Aussie Inflation Cools to 3.5%: Is the RBA's Tightening Cycle Bearing Fruit?

July's CPI data revealed decreased inflation, potentially affecting RBA's interest rate decisions?

Wednesday, 28 August, Week 35

Introducing a comprehensive report tailored for forex traders, we delve into the intricacies of Australia's macroeconomic landscape to empower you with the knowledge and insights necessary to navigate the Australian dollar's complexities. This report provides an in-depth analysis of key drivers shaping the Australian economy, covering geopolitics, fiscal policy, economic performance, monetary policy, and future macroeconomic prospects.

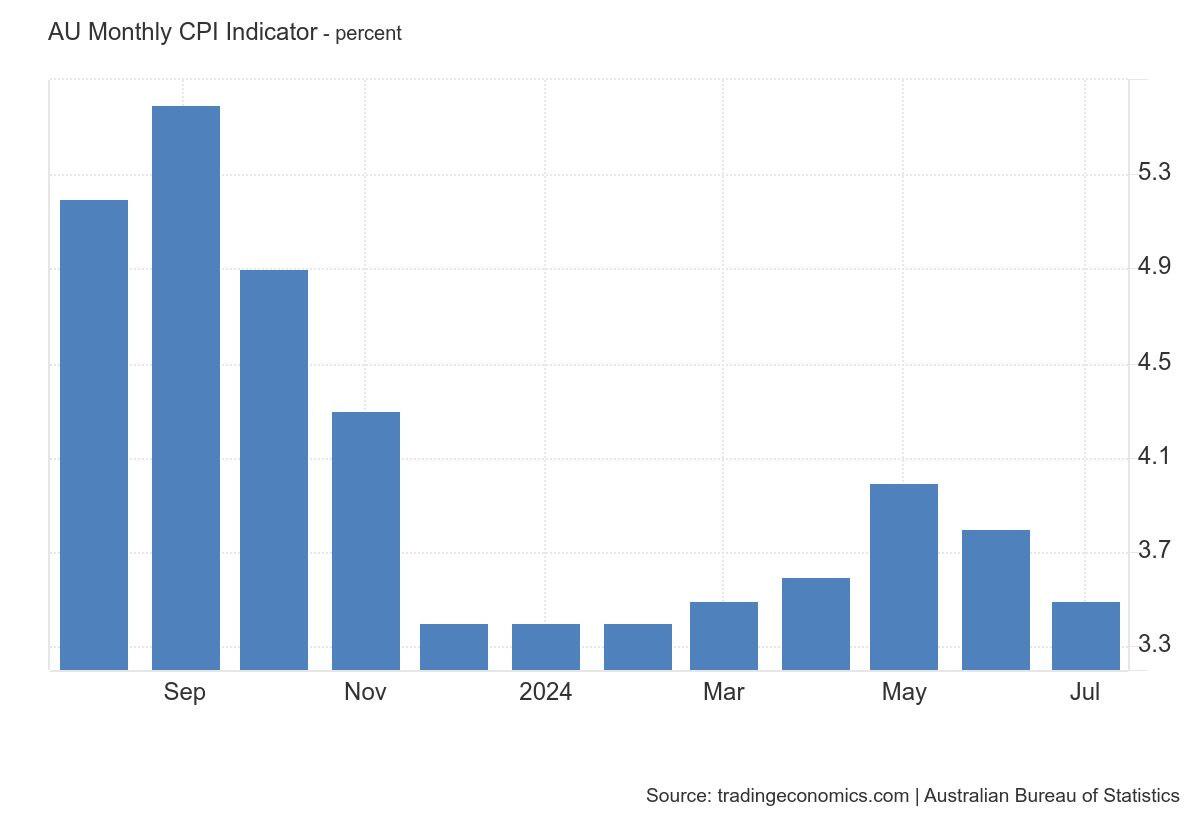

The Australian Bureau of Statistics (ABS) recently released the July Monthly CPI Indicator, revealing a 3.5% year-on-year increase, a slight decrease from 3.8% in June. This marks the lowest inflation reading since March and signifies a faster disinflation pace than anticipated in the previous report. The decline primarily resulted from reduced electricity prices due to new Commonwealth and State rebates. However, food inflation climbed to a three-month high of 3.8%, driven mainly by higher fruit and vegetable prices.

