and the interest rate differential between the US and Canada are the key drivers of this pair’s liquidity. The USD/CAD pair typically exhibits an inverse correlation with oil prices.

The dominant market theme influencing the USD/CAD pair is the divergence in monetary policy between the Federal Reserve and the Bank of Canada. The Fed's aggressive move toward easing, with a 50-basis-point rate cut and expectations for further reductions, has pressured the USD. Conversely, the BoC’s more cautious approach to its rate-cutting cycle, stemming from concerns about exceeding its 2% inflation target, has supported the CAD.

Looking ahead to the upcoming week, the bearish thesis for the USD/CAD pair holds moderate conviction. This is based on the potential for further USD weakness amidst ongoing Fed easing, and the BoC's continued caution regarding its rate-cutting cycle. If the USD weakens due to disappointing economic data or a dovish Fed statement, the USDCAD pair is likely to decline, potentially targeting 1.349. The continuation of this bearish trend throughout the upcoming month hinges on the global economic outlook, the Fed's future monetary policy decisions, and the BoC’s stance on interest rates.

The bullish thesis for the USD/CAD pair has a low conviction level. While a potential USD rebound and a more hawkish BoC statement could trigger a correction, these scenarios appear less likely in the upcoming week. The Fed’s commitment to easing and the BoC’s cautious stance, alongside the CAD's sensitivity to oil price movements, suggest a sustained USDCAD uptrend is unlikely in the near term. A continuation of this bullish trend throughout the upcoming month is also unlikely unless these factors shift significantly.

Key Indicators / Events to Watch

Friday, 27th September, Week 39: GDP MoM (JUL) - Canada. The market is forecasting 0.00% growth. A weaker-than-expected GDP figure for July could prompt the BoC to consider easing, pressuring the CAD.

Friday, 27th September, Week 39: GDP MoM Prel (AUG) - Canada. The market expects a 0.10% increase. A weaker-than-expected GDP figure for August would add to anxieties about the pace of Canada’s economic recovery.

Tuesday, 1st October, Week 40: S&P Global Manufacturing PMI (Canada). The consensus forecast is for a reading of 51.5. This would signal expansion in the manufacturing sector.

