Dollar moving to the downside, pressured by peak rate sentiment

Dollar Currency Report -November (Monetary Policy update)

Derbyshire, UK – November 4th, 2023: This is the currency report for the US Dollar and is intended to be a reference aid for your own analysis and trade planning. The next update will be after the inflation report on Tuesday, November 14th.

Trading involves a possibility of losing money therefore all decisions in market speculation are undertaken at your own financial risk.

Dollar moving to the downside, pressured by peak rate sentiment

The economic outlook for Q4 is mixed. Some indicators point to a slowdown, such as sluggish GDP growth and stalling retail sales. However, other indicators suggest continued growth, such as strong GDP growth in Q3 and low risk of a recession.

Traders should be aware of the risks and opportunities presented by this uncertain environment. Potential risks include a recession, rising interest rates, and continued inflation. Potential opportunities include sectors that are likely to benefit from a slowdown, such as consumer staples and utilities.

Other factors to consider include the conflict in Israel-Hamas, the war in Ukraine, and the US-China trade war. These conflicts and tensions could add uncertainty to the global economy and impact the US dollar.

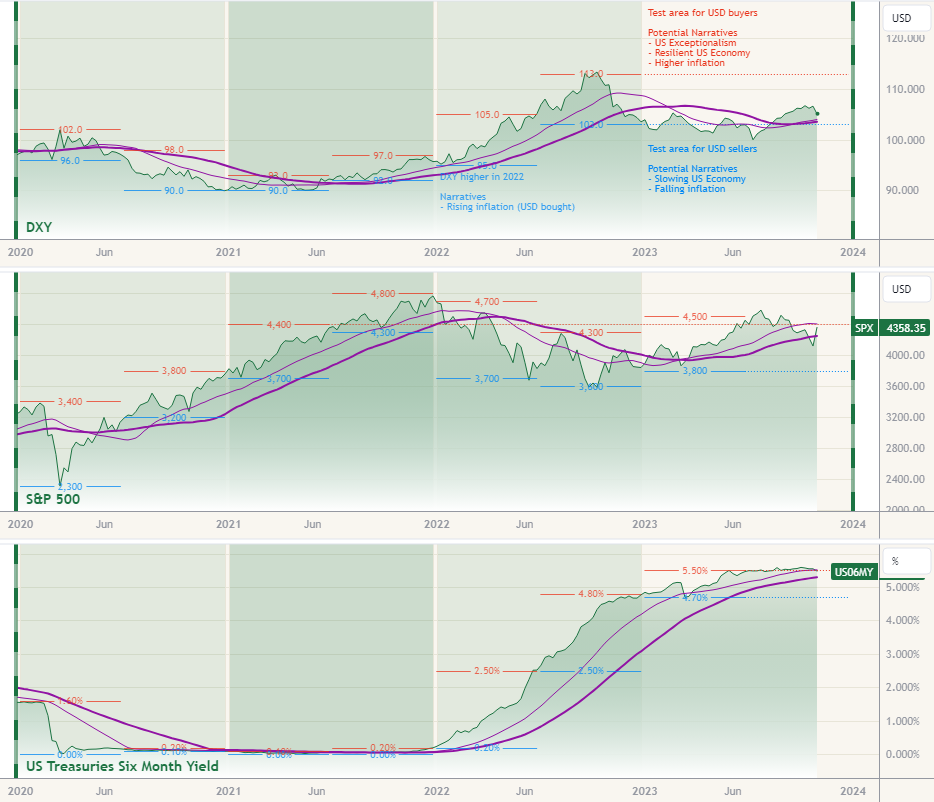

Dollar under selling pressure

DXY was flat in October and indicative of even buying and selling pressure. Dollar sellers are evaluating the soft economic outlook which would lead to the Fed being at peak rate, while dollar buyers grapple with the potential for further rate hikes and also geopolitical uncertainty.

Downside moves towards 104.5 are possible if market sentiment focuses on the slowing US economy and leads investors to believe that the Fed may cut sooner. The long-term support level is in the 103.0 area.

Upside moves towards 106.8 are possible if the US economy outperforms expectations and, or inflation remains high. The long-term resistance level is in the 113.0 area.

The US stock market index (S&P 500) has recently been falling although remains above the 200-day moving average and showing signs of optimism that the fed may cut sooner.