Equipped with this report, forex traders will gain a comprehensive understanding of the factors influencing the Australian dollar, particularly in light of the latest inflation data. This report will assist in making informed trading decisions.

Furthermore, we delve into Australia's fiscal policy balancing act, as the government strives to maintain fiscal discipline while providing targeted support to alleviate cost-of-living pressures and invest in future growth. Additionally, we examine the Reserve Bank of Australia's (RBA) monetary policy stance as the central bank navigates the delicate task of bringing inflation back to target while also supporting economic growth.

This report defines the near-term as a five-day outlook, the short-term as a six-week outlook, the mid-term as a six-month outlook, and the long-term as a five-year outlook.

Australia's Place in a Turbulent World

The previous report highlighted the AUKUS security pact, trade tensions between the West and China, and the persistent threat of Houthi attacks as key geopolitical factors shaping Australia's macroeconomic outlook. Since then, tensions in the Middle East have escalated following the assassination of Hamas' political leader, Ismail Haniyeh, in Tehran on July 31st, prompting fears of Iranian retaliation against Israel and US targets.

BAE Systems rendering of possible design for SSN-AUKUS submarines

The geopolitical landscape is currently dominated by several key narratives that are being closely monitored by market traders:

The escalating conflict between Israel and Iran-backed militant groups: The assassination of Haniyeh has significantly heightened tensions in the Middle East, raising concerns about a potential wider conflict. As Stratfor notes in its August 26th assessment, "Hezbollah's retaliation risks emboldening Israel, portending more violence." The potential for disruptions to global energy supplies and increased geopolitical uncertainty is weighing on investor sentiment, potentially impacting the Australian dollar.

The ongoing trade war between the US and China: This trade war continues to disrupt global supply chains and create uncertainties for Australian businesses. As China is Australia's largest trading partner, any further escalation of tensions could have significant consequences for the Australian economy.

The evolving dynamics of the AUKUS pact: The implementation of the AUKUS pact, particularly the development of nuclear-powered submarines for Australia, is a major focus for the Australian government. The pact is seen as a key element of Australia's strategy to counter China's growing military and economic power in the Indo-Pacific region.

Russia's war in Ukraine: The ongoing conflict in Ukraine continues to have a significant impact on global energy markets and geopolitical stability. The West's continued support for Ukraine and the imposition of sanctions on Russia are likely to further escalate tensions with Moscow.

The rise of far-right extremism in Europe: The recent riots in the United Kingdom highlight the growing threat of far-right extremism in Europe, fueled by anti-immigration sentiment, political polarisation, and disinformation campaigns. This trend poses a risk to social stability and economic growth in Europe, potentially impacting Australia's trade and investment relationships with the region.

Geopolitical Outlook

September 9th: The second US antitrust trial against Google, covering its advertising technology business, is scheduled to begin. The outcome of this trial could have implications for the global technology sector and for Australia's trade and investment relationships with the US.

The US Presidential election in November: A change in administration could lead to shifts in US foreign policy, trade policies, and alliances, with potential ramifications for Australia's economic and strategic interests.

The ongoing development and implementation of the AUKUS pact: The pact is expected to have a significant impact on Australia's defence spending, international relations, and regional security.

The evolution of the trade war between the US and China: Any further escalation of tensions could have significant consequences for the Australian economy.

In conclusion, Australia's geopolitical landscape remains complex and dynamic, with several key narratives shaping the nation's macroeconomic outlook. The escalating conflict between Israel and Iran-backed militant groups, the ongoing trade war between the US and China, the evolving dynamics of the AUKUS pact, and the rise of far-right extremism in Europe are all factors that will continue to influence Australia's economic and strategic interests. Forex traders will need to closely monitor these developments and adjust their strategies accordingly.