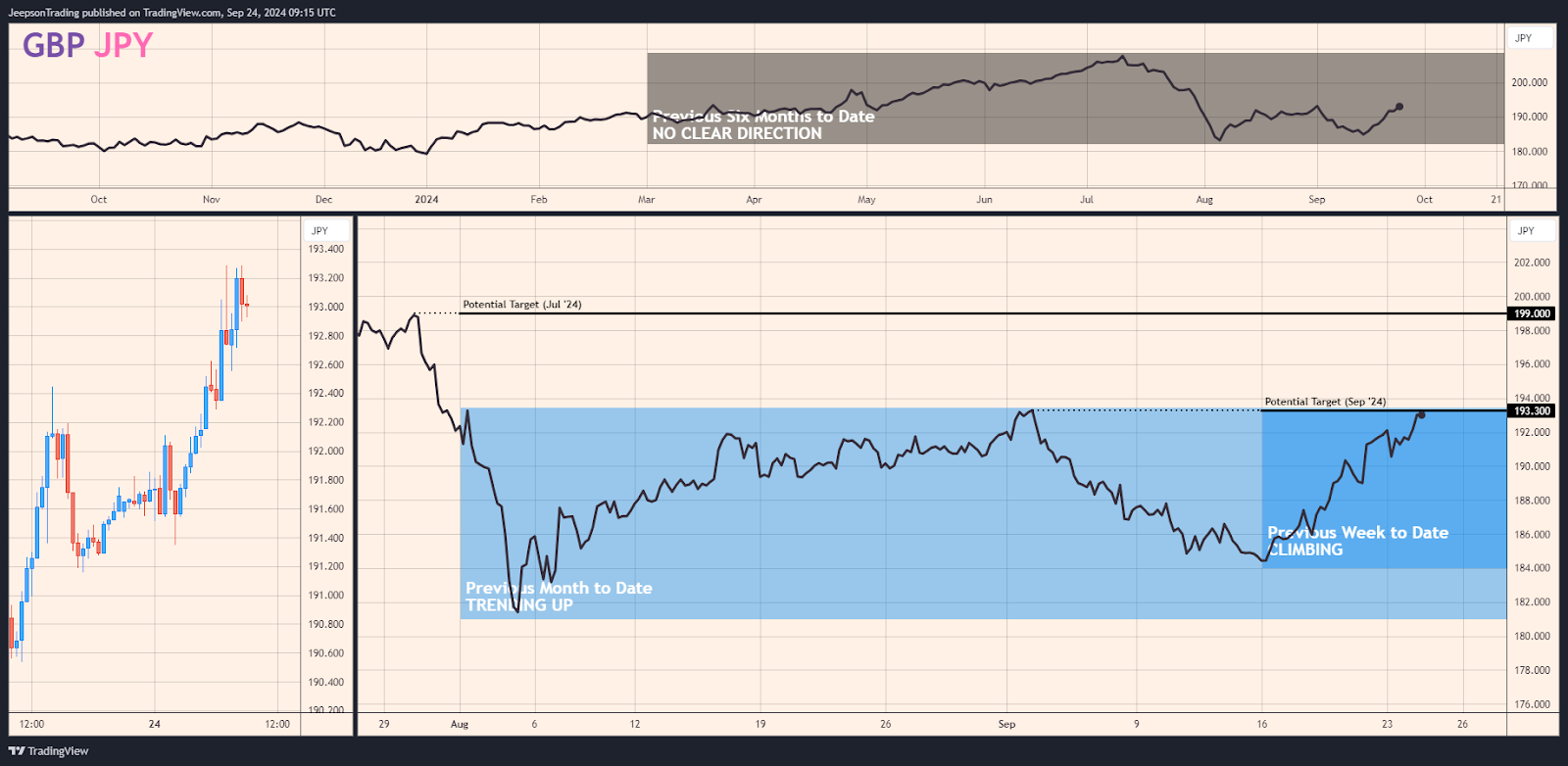

GBP/JPY: Sterling's Climb Amidst BOJ's Policy Dilemma

The GBP/JPY pair is typically traded by carry traders, hedge funds, and institutional investors. This pair's popularity is due to the historically wide interest rate differential between the UK and Japan, making it attractive for carry trades. Shifts in interest rate differentials, along with global risk sentiment, significantly influence the pair’s liquidity. The GBP/JPY pair typically shows a positive correlation with the UK's economic performance and an inverse correlation with safe-haven flows into the JPY.

The dominant market theme influencing the GBP/JPY pair is the divergence in monetary policies between the Bank of England and the Bank of Japan. The BOE's cautious approach to its easing cycle, evident in its decision to hold rates steady at 5%, contrasts sharply with the BOJ’s ultra-loose monetary policy stance. This divergence is widening the interest rate differential.

If the interest rate differential between the UK and Japan widens further, the GBP/JPY pair could see continued upward momentum in the upcoming week. The BOE is expected to maintain its current policy stance. The BOJ’s commitment to ultra-loose monetary policies appears unwavering. Should the BOE signal a hawkish bias, potentially hinting at a rate hike in the coming months, this could further strengthen the GBP against the JPY. This bullish thesis holds a moderate conviction level. However, uncertainties surrounding the BOE's policy trajectory and global risk sentiment could pose risks to the uptrend’s continuation.

A potential decline in the GBP/JPY pair during the upcoming week could be triggered by an unexpected signal from the BOE of a shift towards more aggressive easing. A sudden surge in risk aversion could also trigger safe-haven flows into the JPY. However, the bearish thesis for the GBP/JPY pair has a low conviction level. The current monetary policy divergence and the GBP’s relative strength suggest that a sustained downtrend is less likely in the near term.

Key Indicators / Events to Watch

Thursday, 26th September, Week 39: BoJ Monetary Policy Meeting Minutes (Japan). If the minutes reveal a more hawkish bias, potentially hinting at future rate hikes, this could support the JPY.

Friday, 27th September, Week 39: CBI Distributive Trades (United Kingdom). A negative reading, suggesting a decline in retail sales, could weaken the GBP.

Monday, 30th September, Week 39: Current Account (United Kingdom). A widening deficit could signal weakness in the UK economy.

Conclusion: Central Bank Policies and Economic Data Drive Volatility

The forex market is experiencing heightened volatility influenced by central bank policies and uncertainty about the global economic outlook. The Fed’s easing stance has weakened the USD, impacting major currency pairs. The divergence in monetary policies between the Fed and other central banks creates opportunities for currencies like the AUD and the GBP. However, a potential US recession and geopolitical tensions in the Middle East remain key risks.

Sources

Bloomberg

Stratfor

Financial Juice

Federal Reserve

Bank of England

Reserve Bank of Australia

European Central Bank

Trading Economics

Australian Bureau of Statistics

Office for National Statistics