Budget Jitters, Inflation Fears, and Election Risks

Wednesday, October 16, 2024 (Week 42)

Forex traders are currently focused on a confluence of crucial narratives impacting currency markets. This past week (October 6th-15th), persistent US inflation concerns, fueled by hotter-than-expected CPI data, and anxieties surrounding the upcoming UK Autumn Budget have taken centre stage. Adding to the complexity, the escalating conflict in the Middle East and the potential for further disruptions to global energy markets are driving safe-haven flows and influencing central bank policy expectations. These intertwined narratives have significantly contributed to recent forex market volatility. This report provides an in-depth analysis of the dominant and emerging themes impacting four major currency pairs, offering valuable insights for forex traders navigating this dynamic environment.

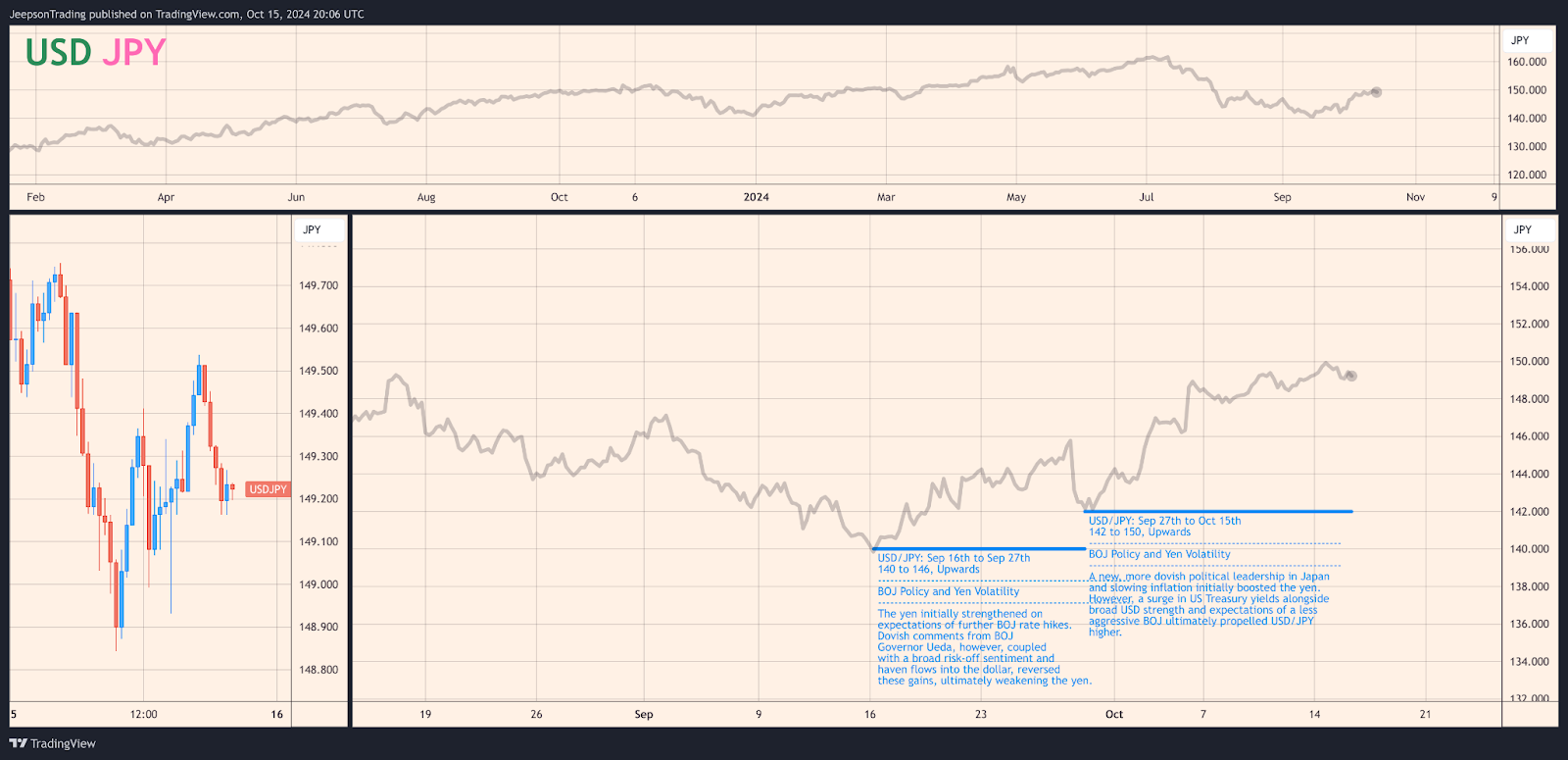

USD/JPY: Yen Under Pressure

USD/JPY trading is dominated by institutional investors, central banks, and corporations, with retail traders also participating. Liquidity stems from Japan's economic size and its role in global trade. USD/JPY typically shows an inverse correlation with US Treasury yields. The October 8th COT report indicates Asset Managers/Institutions are net short JPY, suggesting bearish sentiment.

The dominant theme shaping USD/JPY is the interplay between the BOJ's hawkish bias and the yen's haven status. Mixed Japanese economic data creates uncertainty. Market narratives revolve around the BOJ’s challenge: managing above-target inflation while mitigating the strong yen's impact on exports.

Bullish Thesis (Upcoming Week): Moderate Conviction. USD/JPY could test 150.000 if geopolitical tensions escalate. Upcoming US retail sales data (Oct 17th) could add to volatility. A stronger-than-expected report would likely reinforce the USD's strength.

Bearish Thesis (Upcoming Week): Low Conviction. De-escalation in the Middle East could weaken USD, potentially pushing USD/JPY lower. However, the overall risk-off environment limits downside potential.

What to Watch:

USD: Retail Sales MoM (Oct 17th), forecast 0.3%; Initial Jobless Claims (Oct 17th), forecast 241K; Philadelphia Fed Manufacturing Index (Oct 17th), forecast 3

