Forex Market Strategic Outlook: July 2026

Read This Before You Trade Today

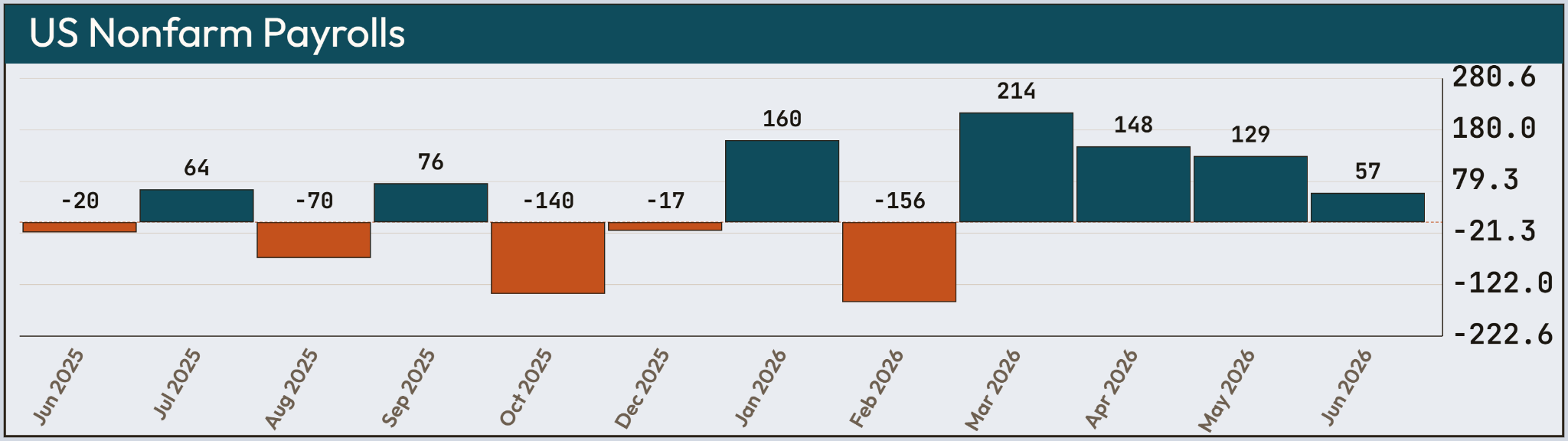

June was dominated by a sharp escalation in the Middle East. Missile strikes between the US and Iran effectively shut down the Strait of Hormuz, sending Brent crude soaring. That surge completely overshadowed the Bank of Japan’s rate hike to 1.0% on June 16, pushing the yen down near 40-year lows. Meanwhile, the US dollar lost its usual safe-haven boost after a weak jobs report on July 2 showed Nonfarm Payrolls at just 57k against a 110k forecast.

Looking through July and into October, the main story is an energy-driven split in central bank policy. How central banks respond depends entirely on how well their domestic economies can handle high oil prices. Right now, the two best setups to trade this gap are Long NZD/JPY (+72.0 FSS delta) and Short AUD/NZD (-55.0 FSS delta).

The Strait of Hormuz Shock and Central Bank Divide

The blockade of the Strait of Hormuz is driving global markets right now. US and Iranian missile attacks throughout June and early July forced ships to avoid the Persian Gulf, triggering a massive spike in energy costs. This acts like a heavy tax on global growth and revives headline inflation.

The Bank of Japan tried raising interest rates to 1.0% from 0.75% on June 16. It did not help. The yen plummeted to 163 against the dollar because Japan imports almost all of its energy, leaving it exposed to rising oil.

Higher energy prices are splitting central banks into two groups: those raising rates to protect their currencies, and those stuck on the sidelines due to weak domestic growth.

The Reserve Bank of New Zealand (RBNZ) stepped up on July 8, raising its benchmark rate by 25 basis points to 2.50% to fight sticky inflation. Capital is now flowing into the Kiwi to capture those higher yields. Expect central banks with solid economic backings to keep using rate hikes as a shield against inflation over the next three months.

What Could Break the Energy Shock Thesis

The biggest risk to this setup over the next three months is a sudden peace agreement between the US and Iran.

If the Strait of Hormuz reopens and tankers start moving freely again, oil prices will drop fast. That would immediately lift import pressure off Japan, likely sparking a fast rally in the yen as traders cover short positions.

Soft US Jobs and Cool Inflation Cap the Dollar

The greenback has struggled to keep its momentum despite ongoing Middle East tensions. The main culprit is a weakening US labor market.

On July 2, US Nonfarm Payrolls came in at a weak 57k, missing the 110k estimate and falling well below the previous 129k number. Unemployment dropped slightly to 4.2%, but only because fewer people were actively looking for work. That weak job growth cooled off expectations for Federal Reserve rate hikes.