The yield on US six-month treasury bonds has recently been ticking higher and remains above the 200-day moving average and showing signs that some market participants are considering the Fed will hold rates higher for longer.

The Fed held interest rates at its November meeting, signalling a shift away from its ultra-hawkish stance. This is good news for consumers and businesses, as it could mean lower borrowing costs in the future.

The economy's performance relative to the Fed's projections is mixed. Real GDP growth is expected to be sluggish, but the risk of a recession is low. Annual PCE inflation is expected to come in below expectations, while unemployment is expected to rise slightly.

Overall, the US economic outlook is uncertain. The Fed is committed to bringing inflation back to its 2% target, but it is also aware of the risks of raising rates too aggressively. The Fed is likely to continue monitoring economic data closely and adjusting its policies accordingly.

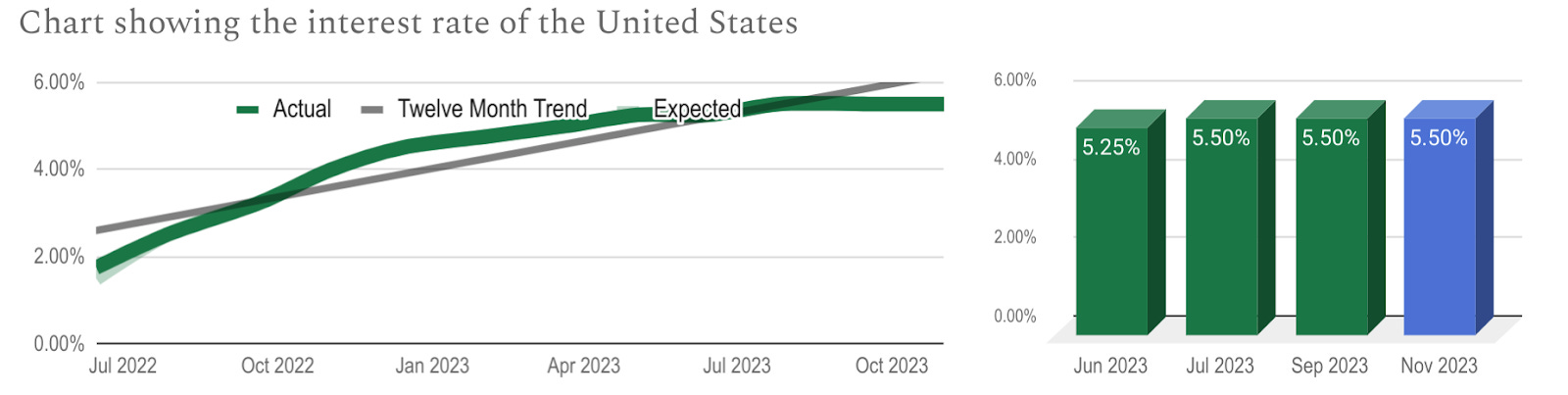

Interest rates held, no hikes or cuts in sight

The seven members of the Federal Reserve’s (Fed) Federal Open Market Committee (FOMC) set monetary policy, including the Federal Funds rate (interest rate). The Federal Funds rate is the interest rate that banks pay to borrow money from other banks. This rate affects the interest that banks charge their borrowers.

The FOMC meets to set monetary policy eight times a year, the latest was November 1st and the next is on December 13th.

The interest rate of the US was held at the November meeting after being held in September but had been hiked throughout most of the previous twelve meetings. This indicates that the Federal Reserve is moving away from its ultra-hawkish stance as inflation has been falling quickly. Trading Economics forecast another hike to reach a peak of 5.75% and 2024 to see cuts to 5.25%.

Key points of the Federal Reserve’s FOMC meeting:

Maintained the federal funds rate

The Fed is concerned about inflation and is committed to bringing it back to its 2% target.

The Fed will continue to monitor economic data and adjust its policies as needed.