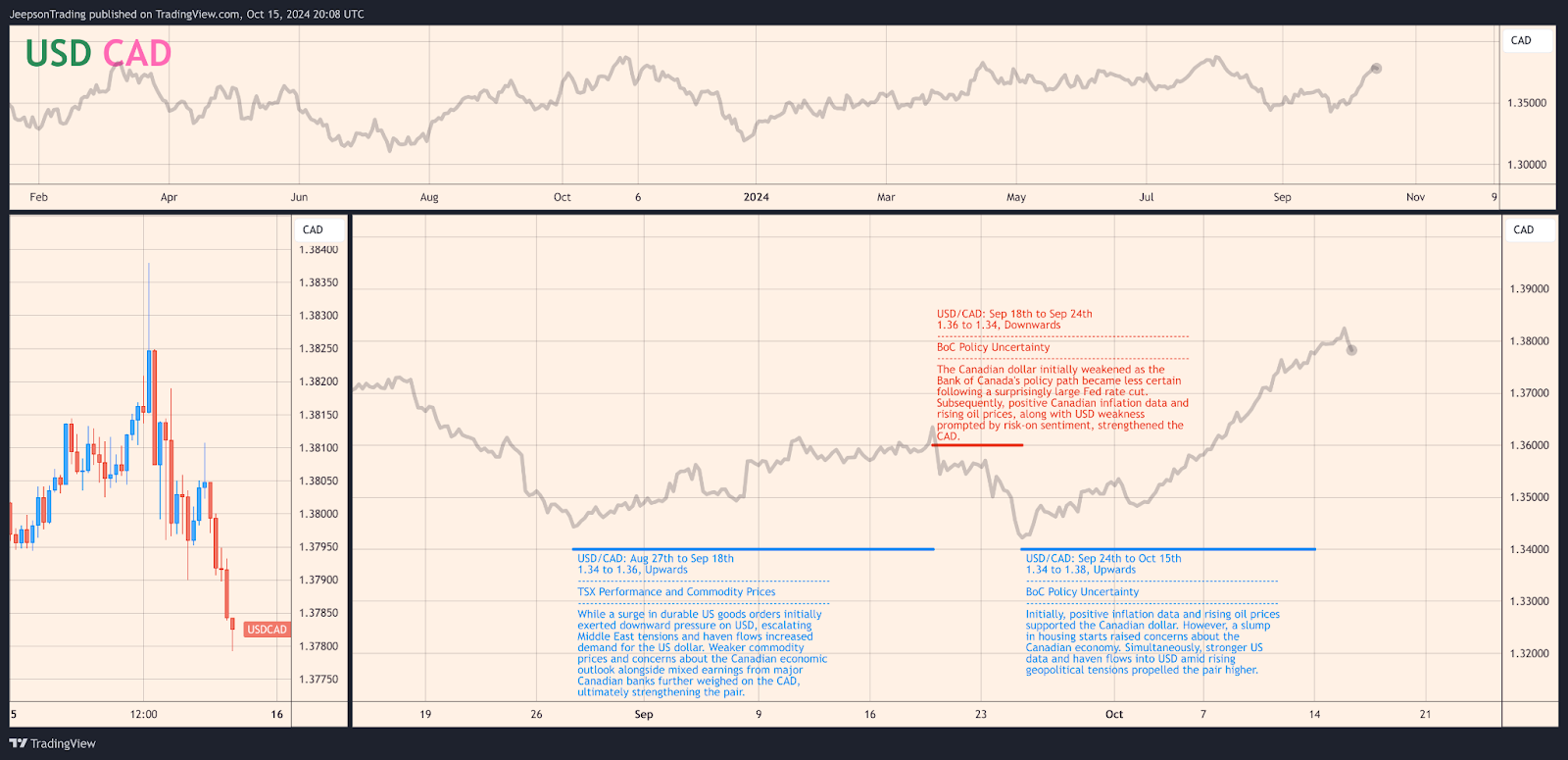

USD/CAD: Loonie's Tightrope Walk

Oil prices, Canadian economic data, and the TSX's performance heavily influence the actively traded USD/CAD pair. Participants include institutions, corporations, hedging, and retail traders. Canada’s oil exports drive liquidity. The latest COT report (October 8th) indicates a net short CAD position by Leveraged Funds, reflecting a bearish sentiment.

The dominant theme impacting USD/CAD remains the interplay between the TSX's performance and fluctuations in oil prices, alongside an emerging theme of BoC policy uncertainty. While the TSX's record highs typically boost CAD, the uncertain pace of the BoC's easing cycle compared to the Fed's rate cuts creates headwinds.

Bullish Thesis (Upcoming Week): Moderate Conviction. USD/CAD could climb toward 1.390 should upcoming US economic data, particularly retail sales (October 17th), surprise to the upside, suggesting a stronger US economy and potentially limiting the extent of future Fed easing.

Bearish Thesis (Upcoming Week): Low Conviction. Weaker US data could trigger some profit-taking in USD/CAD longs, potentially pushing the pair lower. However, uncertainty surrounding the upcoming Canadian inflation report (October 15th) and the potential for an escalation of geopolitical risks remain upside risks.

What to Watch:

USD: Retail Sales MoM (Oct 17th), forecast 0.3%; Initial Jobless Claims (Oct 17th), forecast 241K; Philadelphia Fed Manufacturing Index (Oct 17th), forecast 3

CAD: Inflation Rate YoY (Sep), forecast 2.1% (Tuesday); Housing Starts (Sep), forecast 235K (Wednesday); BoC Interest Rate Decision (Wednesday)

GBP/USD: Autumn Budget Looms Large

GBP/USD is heavily traded given the UK and US are major financial hubs. Liquidity is robust. UK gilt yields often exhibit an inverse relationship with the pair. The October 8th COT report shows Asset Managers/Institutions holding a large net short GBP position, suggesting bearish sentiment, however fewer Leveraged Funds hold a net short position.

