CA MACROECONOMICS: Trade Tensions and Election Sway the Loonie

The CAD has been Neutral, likely to Moderately Weaken

The CAD has been Neutral, likely to Moderately Weaken

Unveiling the Loonie's Story: Past and Future Strength

This macroeconomic analysis delves into the multifaceted story of the Canadian Dollar, its intricate relationship with oil markets, and the broader economic forces shaping its trajectory. Over the preceding seven months, the Canadian Dollar's fundamental strength has been assessed as NEUTRAL, reflecting a balance of economic resilience and emerging headwinds. Looking ahead, the outlook for the next seven months suggests a MODERATELY WEAKENING fundamental strength, as the currency navigates a landscape increasingly defined by trade tensions and domestic economic adjustments.

Context: What's Weighing on Traders' Minds?

Canadian Dollar traders are likely focused on several connected elements. The growing trade tensions with the US, a crucial economic partner, are paramount. President Trump's tariffs and Canada's responses create unpredictability regarding the immediate economic effects. The Bank of Canada's easing monetary policy, with potential further rate cuts due to these trade challenges, is also a key consideration. Mixed domestic economic signals add another layer of complexity. Furthermore, the upcoming April 2025 federal election introduces political uncertainty, as the results could alter the government's strategy for tackling these significant economic issues. Comprehending these interwoven factors is essential for assessing the Canadian Dollar's present and future underlying value.