Sources: The Federal Reserve, Trading Economics, FXStreet

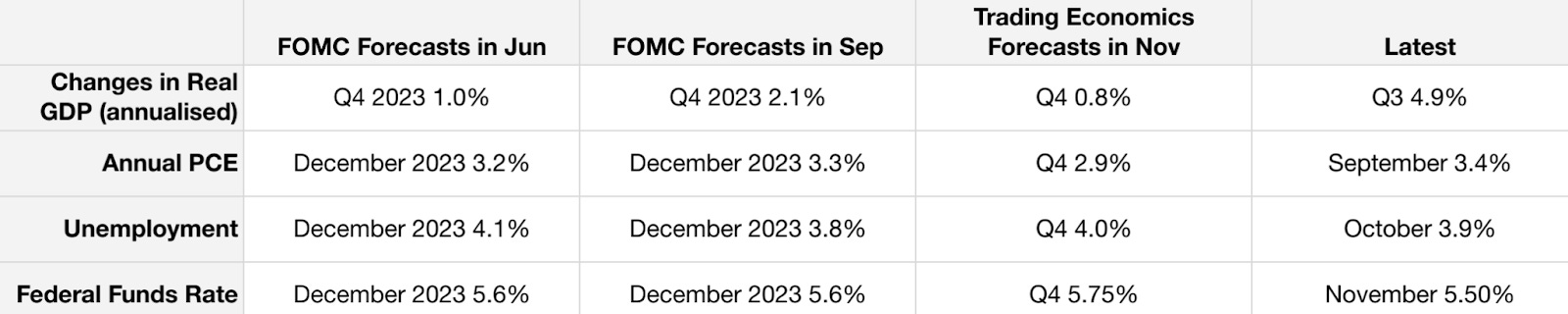

Indifferent economic outlook for Q4

The Federal Reserve’s Federal Open Market Committee (FOMC) makes economic forecasts four times a year. The most recent was at their September meeting and they will be updated in December.

Changes in Real GDP (annualised) has a very pessimistic outlook compared to the FOMC’s forecast although the risk of a recession is minimal.

Annual PCE has an optimistic outlook compared to the FOMC’s forecast and is on track to come in below expectations.

Unemployment has a pessimistic outlook compared to the FOMC’s forecast and it could climb higher.

The Federal Funds Rate is on track to match the FOMCs’ forecast and is likely at the peak with small cuts beginning to be priced in for 2024.

The US economy bounced back in Q3 with strong GDP growth, but there are signs of a slowdown in Q4. Inflation remains elevated, putting pressure on budgets and businesses. Retail sales stalled in September, suggesting consumer spending may be cooling. Non-farm payrolls growth slowed in November and the unemployment rate edged up, suggesting the labour market is tightening.

Overall, the economy is still growing but at a slower pace. This is reflected in Trading Economics' GDP forecast of just 0.8% in Q4, which is below the baseline trend. This suggests that economists are pessimistic about the pace of future economic growth.

From a trader's perspective, this means that there are both risks and opportunities. The risks include a potential recession, rising interest rates, and continued inflation. The opportunities include sectors that are likely to benefit from a slowdown, such as consumer staples and utilities. It is also important to be aware of the potential for volatility in the markets.

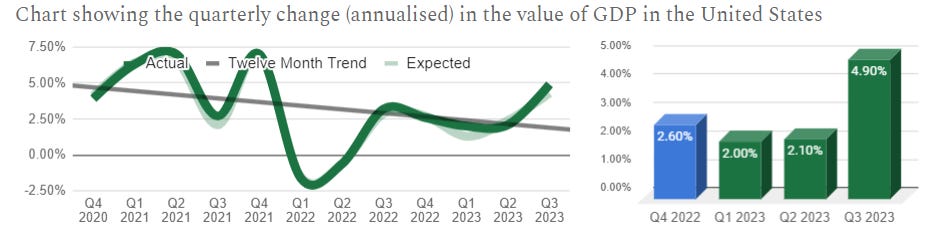

Slowing economy bounces higher in Q3, Q4 expected to be far weaker

The US GDP quarterly rate report measures the change in value of goods and services produced in the US over a given quarter compared with the previous and then annualised. The latest data covers the Q3 period and was published on October 26th by the Bureau of Economic Analysis and the next version is out on November 29th.

The latest result of 4.90% was far above expectations and signals that the economy is growing and at a fast pace as it is far higher than the previous quarter and far above the baseline trend.

Trading Economics are forecasting 0.8% for Q4 which would be below the baseline trend of 1.9% and suggest pessimism with regards to future economic growth.