UK economic uncertainty dominates GBP/USD, fueled by mixed economic signals, Brexit’s continued impact, and an unclear BoE policy path. The upcoming Autumn Budget (October 30th) adds significant uncertainty.

Bullish Thesis (Upcoming Week): Low Conviction. GBP/USD could strengthen if UK inflation data (October 16th) surprises to the upside. However, uncertainty around the Autumn Budget (Oct 30th) limits potential gains.

Bearish Thesis (Upcoming Week): Moderate Conviction. A disappointing Autumn Budget or stronger US data could pressure GBP/USD lower. Escalating geopolitical tensions would further weigh on the pound.

What to Watch:

GBP: Inflation Rate YoY (Wed, Oct 16th, Week 42), forecast 1.9%; Retail Sales MoM (Fri, Oct 18th, Week 42), forecast -0.3%

USD: Retail Sales MoM (Oct 17th), forecast 0.3%; Initial Jobless Claims (Oct 17th), forecast 241K; Philadelphia Fed Manufacturing Index (Oct 17th), forecast 3

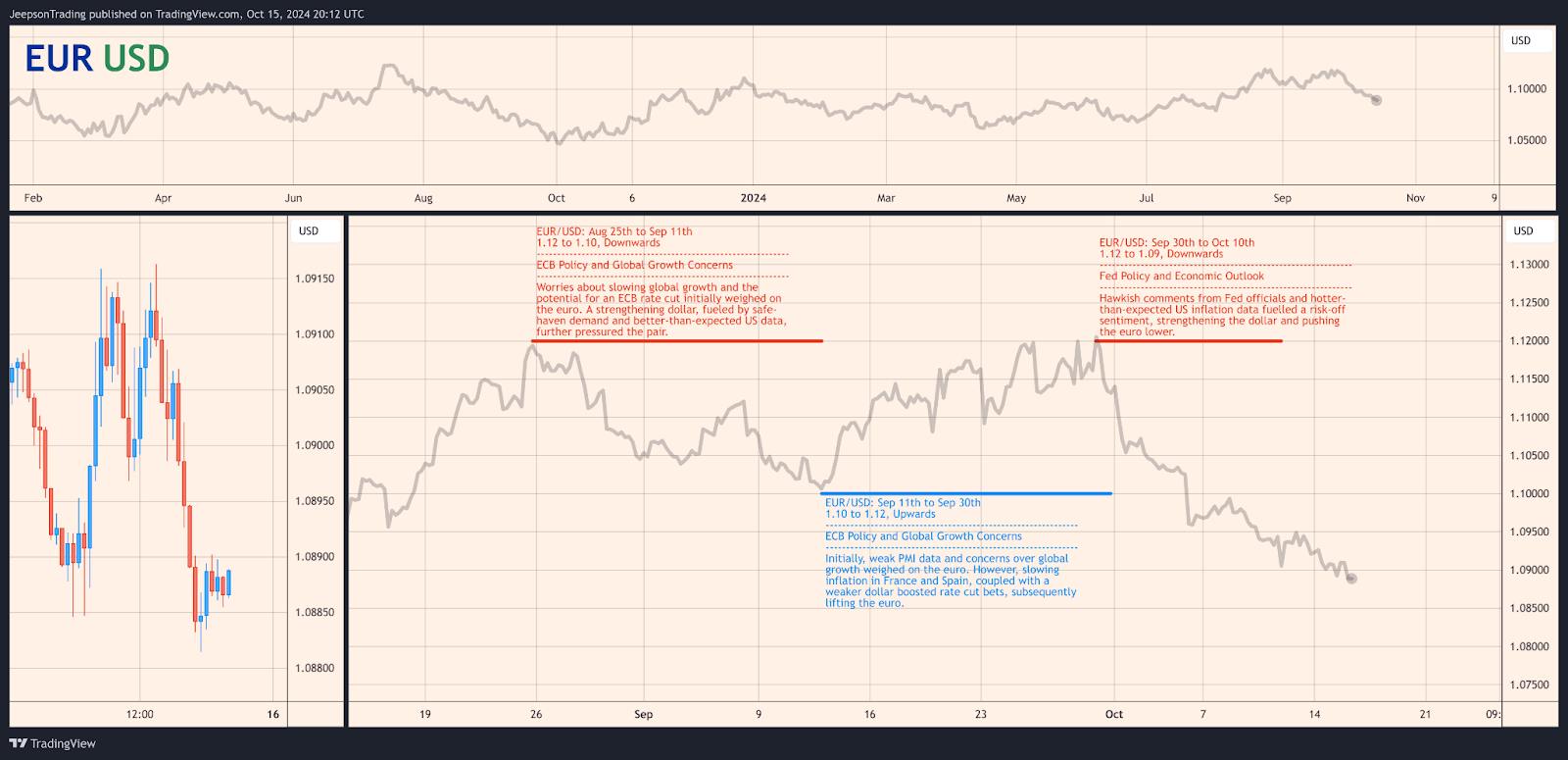

EURUSD: Eurozone's Uncertain Path

EURUSD is one of the most liquid forex pairs, actively traded by institutions, central banks, and corporations. The euro's reserve currency status drives liquidity. German Bund yields typically exhibit an inverse correlation. The October 8th COT report suggests a net short EUR position for Asset Managers/Institutions while Leveraged Funds hold a similar position.

The dominant theme impacting EURUSD is the ECB's policy trajectory amidst Eurozone economic weakness. The September rate cut signalled a dovish tilt, but uncertainty remains around future easing. The Eurozone’s sluggish growth and disappointing PMI data weigh on the euro. Renewed optimism around Chinese stimulus could provide support, but concerns persist about US economic performance.

Bullish Thesis (Upcoming Week): Low Conviction. EURUSD could experience a modest bounce although this is restricted by the broader narrative of Eurozone economic weakness.

