Euro outlook sees downside momentum, pressured by a stronger USD and geopolitical uncertainty

Euro Currency Report October

Derbyshire, UK – October 16th, 2023 - This is the currency report for the Euro and is intended to be a reference aid for your own analysis and trade planning. This update contains the latest data for retail sales which are reflective of a slowdown and unemployment which remains steady. The next update will be after the EA inflation data on Wednesday, October 18th, or before if any significant event occurs.

Decisions to trade are made at your own monetary risk.

Euro outlook to see downside momentum, pressured by a stronger USD and geopolitical uncertainty

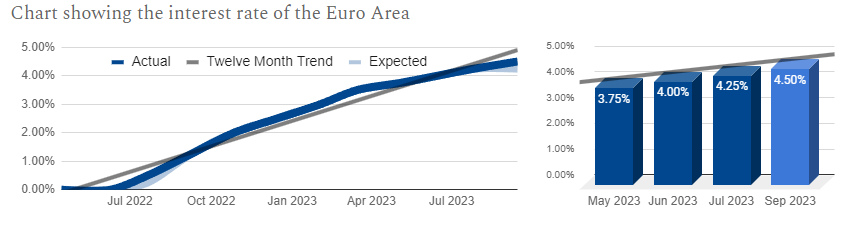

Monetary Policy provides upside momentum for EUR: The ECB has raised rates to 4.50% in September and is maintaining its hawkish policies which involve rates being higher for longer.

Market narratives provide downside momentum for EUR: The US economy remains resilient which is supportive of higher rates from the Fed and keeps the dollar in demand.

Macroeconomics provides mixed momentum for EUR: Analysis indicates that the EA economy is at risk of recession but unemployment levels remain stable enough to possibly avert this crisis.

Geopolitics provides downside momentum for EUR: The ongoing conflicts have an uncertain outlook and investors are averse to risky holdings in favour of safe-havens such as the US dollar.

Monetary Policy

In the Euro Area, the benchmark interest rate is set by six members of the Governing Council plus nineteen governors from the national central banks of the countries using the euro.

Interest Rates Hiked, ECB Target Inflation Over Growth

The six members of the European Central Bank’s (ECB) Governing Council (plus nineteen governors from the national banks of the countries using the euro) set monetary policy, including the Main Refinancing Operations rate (interest rate). The main refinancing operations rate is the interest rate that banks pay to borrow money from the ECB overnight and is secured by bonds. This rate affects the interest that banks charge their borrowers.

The governing council meets to set monetary policy eight times a year, the latest was September 14th and the next is on October 26th.

The interest rate of the EA was hiked at the September meeting by 0.25% after also being hiked by 0.25% in August and throughout almost all of the previous twelve meetings. This indicates that the ECB is hawkish and is focused on stamping out the high rate of inflation. Trading Economics forecast 4.50% to be the peak rate and 2024 to see cuts of 0.75%.

Key points of the ECB’s Governing Council September 2023 meeting:

Raised its key interest rates by 25 basis points in order to bring inflation back to its 2% medium-term target.

Expects inflation to average 5.6% in 2023, 3.2% in 2024 and 2.1% in 2025.

Rate increase is likely to dampen economic growth, which is now expected to be 0.7% in 2023, 1.0% in 2024 and 1.5% in 2025.

Will keep interest rates at restrictive levels for as long as necessary to bring inflation back to target.

Sources: European Central Bank, Macroeconomic Projections, Trading Economics, FXStreet

The Economy is Slowly Growing but has a Mixed Outlook

The ECB’s Governing Council makes macroeconomic projections four times a year. The most recent was at their September meeting and they will be updated in November.

Annual Real GDP has a pessimistic outlook compared to the Governing Councils forecast and shows a contraction is likely.

Annual HICP has an optimistic outlook compared to the Governing Councils forecast and is on track to come in below expectations.

Market Narratives

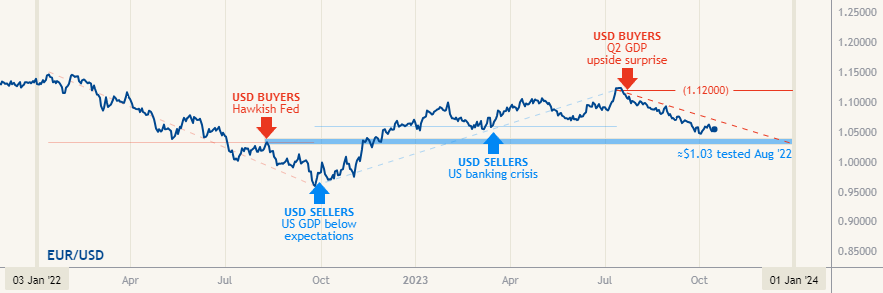

US Economic Strength provides downside pressure to the EUR/USD

Late July 2023: in late July, the Fed remained on their hawkish path with the Fed fund rate being hiked by 0.25% to 5.5%. The next day saw a significant upside surprise in GDP for Q2 at 2.4% which indicated that the US economy is resilient to recent hikes and a wave of dollar buying began as the ‘higher-for-longer’ narrative took hold. There have been no retracements since.

