Euro moving to the upside, supported by peak rate sentiment

Euro Currency Report -November (GDP, CPI update)

Derbyshire, UK – October 2nd, 2023: This is the currency report for the Euro and is intended to be a reference aid for your own analysis and trade planning. The next update will be after the unemployment rate on Friday, November 3rd.

Trading involves a possibility of losing money therefore all decisions in market speculation are undertaken at your own financial risk.

Euro moving to the upside, supported by peak rate sentiment

The euro made marginal gains in October against the dollar, but both currencies remain under selling pressure. The DAX index has started to recover from its recent lows, but the outlook is still pessimistic as German six-month bond yields have started to slip.

The ECB kept interest rates unchanged in October, as expected, given the cautious economic outlook. A contraction was seen in Q3 as inflation fell at a faster pace. Unemployment is stable.

The economic outlook for the Euro Area is mixed as although there are signs of improvement, there are also risks.

Euro and Dollar Under Selling Pressure

EUR/USD made marginal gains in October, rising just 1.30% and indicative of both currencies coming under selling pressure. Euro sellers are concerned about growth in the euro-area, while dollar sellers evaluate the Fed being close to, or at the end of its hiking cycle.

Upside moves towards 1.069 are possible if market sentiment focuses on the slowing US economy and leads investors to believe that the Fed may cut sooner. The long-term resistance level is in the 1.12 area.

Downside moves towards 1.045 are possible if the US economy outperforms expectations and, or inflation remains high. The long-term support level is in the 0.97 area.

The German stock market index (DAX) has been trading in a bearish trend, indicating a pessimistic outlook. However, the DAX has recently started to recover, bouncing from the 14,700 level.

The yield on German six-month bonds has also been slowly trending higher, indicating a pessimistic outlook. However, the yield has recently started to slip and is testing the 50-day moving average.

The European Central Bank (ECB) kept interest rates unchanged on October 26, 2023, as expected, given the recent drop in inflation from its peak. However, inflation remains high, and the ECB is committed to bringing it back to its 2% target. The bank will continue to monitor data to inform its future monetary policy decisions.

The ECB's decision is a sign of caution about the economic outlook, given the impact of the war in Ukraine and the rising cost of living. The bank is also aware that raising interest rates too quickly could lead to a recession.

Overall, the ECB's decision is likely to have a slightly positive impact on the economy, as it removes the risk of rising borrowing costs for businesses and consumers, which could boost economic growth.

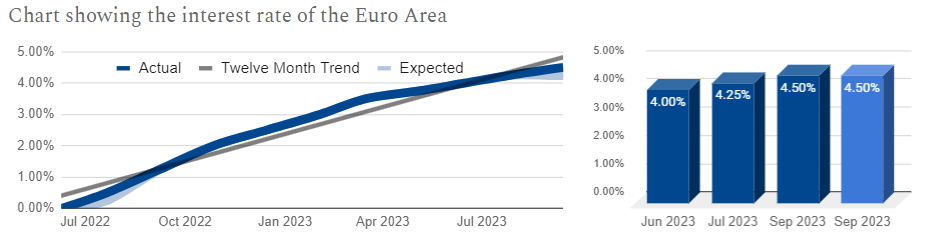

ECB Holds Rates Steady Amidst Growth Concerns

The six members of the European Central Bank’s (ECB) Governing Council (plus nineteen governors from the national banks of the countries using the euro) set monetary policy, including the Main Refinancing Operations rate (interest rate). The main refinancing operations rate is the interest rate that banks pay to borrow money from the ECB overnight and is secured by bonds. This rate affects the interest that banks charge their borrowers.

The governing council meets to set monetary policy eight times a year, the latest was October 26th and the next is on December 14th.

The interest rate of the EA was held at the October meeting to end the hiking cycle of 10 consecutive meetings. This ECB remains hawkish and although their focus remains on stamping out high inflation, they are increasingly more observant of the impact rates are having on growth. Trading Economics forecast 4.50% to be the peak rate and cuts to 4.00% to happen during 2024.

Key points of the ECB’s Governing Council October 2023 meeting:

Rates unchanged at 4.50%, 4.75%, and 4.00% for the main refinancing operations, the marginal lending facility, and the deposit facility, respectively.

Inflation dropped markedly in September, including due to strong base effects, and most measures of underlying inflation have continued to ease.

Data-dependent approach to determining the appropriate level and duration of restriction.

Sources: European Central Bank, Macroeconomic Projections, Trading Economics, FXStreet

The Economy is Slowly Growing but has a Mixed Outlook

The ECB’s Governing Council makes macroeconomic projections four times a year. The most recent was at their September meeting and they will be updated in December.

Annual Real GDP has a pessimistic outlook compared to the Governing Councils forecast and shows a contraction is likely.