Australia's Fiscal Policy Under Scrutiny

The previous report highlighted the Australian government's efforts to balance fiscal discipline with targeted support for households and businesses struggling with the rising cost of living, while also investing in future growth. The 2024-25 Budget, released in May, projected a second consecutive surplus for 2023-24, followed by a deficit of A$28.3 billion in 2024-25.

Australia's fiscal policy is currently focused on delivering on the promises made in the 2024-25 Budget, which includes a range of measures aimed at easing cost-of-living pressures, building more homes, investing in a "Future Made in Australia" plan, and strengthening Medicare and the care economy.

Market traders are closely monitoring the following aspects of Australia's fiscal policy:

The implementation of the cost-of-living relief package: The package includes tax cuts for all taxpayers, energy bill relief for households and businesses, and increases to Commonwealth Rent Assistance. The effectiveness of these measures in providing relief to households and businesses, while also minimising the impact on inflation, will be closely watched.

The government's management of the budget deficit: The projected deficit for 2024-25 is significant, and the government will need to carefully manage spending to ensure that it is targeted at areas that will support sustainable economic growth.

The progress on the "Future Made in Australia" plan: This plan includes a range of initiatives aimed at supporting the transition to a net-zero economy, including investments in renewable energy, critical minerals, and clean manufacturing. The success of this plan will be crucial for Australia's long-term economic prosperity.

The implementation of the National Housing Accord: The Accord aims to deliver 1.2 million new, well-located homes in the five years to 30 June 2029. The progress on this target will be closely watched by market traders, as it will have a significant impact on the housing market and the broader economy.

Fiscal Outlook

In the immediate future, the government's ability to execute its budgetary commitments will be crucial, primarily concerning cost-of-living alleviation, housing, and the "Future Made in Australia" plan. Success in implementing these measures is pivotal to maintaining economic prosperity and stability.

Australia's fiscal policy navigates a complex landscape of competing priorities. The government strives to strike a balance between fiscal prudence and providing relief to households and businesses grappling with escalating living expenses. Simultaneously, strategic investments are made to foster sustainable growth. The dexterity and effectiveness with which this balancing act is achieved will exert a significant influence on Australia's macroeconomic performance in the forthcoming years.

Australia's Economic Landscape

The previous report highlighted Australia's economic resilience amid global challenges, with a focus on moderating inflation, a tight labour market, and a solid pipeline of business investment. However, recent data suggests a more nuanced picture, with disinflation slowing, labour market conditions easing more gradually than anticipated, and concerns about the responsiveness of household consumption to rising incomes.

Australia's economic situation is currently characterised by the following key trends:

Moderating but persistent inflation: Inflation has fallen substantially from its peak in 2022, but remains above the Reserve Bank of Australia's (RBA) target band of 2-3%. The release of the July CPI data today showed a 3.5% year-on-year increase, down from 3.8% in June, indicating a faster pace of disinflation than previously anticipated. The decline was primarily driven by falls in electricity prices, thanks to the introduction of new Commonwealth and State rebates. However, food inflation ticked up to a three-month high of 3.8%, primarily due to higher prices for fruit and vegetables.

A resilient but easing labour market: The labour market remains tight, with the unemployment rate at a historically low level of 4.0%. However, conditions are gradually easing, with the unemployment rate expected to rise to 4.5% by mid-2025. Wages growth remains high, but is expected to moderate somewhat as the labour market eases.

A solid pipeline of business investment: Business investment has withstood the global and domestic pressures, growing by a strong 8.3% last year. The upswing in business investment is expected to continue through to 2025-26 and, if realised, will be the longest sustained increase in business investment since the mining boom.

A tight housing market: The housing market remains tight, resulting in housing prices rising more briskly than expected in recent months and strong growth in advertised rents. This reflects the lack of new housing supply and strong demand. Dwelling investment in early 2024 was weaker than anticipated as high construction costs reportedly made some projects unfeasible and labour shortages remain for certain trades.