Sources: Bureau of Economic Analysis, Trading Economics, FXStreet

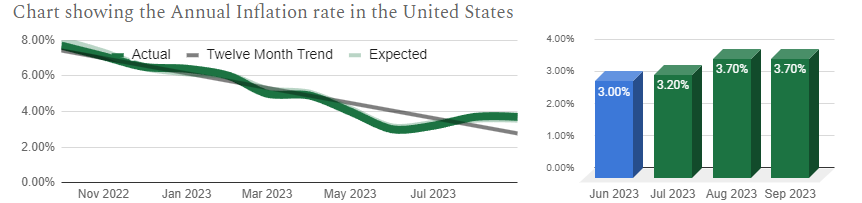

Falling inflation halts in September, applies indifferent pressure to Q3 growth expectations

The US inflation rate report measures the change in value of a basket of goods and services in the US over a given month compared with the previous. The latest data covers the August period and was published on October 12th by the Bureau of Labour Statistics and the next version is out on November 14th.

The latest result of 3.70% was just above expectations and signals that the falling rate of inflation is slowing as it matches the previous month and is above the baseline trend. This applies indifferent pressure to the economic outlook as demand steadies.

Trading Economics are forecasting 3.0% for Q4 which would be close to the baseline trend of 3.1% and suggest indifference with regards to the pace of falling inflation.

Sources: Bureau of Labour Statistics, Trading Economics, FXStreet

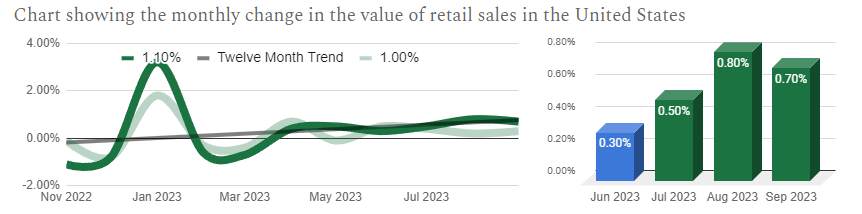

Rising retail sales stalls in September, applies indifferent pressure to Q3 growth expectations

The US retail sales report measures the change in value of aggregated retail goods and services sales over a given month compared with the previous. The latest data covers the September period and was published on October 17th by the Census Bureau and the next version is out on November 15th.

The latest result of 0.70% was far above expectations and signals that the rising rate of retail sales is set to continue although it is a minor fall from the previous month, it is on track with the baseline trend. This applies some bullish pressure to the economic outlook as consumers spend more.

Trading Economics are forecasting 0.2% for Q4 which would be below the baseline trend of 0.6% and suggest pessimism with regards to a continuation of rising sales.

