Euro Currency Report September - ECB update

Derbyshire, UK – September 14, 2023: The ECB raised rates by 0.25% when markets had considered a pause. Along with the hike, the ECB also downgraded growth which they expect to be dampened by the rates remaining higher for longer. The next update is planned to be published after the EA CPI report on Tuesday, September 19th or before if any significant event occurs.

Decisions to trade are made at your own monetary risk.

Euro Currency Report Summary

The macroeconomic outlook of the Euro-Area (EA) economy suggests the euro will have a slightly bearish weakness due to higher-for-longer interest rates and safe-haven outflows amid the war in Ukraine and its subsequent impact on the wider economy.

The EA interest rate is anticipated to be held at its present level which is likely to lead to stagnant borrowing. This suggests an indifferent outlook for the EA economy and may apply indifferent pressure to the value of the euro.

EA GDP is projected to improve to 0.4% in Q3 although it missed expectations in Q2 and suggests an indifferent outlook for the EA economy and may apply indifferent support to the value of the euro.

EA CPI is projected to fall towards 5.1% in Q3 which is revised up from 4.7% after coming in at 5.3% for July, missing expectations and suggests a slightly pessimistic outlook for the EA economy and may apply downward pressure to the value of the euro.

EA unemployment is projected to slightly deteriorate to 6.6% this quarter after coming in at 6.4% for July, matching expectations and suggests a cautiously optimistic outlook for the EA economy and may apply some upward support to the value of the euro.

The Russia-EU Gas dispute is likely to apply upward support to the value of the euro as the price pressures of 2022 have significantly eased.

The war in Ukraine will at times cause risk aversion and may lead to decreased foreign investment and apply downward pressure to the value of the euro.

Monetary Policy

The European Central Bank (ECB) Governing Council

In the Euro Area, the benchmark interest rate is set by the Governing Council which consists of six members from the Executive Board plus governors of the national central banks from the nineteen countries using the euro.

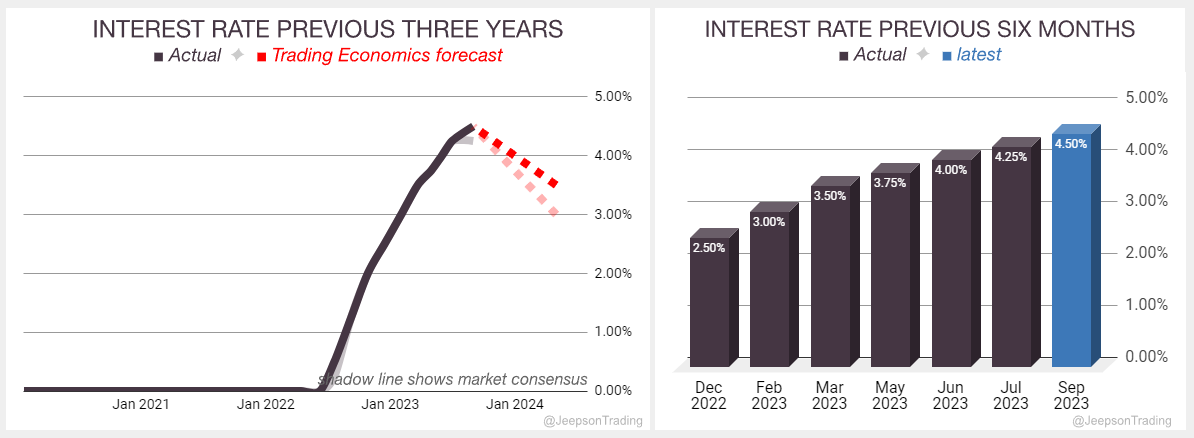

The September meeting saw a 0.25% hike of the Main Refinancing Operations rate setting it at 4.50% which is up from 4.20% and the 0.25% hike in July. Markets were expecting a hold.

The latest rate now matches the Trading Economics Q3 ‘23 forecast of 4.50% which they also identify as the peak.

Over the previous three years, since the start of 2020, the interest rate has been trending up with a low of 0.00% and a high of 4.50%. Over the previous six months, the rate has continued to climb.

The next meeting is due on Thursday, October 26th.

The Governing Councils September statement summarised:

Rates raised by 25 basis points to combat high inflation

Inflation is still expected to remain too high for too long

Past rate increases are continuing to be transmitted forcefully

Committed to bringing inflation back to target, even if it means slower economic growth.

Sources: European Central Bank, Macroeconomic Projections, Trading Economics, FXStreet

Macroeconomic Projections

The Governing Council revised its macroeconomic projections at their September meeting. They will update them again in December.

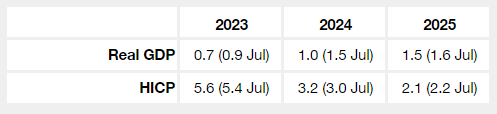

The short-term outlook for growth in the euro area has deteriorated, with GDP growth expected to slow down from 3.4% in 2022 to 0.7% in 2023.

Growth is expected to pick up in 2024 and 2025, but will remain below the pre-pandemic trend.