Subdued consumer sentiment: Consumer sentiment remains subdued, reflecting ongoing concerns about the cost of living and the economic outlook. However, the recent implementation of the Stage 3 tax cuts and the easing of fears about further interest rate hikes could support a modest improvement in sentiment in the coming months.

Economic Outlook

Future economic performance will be shaped by the evolution of inflation, economic growth, and the labor market in the medium term. The RBA's monetary policy choices will be important in determining economic performance. Traders and investors should pay attention to these areas to predict future policy changes.

Australia's economic outlook is a combination of resilience and uncertainty. The economy faces challenges from global uncertainty and higher interest rates, but it remains fundamentally strong due to a resilient labor market, moderating inflation, and significant business investment. In the coming months, the RBA's monetary policy decisions will be critical in determining economic success. To predict future policy shifts, traders and investors should carefully monitor inflation and economic growth developments.

Decoding Australia's Monetary Policy

The previous report highlighted the RBA's efforts to balance the need to bring inflation back to target with the need to support economic growth. The central bank has embarked on a tightening cycle, raising the cash rate from a record low of 0.1% in May 2022 to its current level of 4.35%. The RBA has signalled that further rate hikes are possible, but the pace and magnitude of increases will depend on the evolution of inflation and economic growth.

The Reserve Bank of Australia Board Room

Australia's monetary policy is currently focused on returning inflation to the RBA's target band of 2-3% over the medium term. The central bank has acknowledged that inflation is proving more persistent than previously anticipated, and has revised its inflation forecasts accordingly. However, the release of the July CPI data today, showing a decline in headline inflation to 3.5%, could potentially influence the RBA's decision-making at its next meeting.

Market traders are closely monitoring the following aspects of Australia's monetary policy:

The RBA's assessment of the current level of the cash rate: The RBA has stated that the current level of the cash rate is restrictive, but it will continue to assess the impact of its previous rate hikes on the economy and inflation.

The RBA's outlook for inflation: The RBA expects inflation to ease gradually over the forecast period as excess demand in the economy declines, but persistent services inflation and a sharp rise in shipping costs pose upside risks.

The RBA's assessment of the labour market: The RBA has acknowledged that the labour market remains tight, but it expects conditions to ease gradually over the forecast period.

The RBA's assessment of global economic developments and risks: The RBA is closely monitoring global economic developments, particularly the actions of other major central banks, for their potential impact on the Australian dollar and financial conditions.

Monetary Policy Outlook

In the short-term, market traders will be focused on the following monetary policy events:

September 24th: The RBA's next monetary policy meeting is scheduled for this date. The market is currently pricing in a high probability of a rate cut at this meeting, but the RBA has stated that it is not ruling anything in or out. The July CPI data, showing a decline in inflation, could potentially influence the RBA's decision at this meeting.

In the mid-term, the key focus will be on the evolution of inflation and economic growth. The RBA is expected to continue raising interest rates gradually over the coming months, but the pace and magnitude of rate hikes will depend on the evolution of inflation and economic growth.

In conclusion, Australia's monetary policy is at a crossroads as the RBA seeks to balance the need to bring inflation back to target with the need to support economic growth. The central bank's actions are being closely watched by market traders, who are eager to anticipate future policy changes and their potential impact on the Australian dollar.

Navigating the Uncertain Waters: Australia's Macroeconomic Outlook

The previous report highlighted a mix of resilience and uncertainty in Australia's macroeconomic outlook, with moderate economic growth, gradually easing inflation, and a labour market moving towards a more balanced state. However, persistent inflation, a sharper-than-expected slowdown in global growth, and a renewed downturn in the Chinese economy were identified as key risks.

Australia's macroeconomic outlook is currently characterised by a delicate balancing act between supporting economic growth and controlling inflation. The RBA's recent decision to hold the cash rate steady, while acknowledging persistent inflationary pressures, highlights this challenge. The release of the July CPI data today, showing a decline in headline inflation, provides some optimism for the outlook, but the RBA will likely remain cautious in its approach to monetary policy.