Annual HICP has an optimistic outlook compared to the Governing Councils forecast and is on track to come in below expectations.

The Euro Area economy contracted in Q3 2023, with GDP growth falling to -0.1%. This is below expectations and raises the risk of a recession. The contraction was driven by a sharp decline in retail sales and a slowdown in manufacturing activity.

Inflation also fell at a faster pace in October, with the annual inflation rate dropping to 2.9%. This is below expectations and is reflective of reduced demand as the higher cost of living is hurting the purchasing power of consumers.

The unemployment rate remained stable in August, at 6.4%. This suggests that businesses are maintaining employment levels. However, Trading Economics is forecasting a slight increase in the unemployment rate in Q4, to 6.8%.

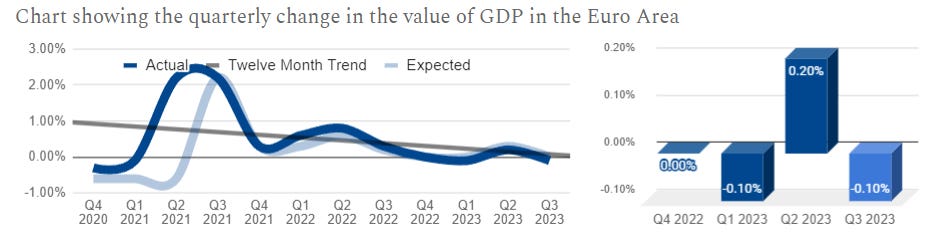

Economy returns to contraction in Q3, recovery expected in Q4

The EA GDP quarterly rate report measures the change in value of goods and services produced in the EA over a given month compared with the previous. The latest data covers the Q3 period and was published on October 31st by Eurostat and the next version is out on November 14th.

The latest result of -0.10% was below expectations and signals that the economy has contracted and is at significant risk of recession, it is lower than the previous quarters expansion (slightly revised up) and below the baseline trend.

Trading Economics are forecasting 0.2% for Q4 (prev. 0.4) which would be above the baseline trend of 0.00% and suggest optimism with regards to economic growth.

Sources: Eurostat, Trading Economics, FXStreet

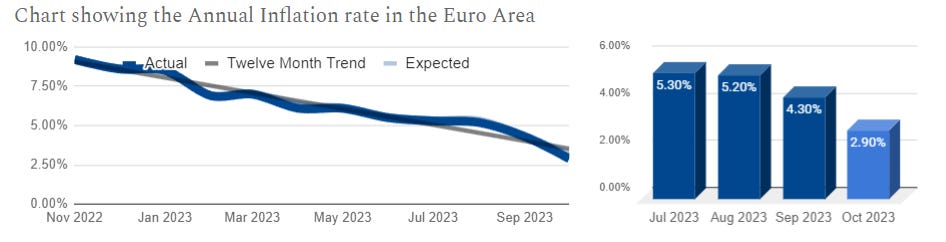

Falling inflation quickens again in October, applies bearish pressure to Q4 growth expectations

The EA inflation rate report measures the change in value of a basket of goods and services in the EA over a given month compared with the previous. The latest data covers the October period and was published on October 31st by Eurostat and the next version is out on November 17th.

The latest result of 2.90% was below expectations and signals that the falling rate of inflation is picking up pace as it is a sharp fall from the previous month and below the baseline trend. This applies bearish pressure to the economic outlook as demand falls and businesses compete for fewer customers. However, it could also be a sign that supply chains are improving.

Trading Economics are forecasting 3.60% for Q4 which would be above the baseline trend of 3.1% and suggest that the speedier pace of falling inflation will stall and reverse.

Sources: Eurostat, Trading Economics, FXStreet

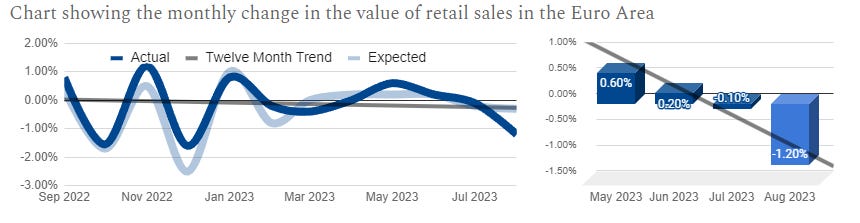

Falling retail sales quickens and applies bearish pressure to growth

The EA retail sales report measures the change in value of aggregated retail goods and services sales over a given month compared with the previous. The latest data covers the August period and was published on October 4th by Eurostat and the next version is out on November 8th.

The latest result of -1.20% was far below expectations and signals that the falling rate of retail sales is picking up pace as it is a very sharp fall from the previous month and far below the baseline trend. This applies bearish pressure to the economic outlook as consumers spend less.

