EUR/USD's Perfect Storm: Politics, Policy, and Protectionism

Sunday, 17 November 2024 (Week 46)

As we begin the week, traders are focusing on several critical upcoming events that could shape the euro's trajectory, particularly Wednesday's ECB President Lagarde's speech and Friday's Flash PMI data. These events take on added significance given last week's ECB meeting accounts which revealed growing consideration of rate cuts, and the recent market turbulence following Trump's election victory.

Trade Tensions and Political Upheaval

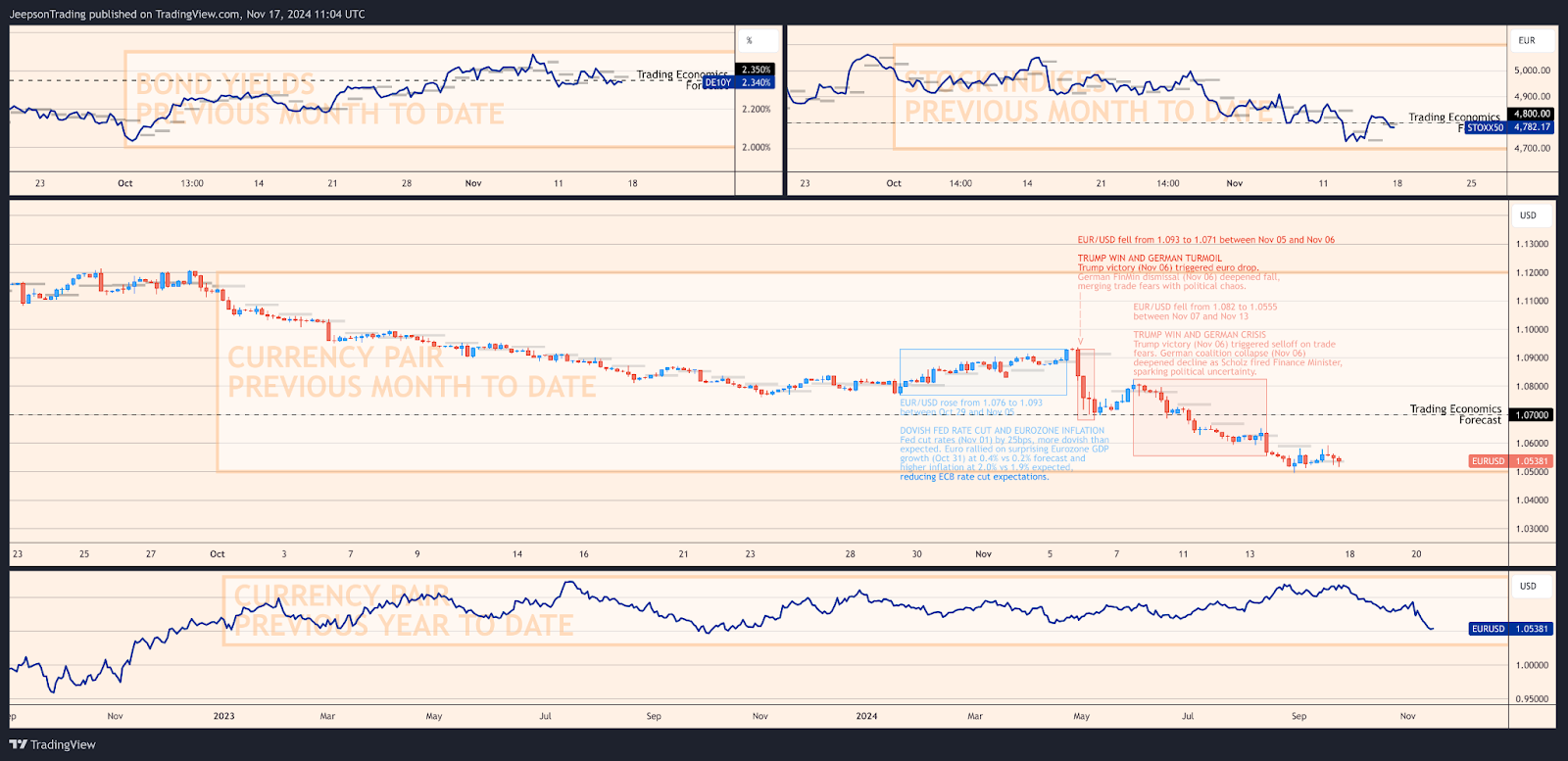

The re-election of Donald Trump has fundamentally shifted market dynamics in the Eurozone. The euro fell sharply to 1.0539 against the dollar by November 15, marking its lowest level since July. This decline reflects mounting concerns over Trump's proposed trade policies, particularly their potential impact on the Eurozone's export-driven economy. European automotive stocks have borne the brunt of these concerns, declining 3.2% on November 14 as markets priced in the risk of new tariffs on European vehicles.