Market traders are closely monitoring the following factors that could shape Australia's macroeconomic outlook:

The trajectory of inflation: The July CPI data, showing a decline in inflation to 3.5%, is a positive development for the outlook. However, the RBA will be watching closely for signs of persistent inflation in the coming months, particularly in services prices.

The pace of global economic growth: A sharper-than-expected slowdown in global growth, particularly in China, could weigh on Australian exports and commodity prices, dampening economic activity.

The evolution of the labour market: The RBA is closely watching the labour market for signs of easing, which would support a moderation in wages growth and reduce inflationary pressures.

The government's fiscal policy: The government's fiscal policy settings, particularly in relation to spending and taxation, will also play a role in shaping the macroeconomic outlook.

The immediate focus is on the reaction of financial markets to the July CPI data. The data could potentially influence the RBA's decision on interest rates at its next meeting in September.

The short-term outlook is for continued moderate economic growth, with GDP growth projected at 0.9% in the June quarter and 1.7% in the September quarter. Inflation is expected to continue easing, with the July CPI data providing some optimism for the outlook. The labour market is expected to continue easing gradually, with the unemployment rate forecast to rise to 4.3% by the end of the year.

The mid-term outlook is for a gradual recovery in economic growth, with GDP growth projected to pick up to 2.6% in the year to mid-2025. Inflation is expected to continue easing, with underlying inflation forecast to fall below 3% by late 2025 and approach the midpoint of the RBA's target band in 2026. The labour market is expected to remain somewhat tight over much of the forecast period, with the unemployment rate forecast to stabilise around 4.5% by mid-2026.

Risks to the Outlook:

Persistent inflation: If inflation proves to be more persistent than expected, the RBA may need to raise interest rates further, potentially weighing on economic growth.

Global economic slowdown: A sharper-than-expected slowdown in global growth, particularly in China, could weigh on Australian exports and commodity prices, dampening economic activity.

Renewed downturn in China: A renewed downturn in the Chinese economy, particularly in the property sector, could have a significant impact on the Australian economy, given China's importance as a trading partner.

In conclusion, Australia's macroeconomic outlook is for continued moderate economic growth, gradually easing inflation, and a labour market that is moving towards a more balanced state. However, several risks could derail this outlook, and traders and investors will need to closely monitor developments in inflation, economic growth, and global economic conditions to assess the likelihood of these risks materialising.

Economic Indicators of Australia: A Trader's Guide

Economic Growth:

GDP Growth Rate: The Australian economy expanded by 0.1% in the first quarter of 2024, marking the slowest pace of growth in six quarters. Growth is expected to remain subdued in the short-term, with forecasts of 0.3% for the second quarter and 0.6% for the third quarter. However, the mid-term outlook is for a gradual recovery in growth, with forecasts of 1.9% for the year to mid-2025 and 2.5% for 2025.

Construction Work Done: Total construction work done in Australia shrank by 2.9% in the first quarter of 2024, marking the sharpest decline since the second quarter of 2019. Construction activity is expected to remain subdued in the short-term, reflecting ongoing cost pressures and labour shortages. However, the mid-term outlook is for a gradual recovery in construction activity, supported by the large pipeline of infrastructure work and the government's investment in the "Future Made in Australia" plan.

Price Changes (Inflation):

CPI Inflation Rate: Australia's inflation rate eased to 3.5% in July 2024, down from 3.8% in June. This is the lowest reading since March and suggests that the pace of disinflation is accelerating. The decline was driven by falls in electricity prices, thanks to the introduction of new Commonwealth and State rebates. However, food inflation ticked up to a three-month high of 3.8%, primarily due to higher prices for fruit and vegetables. In the short-term, inflation is expected to remain elevated, but the July CPI data provides some optimism for a faster return to the RBA's target band. In the mid-term, inflation is forecast to continue easing, with underlying inflation expected to fall below 3% by late 2025 and approach the midpoint of the RBA's target band in 2026.