Inflation is projected to continue to decline over the projection horizon, reaching the ECB's target of 2% in the third quarter of 2025.

ECONOMIC DATA

Gross Domestic Product (GDP)

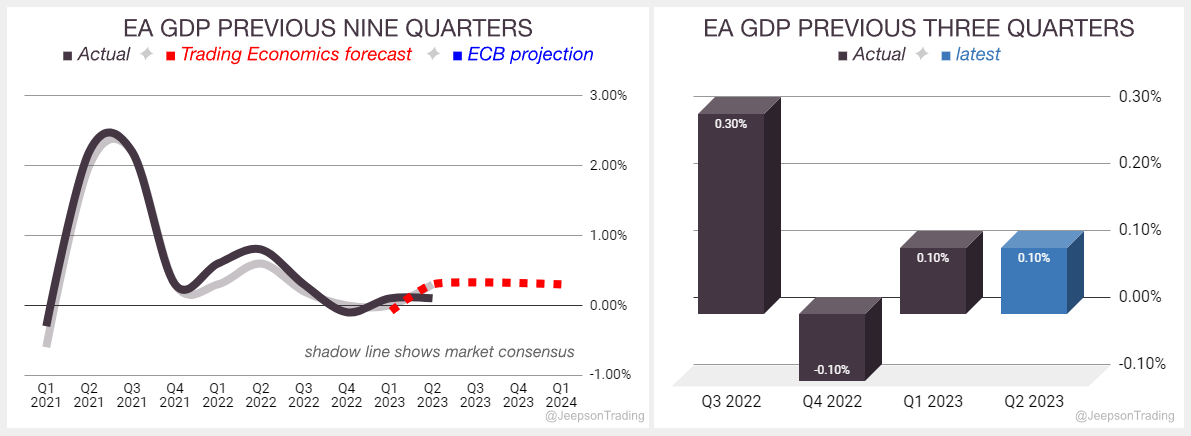

The third estimate of the quarterly change in the value of all goods and services produced across the EA during Q2 remained at 0.10%, the same as the first quarter (Q1 revised up from 0.00%), below expectations of 0.30%.

Over the previous nine quarters, the rate of growth has been trending down with a high of 2.20% and a low of -0.10%. Over the previous three quarters, the rate of growth has been falling although now stable.

The latest report is on track to achieve the Governing Council’s Real GDP 2023 growth rate projection of 0.9% (revised down from 1.0%) if the Trading Economics Q3 ‘23 forecast of 0.4% is accurate.

The next report is published on Tuesday, October 31st.

Sources: Eurostat, Trading Economics, FXStreet

Consumer Price Index (CPI)

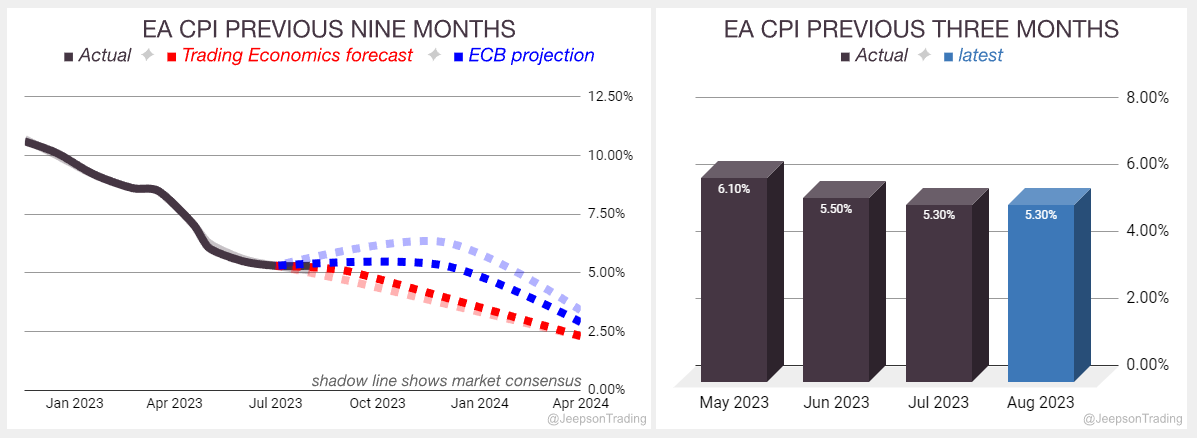

The flash estimate of the yearly change in the weighted average price of goods and services purchased by consumers across the EA during August remained at 5.3%, above expectations of 5.1%.

Over the previous nine months, CPI has been trending down with a high of 10.6% and a low of 5.3%. Over the previous three months, CPI has only slightly fallen as mostly stalled.

The latest report is on track to beat the Governing Council’s 2023 HICP rate projection of 5.3% if the Trading Economics Q3 ‘23 forecast of 5.1% (revised up from 4.7%) is accurate.

The next report is published on Tuesday, September 19th.

Sources: Eurostat, Trading Economics, FXStreet

Labour

Measures the number of people actively looking for a job as a percentage of the labour force.