Trump's proposed 60% tariffs on Chinese goods and potential automotive tariffs pose significant risks to the Eurozone economy, where manufacturing exports constitute 40% of total exports. The automotive sector, representing 7.1% of Eurozone GDP, appears particularly vulnerable, while the chemical industry, at 5.4% of GDP, faces similar challenges under potential new trade barriers.

Emerging Theme

Political instability in Germany has emerged as a critical concern following the collapse of the coalition government on November 12. The prospect of snap elections in February 2025 has created additional uncertainty in the Eurozone's largest economy. This political turmoil has manifested in declining business confidence, with the Ifo index falling to 86.5 in October, while the ZEW Economic Sentiment indicator dropped to 7.4 in November.

Geopolitics: Complex Crossroads

The Eurozone's position as the world's largest trading bloc, with trade representing 85% of GDP, makes it particularly susceptible to shifts in global trade policy. The immediate aftermath of Trump's victory saw an intensification of trade concerns, with the euro declining 1.2% on November 6 following his victory speech emphasising protectionist policies.

The German political crisis has added another layer of complexity to the geopolitical landscape. The dismissal of the Finance Minister and subsequent coalition collapse triggered a 2.3% decline in the DAX index and pushed the euro down 0.8% against major currencies between November 12 and 15.

Central Bank and Monetary Policy: Balancing Act

The European Central Bank, maintaining its deposit rate at 3.40% following October's 25 bps cut, faces mounting pressure to respond to deteriorating economic conditions. Recent signals from the ECB indicate growing consideration of further rate cuts, with markets now fully pricing in a 25 bps reduction at the December 12 meeting.

The central bank must balance these easing pressures against persistent inflation concerns, with core inflation holding steady at 2.7% and services inflation remaining elevated at 3.9% in October. The upcoming Monetary Policy Meeting Accounts will be crucial in understanding the ECB's approach to these competing pressures.

Economic Indicators: Mixed Signals

Economic data from the Eurozone presents a complex picture. Third-quarter GDP growth accelerated to 0.4% quarter-over-quarter, doubling the previous quarter's 0.2% expansion and triggering a 0.3% rise in EUR/USD. However, manufacturing remains in contraction territory, with the PMI at 46.0 in October, despite showing modest improvement from September's 45.0 reading.

Inflation data revealed headline inflation reaching the ECB's 2% target in October, up from September's 1.7%, though this headline figure masks persistent underlying pressures in core inflation. The next critical data points include Flash PMIs on November 22 and inflation figures on November 29.

Inter-markets: Cross-Asset Dynamics

The STOXX 50 has gained 6.06% year-to-date, with recent performance showing significant sector divergence. While banking stocks demonstrated resilience with a 2.1% gain on November 15, the automotive sector's 3.2% decline reflects mounting trade concerns. According to Trading Economics' forecasts, the EU50 is expected to trade at 4,843.70 points by the end of Q4 2024, with a longer-term projection of 4,657.22 points in 12 months.

In fixed income markets, the German 10-year Bund yield has climbed to 2.34%, with the spread against US Treasuries widening to -186 basis points. This spread widening reflects diverging monetary policy expectations between the ECB and Federal Reserve. Forecasts suggest the German 10-year yield will trade at 2.35% by year-end 2024, before declining to 2.23% by Q4 2025, indicating an expected moderation in yields as monetary policy easing takes effect.

The energy market's dynamics remain crucial for the Eurozone inflation outlook, with natural gas prices stabilising below €39.4 per megawatt-hour, significantly down from October's peaks. This moderation in energy costs could support the ECB's ability to implement policy easing in the coming months.

The Currency: EUR/USD at Critical Juncture

The euro trades at 1.0539, having recorded a monthly decline of 1.8%. According to Trading Economics' forecasts, EUR/USD is expected to trade at 1.07 by the end of Q4 2024, with a longer-term projection of 1.05 by Q4 2025. These projections reflect expectations of ECB rate cuts and ongoing economic challenges in the Eurozone.

Near-term technical analysis identifies crucial support levels at 1.0500 and 1.0450, with resistance established at 1.0700 and 1.0850. The 1.0400 level represents a critical threshold that could trigger accelerated selling if breached. Current market positioning shows Asset Managers maintaining significant net long positions of 237,960 contracts, while Leveraged Funds hold net long positions of 49,615 contracts.

The upcoming economic calendar could significantly impact these forecasts, with particular attention on:

ECB President Lagarde's Speech (Nov 20)

Flash PMIs (Nov 22)

Flash Inflation Data (Nov 29)

ECB Rate Decision (Dec 12)

The bearish sentiment prevailing in the market stems from a confluence of factors: the expected continuation of ECB rate cuts, with markets pricing in a reduction to 2.40% by 2025, political uncertainty in Germany, and growing trade tensions following Trump's election victory.

Conclusion

Three key takeaways emerge from this analysis. First, German political instability adds significant uncertainty to the EUR/USD outlook. Second, the ECB's increasingly dovish stance is likely to accelerate given weak economic data. Third, trade tensions pose a major risk to the export-dependent Eurozone economy.

Sources: ECB, Eurostat, S&P Global, Trading Economics, Bloomberg, Reuters.