Economic Indicators

Outlook for Growth Shows that Slowing Economy May Rebound

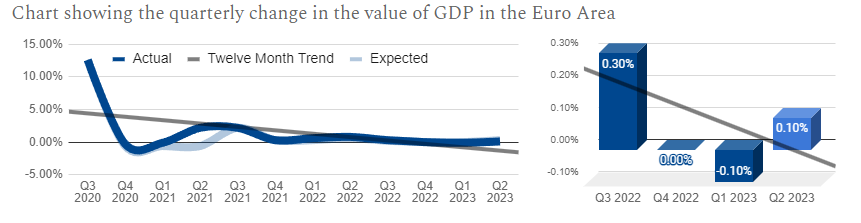

The EA GDP quarterly rate report measures the change in value of goods and services produced in the EA over a given month compared with the previous. The latest data covers the Q2 period and was published on September 7th by Eurostat and the next version is out on October 31st.

The quarterly rate of GDP in the EA has been falling quickly over the past four months although recently rebounded, after being mostly neutral for the previous year. This indicates that the economy is slowing and is at risk of recession.

The Q2 growth rate of 0.10% was higher than Q1’s -0.10%, and bucked the recent downtrend. The forecasting model predicts 0.2% growth during Q3, which would also be above the recent downtrend and suggests that a recession could be avoided. Trading Economics are far more optimistic, with a forecast of 0.4%.

Sources: Eurostat, Trading Economics, FXStreet

Outlook for Inflation Signals a Light Headwind for Growth

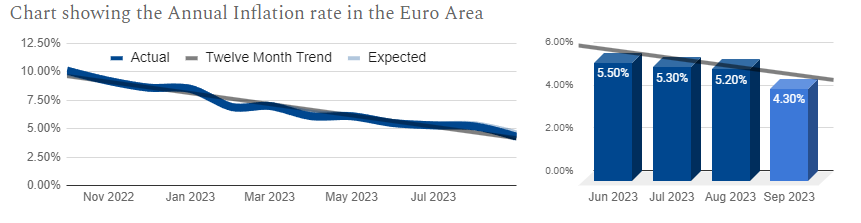

The EA inflation rate report measures the change in value of a basket of goods and services in the EA over a given month compared with the previous. The latest data covers the August period and was published on September 29th by Eurostat and the next version is out on October 18th.

EA prices have been steady over the past four months although recently fell sharply, continuing the rapid fall of the previous year. This suggests that the economy is slowing down, as demand falls and businesses compete for fewer customers. However, it could also be a sign that supply chains are improving.

September’s inflation rate of 4.3% was far lower than August’s 5.2% and was much lower than the trendline. However, the forecasting model predicts 5.0% for September while Trading Economics are forecasting 4.3% by December. This suggests that the recent rapid fall is not expected to continue and prices may stabilise from here through to the end of the year.

Sources: Eurostat, Trading Economics, FXStreet

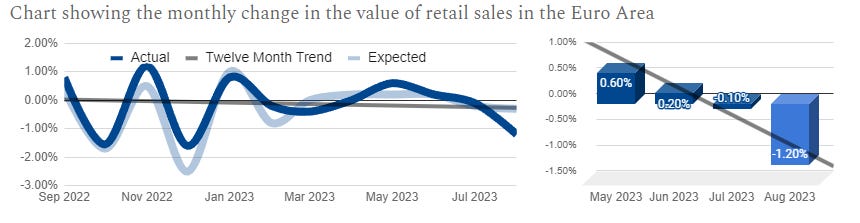

Outlook for Retail Sales Signals a Light Headwind to Growth

The EA retail sales report measures the change in value of aggregated retail goods and services sales over a given month compared with the previous. The latest data covers the August period and was published on October 4th by Eurostat and the next version is out on November 8th.

EA sales have significantly declined over the past four months, reversing the volatile but flat trend seen over the previous year. This is a sign of a slowing economy, as consumers tighten their belts amid the cost of living crisis and rising interest rates.

September's inflation rate of 3.70% matched the rate in August’s. The forecasting model correctly predicted inflation of 3.7% for September and 3.7% again for October. This would see a stabilisation of prices, suggesting that the rate of inflation is steady. Trading Economics are far more optimistic, with a forecast of 3.0% by the end of Q4.