Trading Economics are forecasting 0.6% for Q4 which would be below the baseline trend of -0.3% and suggest optimism with regards to a rebound of falling sales.

Sources: Eurostat, Trading Economics, FXStreet

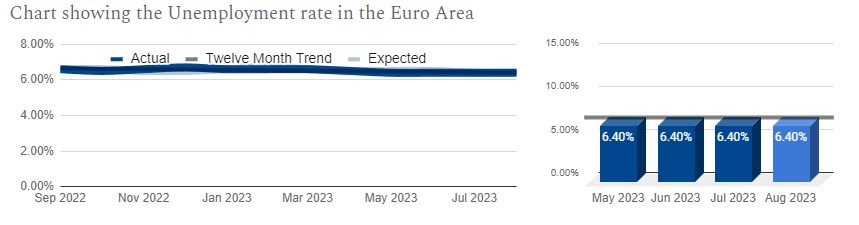

Stable unemployment remains steady and applies indifferent pressure to growth

The EA unemployment rate report measures the number of people actively looking for a job as a percentage of the labour force over a given month. The latest data covers the August period and was published on October 2nd by Eurostat and the next version is out on November 3rd.

The latest result of 6.40% was as expected and signals that the stable rate of unemployment continues as it is the same as the previous month and the same as the baseline trend. This applies indifference to the economic outlook as businesses maintain employment levels.

Trading Economics are forecasting 6.8% (revised down from 7.0%) for Q4 which would be below the baseline trend of 6.3% and suggest some pessimism with regards to a stable labour market.

Sources: Eurostat, Trading Economics, FXStreet

The Russia-EU gas dispute and the war in Ukraine are having a significant impact on the European economy, causing gas prices to soar and putting upward pressure on inflation and economic growth.

Europe is working to reduce its reliance on Russian gas, but the impact of the gas dispute and the war is likely to continue in the near term. However, there are some signs that the situation may improve in the medium term, as Europe diversifies its energy sources.

Russia-EU Gas Dispute Applies Upwards Pressure to Inflation

The Russia–EU gas dispute flared up in March 2022 following the invasion of Ukraine. Russia cut the flow of gas to Europe significantly, and in September 2022, it stopped it altogether. As of August 2023, Russian pipeline gas exports continued to flow to some EU countries and non-EU countries in Europe, but the flow was significantly reduced from pre-war levels. Europe also imported record volumes of liquefied natural gas (LNG) from Russia in 2022.

Recent Key Events

Russia has cut gas supplies to Europe significantly since April 2022, and stopped them altogether to Poland, Bulgaria, Finland, and Ukraine.

Russia has also reduced gas flows via the Nord Stream 1 pipeline, citing technical difficulties.

In September 2022, the Nord Stream 1 and 2 pipelines ruptured, likely due to sabotage.

European countries have been working to secure alternative gas supplies, including from Norway, Qatar, and the United States.

EU gas prices have soared in response to the disruptions, but have fallen in recent months as storage levels have increased.

The gas delivery disruptions have had a significant impact on the European economy, as gas is a key source of energy for many industries and households.

Russian Invasion of Ukraine Adds Uncertainty

On February 24, 2022, Russia invaded Ukraine in an escalation of the Russo-Ukrainian War which began in 2014. The invasion is the largest military conflict in Europe since World War II and has resulted in tens of thousands of casualties on both sides. The invasion has also caused a humanitarian crisis, with millions of Ukrainians displaced from their homes. The international community has condemned the invasion and imposed sanctions on Russia. The International Criminal Court is investigating possible war crimes and crimes against humanity committed by Russian forces.

Recent Key Events

June 2023: The Ukrainian counteroffensive in June 2023 made significant progress, with Ukraine liberating villages and reclaiming territory in the eastern Donbas region. The Wagner Group's rebellion against the Russian government was a major setback for Russia.

August 2023: Ukraine counteroffensive slowed by millions of mines laid by Russia. Ukrainian drones damage the Russian landing ship Olenegorsky Gornyak.

September: An attack on Russian naval targets in Sevastopol damages the Black Sea fleet. Several oil and gas drilling platforms on the Black Sea held by Russia since 2015 have been retaken.

The war in Ukraine is having a negative impact on the global economy, including the value of the Euro. The war has caused energy prices to soar and disrupted supply chains, which are putting upward pressure on inflation and weighing on the EA economy.

Gavin Pearson

Retail trader since 2008

Specialises in forex G7 currencies

Funded account from the5ers.com

Member of the eToro Popular Investors Program

Regular contributor to FXStreet.com analysis and education pages

Returned 27% in 2022 and 5.8% in 2023 H1

Forex focused

Copy Trading available at eToro

Disclaimer

Past performance is not indicative of future results

Trading involves risk, and you could lose money

-end-