Sources: Census Bureau, Trading Economics, FXStreet

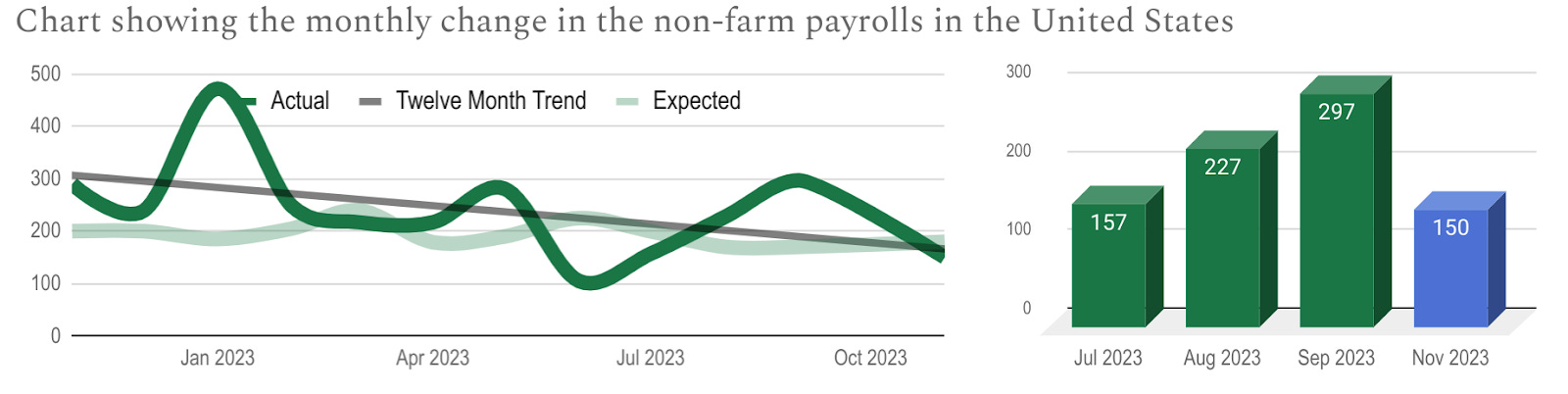

Payrolls give up the recent gains, applies bearish pressure to Q4 growth expectations

The US non-farm payrolls (NFP) report measures the change in the number of paid workers not employed by farms (due to seasonality) over a given month compared with the previous. The latest data covers the November period and was published on November 3rd by the Bureau of Labor Statistics and the next version is out on December 8th.

The latest result of 336K was below expectations and signals that the recent rise has fallen and the value reverts to the baseline trend. This applies indifferent pressure to the economic outlook as new hires are close to expected levels.

Trading Economics are forecasting 100K for Q4 which would be below the baseline trend of 175K and suggest pessimism with regards to the rate of payrolls and its fall.

Sources: Bureau of Labor Statistics, Trading Economics, FXStreet

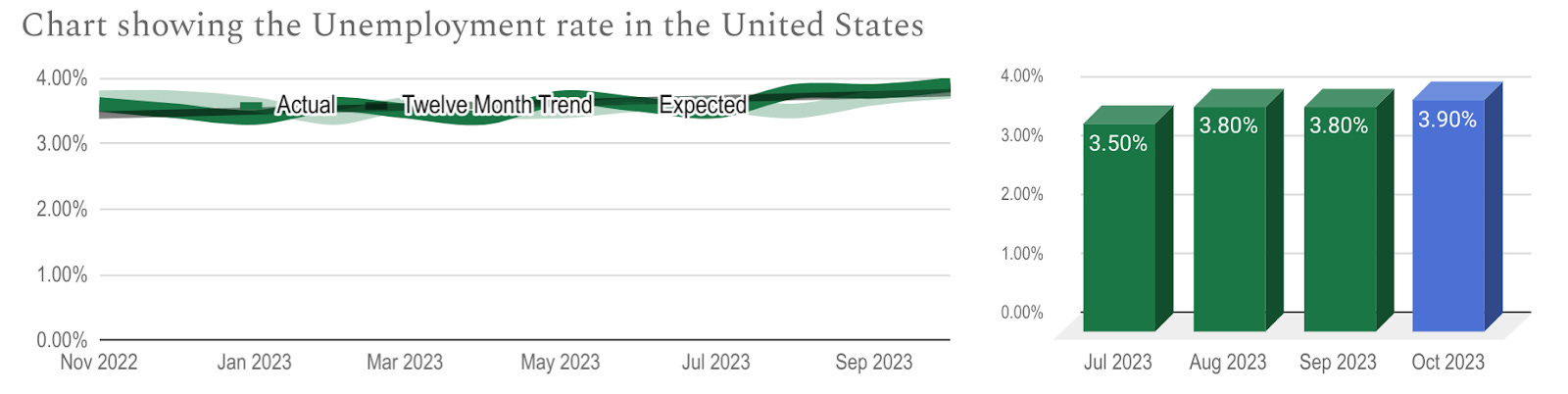

Unemployment moves higher, applies some bearish pressure to Q3 growth expectations

The US unemployment rate report measures the number of people actively looking for a job as a percentage of the labour force over a given month. The latest data covers the October period and was published on November 3rd by the Bureau of Labor Statistics and the next version is out on December 8th.

The latest result of 3.90% was just above expectations and signals that the stable rate of unemployment is cracking as it is higher than the previous month and the baseline trend. This applies some bearish pressure to the economic outlook as businesses reduce employment levels.

Trading Economics are forecasting 4.0% for Q4 which would be above the baseline trend of 3.8% and suggest some pessimism with regards to a stable labour market.