August sales (-1.2%) showed a deterioration over July (-0.10%) and fell far below the recent downtrend. The trend-following forecast model incorrectly predicted sales of 0.0% for September and is now forecasting sales of 0.5% for October. Trading Economics are even more optimistic, with a forecast of 0.6% by the end of Q4.

Sources: Eurostat, Trading Economics, FXStreet

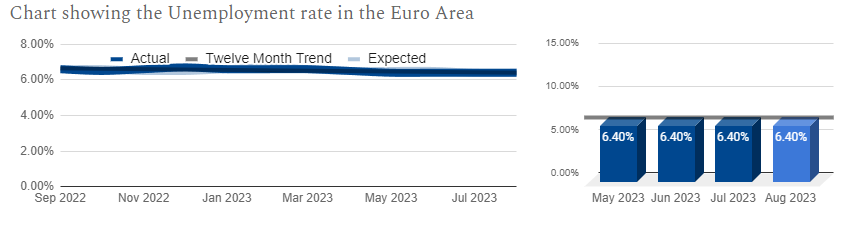

Outlook for Unemployment Signals a Calm Tailwind to Growth

The EA unemployment rate report measures the number of people actively looking for a job as a percentage of the labour force over a given month. The latest data covers the August period and was published on October 2nd by Eurostat and the next version is out on November 3rd.

EA unemployment has been stable over the past four months, continuing the stable trend seen over the previous year. This is a sign of a stable economy, as businesses maintain employment levels.

August’s unemployment of 6.4% matched July’s 6.4% in line with the flat trend. The trend-following forecast model correctly predicted 6.4% for September and is now forecasting 6.2% for October which seems too optimistic. Trading Economics have a forecast of 7.0% by the end of Q4.

Sources: Eurostat, Trading Economics, FXStreet

Geopolitical Events

Russia-EU Gas Dispute Applies Upwards Pressure to Inflation

The Russia–EU gas dispute flared up in March 2022 following the invasion of Ukraine. Russia cut the flow of gas to Europe significantly, and in September 2022, it stopped it altogether. As of August 2023, Russian pipeline gas exports continued to flow to some EU countries and non-EU countries in Europe, but the flow was significantly reduced from pre-war levels. Europe also imported record volumes of liquefied natural gas (LNG) from Russia in 2022.

Recent Key Events

Russia has cut gas supplies to Europe significantly since April 2022, and stopped them altogether to Poland, Bulgaria, Finland, and Ukraine.

Russia has also reduced gas flows via the Nord Stream 1 pipeline, citing technical difficulties.

In September 2022, the Nord Stream 1 and 2 pipelines ruptured, likely due to sabotage.

European countries have been working to secure alternative gas supplies, including from Norway, Qatar, and the United States.

EU gas prices have soared in response to the disruptions, but have fallen in recent months as storage levels have increased.

The gas delivery disruptions have had a significant impact on the European economy, as gas is a key source of energy for many industries and households.

Russian Invasion of Ukraine Adds Uncertainty

On February 24, 2022, Russia invaded Ukraine in an escalation of the Russo-Ukrainian War which began in 2014. The invasion is the largest military conflict in Europe since World War II and has resulted in tens of thousands of casualties on both sides. The invasion has also caused a humanitarian crisis, with millions of Ukrainians displaced from their homes. The international community has condemned the invasion and imposed sanctions on Russia. The International Criminal Court is investigating possible war crimes and crimes against humanity committed by Russian forces.

Recent Key Events

June 2023: The Ukrainian counteroffensive in June 2023 made significant progress, with Ukraine liberating villages and reclaiming territory in the eastern Donbas region. The Wagner Group's rebellion against the Russian government was a major setback for Russia.

August 2023: Ukraine counteroffensive slowed by millions of mines laid by Russia. Ukrainian drones damage the Russian landing ship Olenegorsky Gornyak.

September: An attack on Russian naval targets in Sevastopol damages the Black Sea fleet. Several oil and gas drilling platforms on the Black Sea held by Russia since 2015 have been retaken.

The war in Ukraine is having a negative impact on the global economy, including the value of the Euro. The war has caused energy prices to soar and disrupted supply chains, which are putting upward pressure on inflation and weighing on the EA economy.

Gavin Pearson

Retail trader since 2008

Specialises in forex G7 currencies

Funded account from the5ers.com

Member of the eToro Popular Investors Program

Regular contributor to FXStreet.com analysis and education pages

Jeepson Trading Fund

Returned 27% in 2022 and 5.8% in 2023 H1

Forex focused

Copy Trading available at eToro

eToro

eToro is a social trading platform

Users can copy trades by clicking the "Copy" button on the profile page

Disclaimer

Past performance is not indicative of future results

Trading involves risk, and you could lose money

-end-