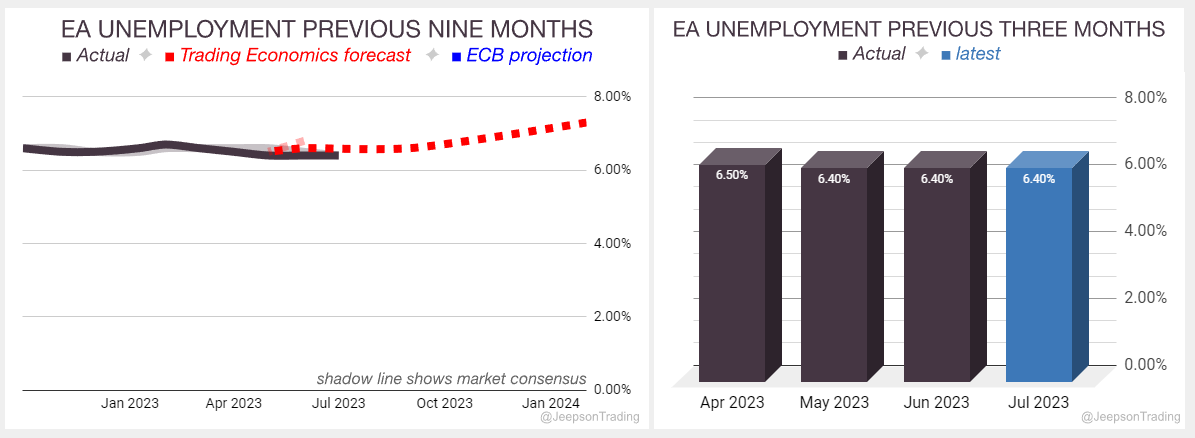

As a percentage of the labour force, unemployment across the EA for July remained at 6.4% as expected.

Over the previous nine months, unemployment has been moving sideways with a low of 6.4% and a high of 6.7%. Over the previous three months, unemployment has continued to move sideways.

The Governing Council’s have not made a labour rate projection but Trading Economics are forecasting a rise during Q3 ‘23 to 6.6%

The next report is published on Monday, October 2nd.

Sources: Eurostat, Trading Economics, FXStreet

Market Influences

Russia–EU gas dispute

The Russia-EU gas dispute caused an increase in the cost of energy which has reduced the spending power of consumers and resulted in slower economic growth. This price pressure has since significantly eased and is expected to lead to increased foreign investment in the stock market and upward support on the Euro’s value.

The EU imported 83% of its natural gas in 2021, with 50% of that coming from Russia. However, after Russia invaded Ukraine in March 2022, the EU needed to diversify its gas imports and seek out more reliable suppliers.

The global energy market is likely to become more volatile in the years to come, due to a number of factors, including the increasing demand for energy from developing countries, the growing importance of renewable energy, and the uncertainty surrounding the future of fossil fuels. Europe is debating how to separate gas prices from electricity prices so that consumers are more protected from the volatile price of gas, which has been a major driver of rising electricity prices.

2022: In the wake of Russia's invasion of Ukraine, Russia began demanding that its natural gas customers pay in rubles, rather than euros or dollars. This led to a number of European countries, including Poland, Bulgaria, and Finland, refusing to pay, and subsequently having their gas supplies cut off. Russia also cut off gas supplies to Ukraine, which was a major transit point for Russian gas to Europe. These events have had a significant impact on the European energy market, causing gas prices to skyrocket and raising concerns about energy security.

2023: Europe has turned to LNG imports as pipeline gas fell and some LNG terminals are fully booked. With EU gas storage near full, prices have fallen to around €30/MWh from above €200 in 2022. Some companies have begun to store gas in Ukraine.

Russian Invasion of Ukraine

The war is having a detrimental effect on the global and EA economy by causing higher energy prices, supply chain disruptions, financial market volatility, refugee crisis and geopolitical uncertainty.

2021: 92,000 Russian troops are amassed at the Ukraine border and President Putin proposes a prohibition of Ukraine joining NATO which is rejected.

2022: On the 21st of February, President Putin ordered Russian forces to enter the separatist republics in eastern Ukraine and announced recognition of the two pro-Russian breakaway regions (Donetsk People's Republic and Luhansk People's Republic). NATO applied sanctions and scaled them up as the war progressed. Ukraine mounted a counter-offensive which regained lost territory and as winter arrived, a stalemate began.

2023: Russian began a new offensive in January although gained little ground. In early June, Ukraine began its counteroffensive although progress has been slow even as Russia faced mutiny from the short-lived Wagner rebellion. During late August, Denmark announced the supply of nineteen F-16 fighter jets to Ukraine with the first batch of six arriving in 2023.

Gavin Pearson

Retail trader since 2008

Specialises in forex G7 currencies

Funded account from the5ers.com

Member of the eToro Popular Investors Program

Regular contributor to FXStreet.com analysis and education pages

Jeepson Trading Fund

Returned 27% in 2022 and 5.8% in 2023 H1

Forex focused

Copy Trading available at eToro

eToro

eToro is a social trading platform

Users can copy trades by clicking the "Copy" button on the profile page

Disclaimer

Past performance is not indicative of future results

Trading involves risk, and you could lose money

-end-