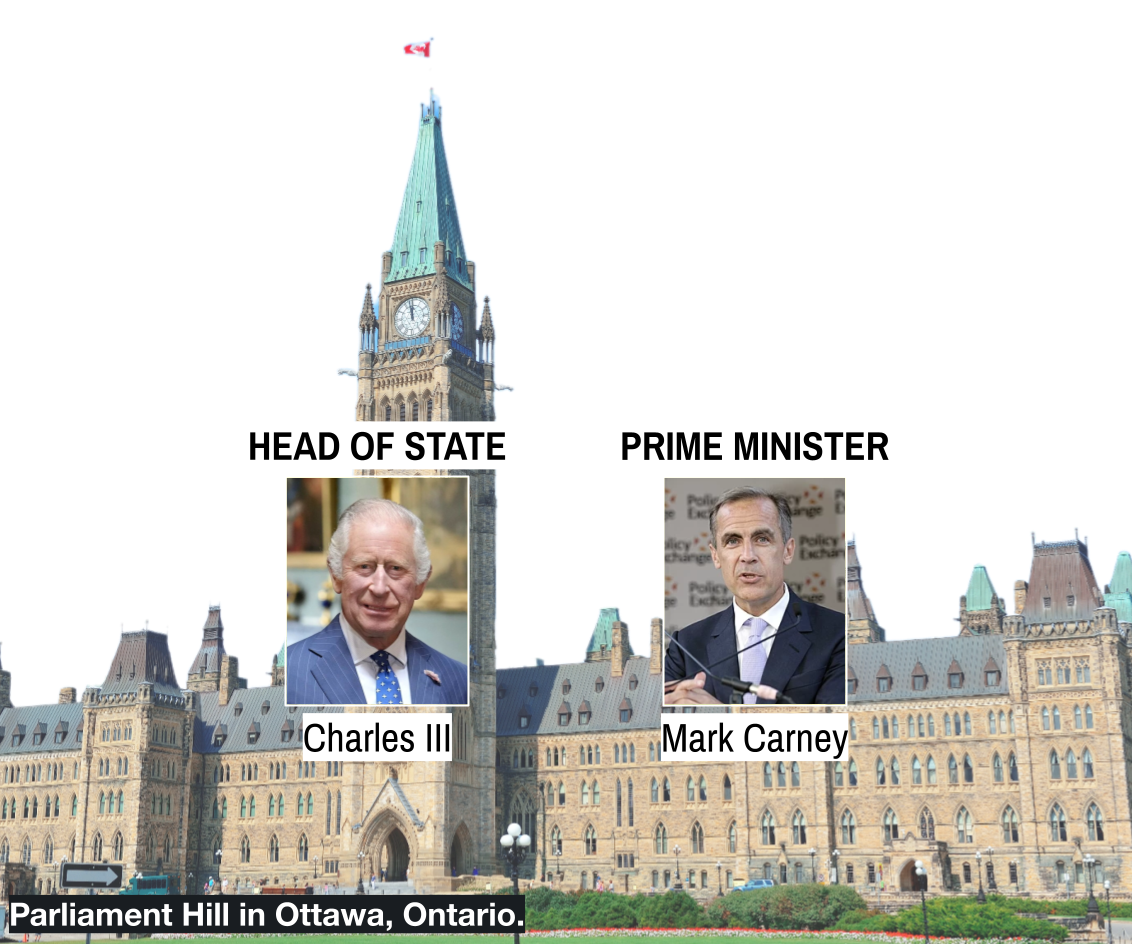

GOVERNMENT Federal Election April 28th

In March 2025, Mark Carney of the Liberal Party became Canada's Prime Minister, following his time leading the central banks of both Canada and England. Shortly after taking office on March 14th, a snap election was called for April 28th, setting up a quick, five-week campaign. His initial focus: bolstering Canada's G7 economic standing, creating jobs, and resolving US trade tensions, especially concerning Trump's tariffs.

Recent Events in Government

Late 2024 saw rising political tensions, with the NDP pulling support from the Liberal minority in September. Trudeau's January 2025 resignation led to Carney's Liberal leadership win in early March. The outgoing government made key policy moves, like the Oil and Gas emissions cap and Arctic Foreign Policy. Immediately after taking office on March 14th, Carney announced middle-class tax cuts, GST elimination for first-time buyers, and ended the carbon tax. Then, a snap election was called on March 23rd, signalling a push for a strong mandate.

Outlook for Government Policy

The snap federal election on April 28, 2025, will shape the next seven months. The outcome dictates the government's path and policy implementation. The seven weeks leading up will be dominated by campaigning. Key debates center on Canada-US trade, recession-proofing the economy, and housing affordability. Prime Minister Carney's tax cuts and housing plans are central to the Liberal campaign. Public opinion will be swayed by the government's handling of US tariffs and trade disputes. Early policy shifts on carbon tax and immigration will also face scrutiny.

CENTRAL BANK Navigating Trade Winds

Governor Tiff Macklem, in office since June 2020, will lead the Bank of Canada until June 2027, navigating economic uncertainties. The Bank's current policy is easing, with March 2025's rate cut bringing it to 2.75%. This easing, begun in June 2024, responds to trade issues and potential slowdowns. The Bank aims to keep inflation at 2%, a challenge given global economic pressures.

Recent Central Bank Actions

In the last seven months, the Bank of Canada actively adjusted monetary policy due to moderating inflation and rising economic risks. Starting in July 2024, a series of interest rate cuts lowered the key rate from 4.50% to 2.75% by March 2025. Inflation, around 2% in August 2024, generally stayed within the Bank's target. January 2025 saw the end of quantitative tightening, further easing the stance. Most recently, on Wednesday, March 12, 2025, the Bank announced its seventh straight rate cut, bringing the key rate down another 25 basis points to 2.75%.

Outlook for Monetary Policy

The Bank of Canada's monetary policy in the next seven months will heavily depend on the changing US trade relationship and global economics. The upcoming interest rate announcement and Monetary Policy Report on Wednesday, April 16, 2025, will be key indicators of future policy. Markets increasingly anticipate further rate cuts in 2025, with some predicting the rate could drop to 2.25% or even 1.5% by year-end. In the next seven weeks, the Bank's April announcement will be crucial. The accompanying Monetary Policy Report will offer updated economic predictions and detail the Bank's plan for dealing with the ongoing trade conflict and its effects on inflation and growth.

ECONOMIC GROWTH A Mixed Terrain

With a $2.14 trillion USD GDP in 2023, projected to grow to $2.21 trillion by the end of 2024, Canada stands as a significant global economy, ranking tenth-largest worldwide. Its economy is diverse, with services contributing the most at two-thirds of the GDP, alongside strong real estate, manufacturing, and natural resources. The United States is its top trade partner, followed by China and the United Kingdom.

Recent Economic Performance

The Canadian economy has fluctuated in the last 7 months. Despite lessened US recession fears and easing inflation, trade tensions and tariffs with the US have led to weaker consumer confidence and slower business investment, resulting in an expected economic slowdown in early 2025.