Trimmed Mean Inflation Rate: The trimmed mean measure of core inflation in Australia slowed to 3.7% in July 2024, down from 4.0% in June. This is the lowest reading since January 2022 and suggests that underlying inflationary pressures are moderating. In the short-term and mid-term, trimmed mean inflation is expected to continue easing gradually, reflecting the RBA's expectation that underlying inflationary pressures are moderating.

Labour:

Employment Change: Employment in Australia increased by 58.2 thousand in July of 2024, marking the largest growth in employment levels since February. Employment growth is expected to moderate in the short-term, reflecting the softening in the leading indicators of labour demand. However, the mid-term outlook is for continued employment growth, albeit at a slower pace, as the economy recovers.

Unemployment Rate: Australia's seasonally adjusted unemployment rate ticked up to 4.2% in July 2024, marking the highest jobless rate since January 2022. The unemployment rate is expected to continue rising gradually over the short-term and mid-term, reflecting the RBA's expectation that the labour market will continue to ease.

Housing:

Building Permits: The seasonally adjusted estimate for total dwellings approved in Australia plunged by 6.5% in June 2024, marking the second time of drop year to date in building permits and the steepest pace since December 2023. Building approvals are expected to remain subdued in the short-term, reflecting material and labour shortages, high construction costs, and elevated interest rates. However, the mid-term outlook is for a gradual recovery in building approvals, supported by the government's investment in housing and infrastructure.

Housing Credit: Housing credit in Australia rose by 0.4% in June 2024, matching market expectations. Housing credit growth is expected to remain moderate in the short-term, reflecting the impact of higher interest rates on borrowing. However, the mid-term outlook is for a gradual pick-up in housing credit growth, supported by the expected recovery in household incomes and the easing of affordability constraints.

Business Confidence:

NAB Business Confidence Index: Australia's NAB business confidence index dropped to 1 in July 2024 from a downwardly revised 3 in the previous month. Business confidence is expected to remain subdued in the short-term, reflecting ongoing uncertainty about the economic outlook. However, the mid-term outlook is for a gradual improvement in business confidence, as inflation eases and economic growth picks up.

Consumer Sentiment:

Westpac-Melbourne Institute Consumer Sentiment Index: The Westpac-Melbourne Institute Consumer Sentiment index in Australia increased to 85.0 in August, the highest in six months, from 82.7 in July of 2024. Consumer sentiment is expected to remain relatively stable in the short-term, supported by the government's cost-of-living relief measures and the easing of fears about further interest rate hikes. However, the mid-term outlook for consumer sentiment is uncertain, as it will depend on the evolution of inflation, economic growth, and the labour market.

Trade:

Balance of Trade: Australia recorded a trade surplus of AUD 5.589 billion in June of 2024. The trade surplus is expected to remain strong in the short-term, supported by robust demand for Australian exports. However, the mid-term outlook for the trade surplus is uncertain, as it will depend on the evolution of global economic growth and commodity prices.

Key Takeaways for Forex Traders

The July CPI data, released today, showed a decline in inflation to 3.5%, providing some optimism for the outlook. This could potentially influence the RBA's decision on interest rates at its next meeting on September 24th.

The Australian economy is expected to continue growing, albeit at a moderate pace, supported by a resilient labour market, moderating inflation, and a solid pipeline of business investment. However, several risks could derail this outlook, including persistent inflation, a sharper-than-expected slowdown in global growth, and a renewed downturn in the Chinese economy.

The Australian dollar is currently trading within the range observed since 2022. The currency has been volatile in recent months, reflecting changing expectations of policy tightening by the Bank of Japan and a decline in some key commodity prices.

In conclusion, the Australian dollar is likely to remain volatile in the near term as the RBA continues to assess the impact of its monetary policy decisions and as global economic conditions evolve. Forex traders will need to closely monitor developments in inflation, economic growth, and global risk sentiment to make informed trading decisions.

Sources

Australian Bureau of Statistics

Reserve Bank of Australia

Australian Government

Trading Economics

Westpac Banking Corporation

Melbourne Institute

National Australia Bank

S&P Global

Australian Industry Group

CoreLogic

Stratfor