Bearish Thesis (Upcoming Week): Moderate Conviction. If the Eurozone trade balance (Oct 17th) disappoints or US data surprises to the upside, EURUSD could decline further. A worsening geopolitical climate could add to EURUSD’s vulnerability.

What to Watch:

EUR: Industrial Production MoM (Oct 15th), forecast -0.3%; Balance of Trade (Oct 17th), forecast €21.2B; Inflation Rate YoY Final (Oct 17th), forecast 1.8%

USD: Retail Sales MoM (Oct 17th), forecast 0.3%; Initial Jobless Claims (Oct 17th), forecast 241K; Philadelphia Fed Manufacturing Index (Oct 17th), forecast 3

Conclusion

This report has analysed four major currency pairs—USD/JPY, USD/CAD, GBP/USD, and EUR/USD—examining the dominant narratives and emerging themes influencing their recent movements. Looking ahead, market sentiment is likely to remain cautious, dominated by the impending UK Autumn Budget and persistent geopolitical tensions. The upcoming week's economic calendar includes key data releases, such as US retail sales and inflation figures from several major economies. These releases will be closely scrutinised for clues about central bank policy trajectories, potentially triggering volatility in the forex market.

Key Takeaways:

Monitor geopolitical developments, particularly in the Middle East. Escalation could fuel haven flows, impacting USD valuations.

The UK Autumn Budget (October 30th) will be a pivotal event for GBP. Be prepared for potential volatility.

Pay close attention to upcoming US and Eurozone data releases. These could significantly shift market sentiment and influence central bank policies, impacting forex pair valuations.

Sources: Bloomberg, Trading Economics, Federal Reserve, Bank of Canada, Bank of England, European Central Bank, Statistics Canada, Office for National Statistics, INSEE, GfK Group, BRC, Nationwide Building Society, Ivey Business School, Cabinet Office Japan, Ministry of Finance Japan, Ministry of Internal Affairs & Communications Japan, S&P Global, Reuters, Australian Bureau of Statistics.