Sources: Bureau of Labor Statistics, Trading Economics, FXStreet

The conflict in Israel-Hamas in October 2023, while limited in scope and impact on the wider world, could potentially add uncertainty. If the conflict were to escalate, involving regional powers such as Iran, there might be significant safe-haven flows into the US dollar. The war in Ukraine, which began in 2014 and has seen recent key events in 2023, is already having a negative impact on the global economy and the US dollar. It has caused energy prices to rise, disrupted supply chains, increased inflation, and led to greater demand for the US dollar as a safe-haven currency. Additionally, the ongoing US-China trade war, which began in 2018 and has seen recent developments, has contributed to economic uncertainty, affecting both nations' economies.

October 2023 Israel-Hamas War has the potential to add uncertainty

The ongoing conflict between Hamas-led Palestinian militants and Israel started on October 7, 2023, when Hamas launched a surprise offensive called "Al-Aqsa Flood." This led to thousands of rockets fired into Israel and Palestinian militants breaching the Gaza-Israel barrier, resulting in casualties on both sides. The conflict is part of the long-standing Israeli-Palestinian issue, with increased violence in 2023 leading to this escalation. Hamas cited various reasons for their attack, including the desecration of the Al Aqsa mosque and the Gaza Strip blockade.

The conflict has caused significant displacement of Palestinians and calls for a ceasefire from the United Nations and many countries. Both Israel and Hamas have been accused of war crimes. International reactions vary, with some nations denouncing Hamas as a terrorist group and others focusing on the Israeli occupation of Palestinian territories. Iran has warned against Israeli military aggression.

The conflict is limited in scope and its influence on the wider world. However, if the conflict were to escalate and regional powers such as Iran were to become involved then there are likely to be significant safe-haven flows into the USD.

Russian Invasion of Ukraine Adds Uncertainty

On February 24, 2022, Russia invaded Ukraine in an escalation of the Russo-Ukrainian War which began in 2014. The invasion is the largest military conflict in Europe since World War II and has resulted in tens of thousands of casualties on both sides. The invasion has also caused a humanitarian crisis, with millions of Ukrainians displaced from their homes. The international community has condemned the invasion and imposed sanctions on Russia. The International Criminal Court is investigating possible war crimes and crimes against humanity committed by Russian forces.

Recent Key Events

June 2023: The Ukrainian counteroffensive in June 2023 made significant progress, with Ukraine liberating villages and reclaiming territory in the eastern Donbas region. The Wagner Group's rebellion against the Russian government was a major setback for Russia.

August 2023: Ukraine counteroffensive slowed by millions of mines laid by Russia. Ukrainian drones damage the Russian landing ship Olenegorsky Gornyak.

September: An attack on Russian naval targets in Sevastopol damages the Black Sea fleet. Several oil and gas drilling platforms on the Black Sea held by Russia since 2015 have been retaken.

The war in Ukraine is having a negative impact on the global economy, including the value of the US dollar. The war has caused energy prices to soar and disrupted supply chains, which are putting upward pressure on inflation and increasing demand for US dollars as a safe-haven.

China-United States trade war adds uncertainty

The US and China have been engaged in a trade war since 2018, with each side imposing tariffs on the other's goods in an attempt to force changes in trade practices. The trade war has had a negative impact on both economies.

Recent Key Events

December 2022: WTO ruled against US tariffs on steel, aluminium, and Hong Kong origin marking. The US is in breach of global trade rules for its tariffs on steel and aluminium, as well as its origin marking requirement for products imported from Hong Kong. The US has disputed the WTO rulings and has not taken any steps to comply.

January 2023: EU and US announce joint effort to block sale of advanced semiconductor chip technology to China.

February 2023: China expands Unreliable Entities List to include US defence contractors.

June 2023: US Secretary of State visits China, seeks to clarify US economic stance, but Chinese officials reject explanation.

July 2023: US Treasury Secretary criticises China's economic restrictions during visit to Beijing, stresses US goal to expand economic partnership.

Gavin Pearson

Retail trader since 2008

Specialises in forex G7 currencies

Funded account from the5ers.com

Member of the eToro Popular Investors Program

Regular contributor to FXStreet.com analysis and education pages

Returned 27% in 2022 and 5.8% in 2023 H1

Forex focused

Copy Trading available at eToro

Disclaimer

Past performance is not indicative of future results

Trading involves risk, and you could lose money

-end-