Economic Outlook Navigating Uncertainty

The economic outlook for Canada over the next seven months is clouded by significant uncertainty, largely stemming from the ongoing trade dispute with the United States. GDP growth forecasts for 2025 vary considerably, ranging from Trading Economics' projection of 0.6% by Q2 2025 to the IMF's more optimistic 2.4%. The Bank of Canada projects 1.8% growth for both 2025 and 2026, while other institutions like Vanguard and BofA Securities have revised their forecasts downwards, citing trade uncertainties. TD Economics even forecasts a mild recession in mid-2025 due to the trade war. In the immediate seven weeks, the Canadian economy is expected to experience slower growth, potentially facing recessionary pressures, as the impact of US tariffs and retaliatory measures becomes clearer. The value of the Canadian dollar is anticipated to remain under pressure. Key factors influencing the outlook include the trajectory of US tariffs, the Bank of Canada's monetary policy response, the performance of the housing market, global economic conditions, and oil price volatility.

Economic Indicators Gauging Canada's Economic Pulse

To understand Canada's economic state, financial markets watch key indicators like inflation (CPI, Core CPI), unemployment, job changes, retail activity, consumer sentiment, GDP growth, trade, housing starts, building permits, and the PMI. Present market drivers include uncertain US trade policies, differing monetary approaches between Canada and the US, inflation levels, housing market shifts, and oil price volatility. The interaction between the Bank of Canada's move toward a looser monetary stance and recent inflation increases is a key dynamic that could influence the Canadian Dollar and bond yields.

Recent Indicator Trends

Canada's economic signals over the last seven months have been varied. Inflation eased for much of 2024, hitting 2.5% in July, but then rose to an eight-month high of 2.6% in February 2025, mainly due to the end of temporary tax relief. Core inflation also edged up to 2.7% in February. After showing signs of slowing down in mid-2024, the job market picked up between November 2024 and January 2025, but then leveled off in February 2025, with unemployment staying at 6.6%. Retail sales have fluctuated, dropping in June 2024 before a strong rebound in December 2024, though early data suggests a fall in January 2025. Consumer confidence has noticeably decreased, likely due to trade tensions. GDP growth was strong at 2.6% in the fourth quarter of 2024, and the Bank of Canada lowered its key interest rate to 2.75% in March 2025. The Canadian Dollar has been fairly stable against the US Dollar but has weakened compared to other major currencies.

Indicator Outlook Navigating a Complex Picture

Forecasts for key Canadian economic indicators over the next seven months present a varied landscape. Inflation is expected to rise in the near term due to the end of tax breaks, with Trading Economics projecting 2.5% by Q2 2025. The Bank of Canada anticipates a temporary increase to around 2.5% in March 2025. Unemployment rate forecasts vary, with Vanguard anticipating a rise to 7% by year-end, while the PBO projects 6.3% for 2025. Interest rate forecasts also diverge, with Trading Economics expecting rates to remain at 2.75% by Q2 2025, while Vanguard anticipates a further cut to 2.25% by year-end. Canadian Dollar forecasts range from 1.44 to 1.40 against the USD by Q2 2025, influenced by trade war developments and monetary policy. Oil price forecasts range around $68-74 USD/BBL by Q2 2025. In the immediate seven weeks, inflation is expected to rise further, while the labor market outlook remains uncertain. Consumer confidence is likely to remain subdued due to trade tensions. The Bank of Canada's upcoming interest rate announcement and Monetary Policy Report in April will be crucial in shaping market expectations and providing further insights into the near-term economic outlook.

GEOPOLITICS Balancing Act

As a middle power, Canada emphasizes international collaboration, with a historical focus on peace. Current US trade policies and relations are testing its global standing. Key allies include the US, UK, and France, and its participation in NATO, the G7, and the WTO is central to its international activities.

Recent Geopolitical Developments

Between August 2024 and March 2025, Canada navigated increasing trade friction with the US, responding with counter-tariffs while also seeing wider tariffs reintroduced by President Trump in March 2025. Recognizing this shift, Prime Minister Carney focused on strengthening ties with France and Britain, signaling a move towards broader international partnerships. Canada also sustained its support for Ukraine amidst the ongoing conflict with Russia. In the Arctic, Canada remained engaged within the Arctic Council, launching its Arctic Foreign Policy in December 2024. Domestically, reinforcing border security and the immigration system was a priority, leading to new measures and planned enhancements. Additionally, Canada upheld sanctions against Russia and Haiti and appointed a new Fentanyl Czar in February 2025 to address the flow of illicit drugs.

Geopolitical Outlook: Navigating a Turbulent World

The next seven months hinge on Canada's US trade ties, with election results and US policy driving the relationship's direction. Balancing this with Arctic goals and Ukraine support is key. The 2025 G7 summit offers global influence. In the next seven weeks, the election will spotlight Canada-US relations, as parties debate how to handle Trump's tariffs. Trade escalation risks loom, especially after April's tariff consultations. Prime Minister Carney's "mutual respect" strategy with Trump will be scrutinized.

Fundamental Strength Debate: Decoding Currency Fundamentals

Previous Seven Months

Cases for Strong CAD Fundamentals:

Stronger than expected GDP growth in Q4 2024

Household spending remained robust

Tight labor market with steady unemployment

Strong job gains in the year prior to February 2025

Widening trade balance surplus in January 2025

BoC signaling caution towards further rate cuts

Cases for Weak CAD Fundamentals:

Escalating trade tensions and tariffs with the US

Downward revision of 2025 economic forecasts

Inflation uptick in February 2025

Declining consumer confidence

Slowing business investment

Depreciation of the CAD vs USD

Political uncertainty

Upcoming Seven Months

Cases for a Strengthening Outlook for the CAD Fundamentals:

Resolution or easing of US-Canada trade tensions

Rebound in global oil prices due to increased demand or supply constraints

Positive surprises in Canadian economic data (GDP growth, employment, inflation)

Decisive federal election outcome providing political stability and a clear policy mandate

Continued strength in key sectors (technology, finance) attracting foreign investment

Cases for a Weakening Outlook for the CAD Fundamentals:

Ongoing trade conflict with the US

Slower-than-expected economic growth

Continued monetary easing by the BoC

Deteriorating global economic conditions could negatively impact commodity prices

Political uncertainty surrounding the upcoming federal election and potential policy shifts

Most Probable Scenario: Neutral Fundamental Strength, Moderately Weakening Outlook

Fundamental Strength (Previous Seven Months): NEUTRAL

The Canadian dollar's fundamental strength over the previous seven months can be best characterized as neutral. While the economy showed pockets of resilience, particularly in GDP growth, these were counterbalanced by significant headwinds. Positive factors such as a robust financial system and natural resource wealth were offset by escalating trade tensions, declining consumer confidence, and a dovish monetary policy stance from the Bank of Canada. The mixed economic data and uncertain political landscape created a neutral fundamental backdrop, preventing the currency from establishing a clear direction.

Fundamental Strength Outlook (Upcoming Seven Months): MODERATELY WEAKENING

The fundamental strength outlook for the Canadian dollar over the upcoming seven months is most likely moderately weakening. The escalating trade conflict with the United States represents a significant downside risk that is expected to outweigh any potential positive factors. The anticipated slowdown in economic growth, coupled with the likelihood of further Bank of Canada interest rate cuts, will likely exert downward pressure on the currency. While a resolution to the trade dispute or a rebound in oil prices could offer some upside potential, the most probable scenario is a continued gradual weakening of the Canadian Dollar as the economic and geopolitical uncertainties persist. The snap federal election adds a further layer of uncertainty, potentially delaying crucial policy decisions and exacerbating market caution. Therefore, a moderately weakening fundamental strength outlook appears to be the most realistic scenario for the Canadian Dollar in the coming months.

Conclusion: Neutral Now, Cautious Ahead

In conclusion, our macroeconomic analysis suggests that the fundamental strength of the Canadian Dollar over the past seven months can be best described as neutral. While the Canadian economy has demonstrated pockets of strength and resilience, these positives have been counterbalanced by significant headwinds, most notably the escalating trade tensions with the United States. Looking forward to the upcoming seven months, the most probable scenario points towards a moderately weakening fundamental strength outlook for the Canadian Dollar. The persistent trade conflict, anticipated slower economic growth, and the likelihood of further monetary easing by the Bank of Canada are expected to exert downward pressure on the currency. Navigating this complex landscape will require careful monitoring of trade policy developments, central bank actions, and the evolving global economic picture as Canada charts its course through these uncertain times.

Sources

Trading Economics, Bloomberg, Reuters, Financial Times, Wall Street Journal, CNBC, Teletrade, Mitrade, The Bull Vine, Forex24, Bank of Canada, American Petroleum Institute, US Bureau of Economic Analysis, US Bureau of Labor Statistics, Statistics Canada, Agrimoon, S&P Global Commodity Insights, ICE Futures U.S., OFX, Exchange Rates UK, S&P Global, BusinessNZ, NAHB.