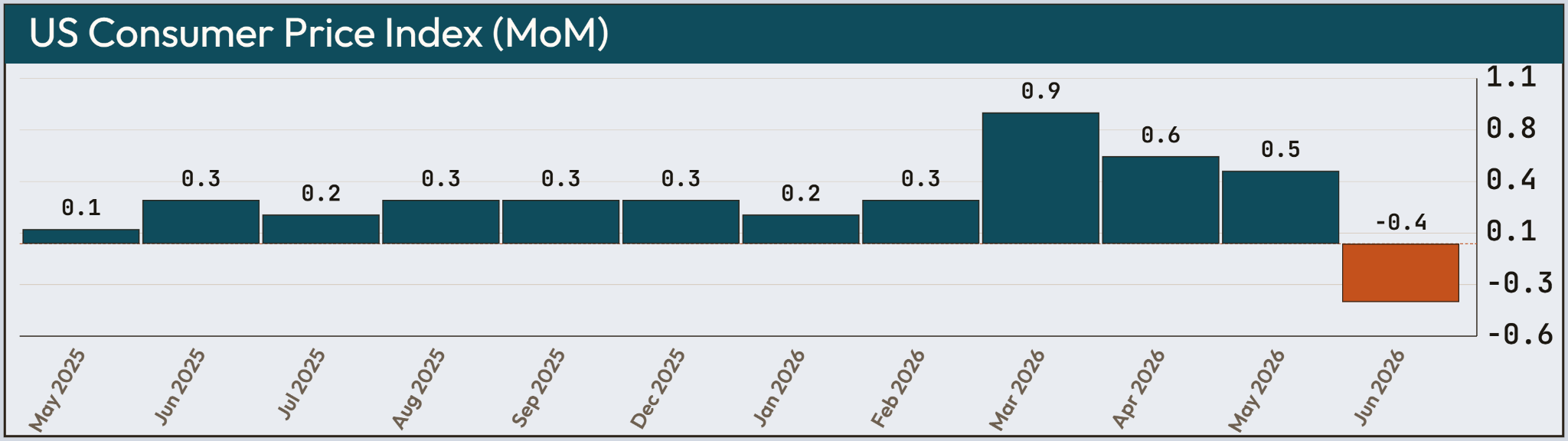

Inflation data sealed the deal on July 14. US Consumer Price Index (CPI) fell 0.4% month-over-month, surprising analysts who expected a much smaller drop of 0.1%. Annual inflation cooled to 3.5% against a 3.8% forecast.

This rare price drop showed that slowing domestic demand is currently outweighing energy shocks in the US. Federal Reserve Chair Kevin Warsh continues to sound hawkish, but the weak data limits the dollar’s upside. That makes it far more attractive to pair strong currencies against the yen rather than the dollar.

Antipodean Split: RBNZ Tightens While the RBA Holds

A clear gap has opened between Australia and New Zealand’s central banks, creating a strong cross-currency opportunity.

On June 16, the Reserve Bank of Australia (RBA) kept its cash rate unchanged at 4.35%. Even though Australia added a strong 76.3k jobs on July 23 (beating the 15k forecast), an uneven domestic economy is keeping the RBA firmly in neutral mode.

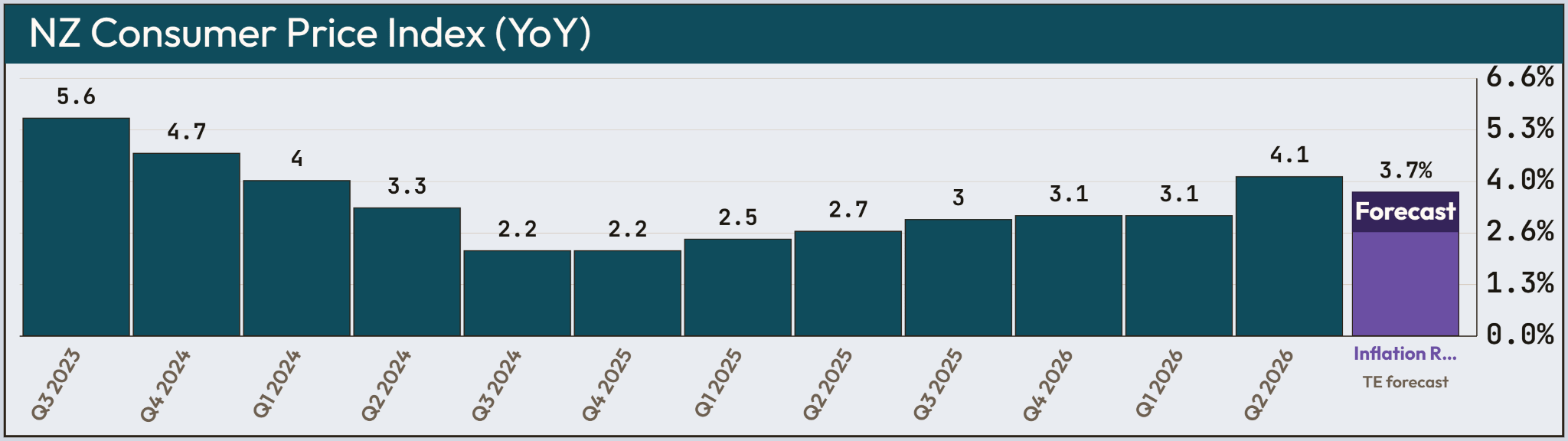

New Zealand is taking the opposite path. Following its July 8 rate hike to 2.50%, consumer prices for Q2 jumped 4.1% year-over-year on July 20, topping the 4.0% forecast.

That hot inflation print practically guarantees another 25-basis-point hike from the RBNZ by September. This difference in policy gives Short AUD/NZD strong fundamental backing through July and into the fall.

Steady Handover in the UK Keeps Sterling Stable

The British Pound has stayed surprisingly steady through a major leadership change.

Following Keir Starmer’s resignation, Andy Burnham took over as Prime Minister on July 20. Concerns about heavy spending eased quickly when John Healey was named Chancellor, stabilizing 10-year UK gilt yields near 5.0%.

The Bank of England held its policy rate at 3.75% on June 18 in a 7-2 vote. UK CPI slowed to 2.6% on July 22, but core services inflation remained sticky at 3.6%.

With a disciplined fiscal policy and a cautious central bank, the pound offers a steady base. It remains far less volatile than either the yen or the kiwi dollar.

Top Currency Focus Pairs

Long NZD/JPY

The RBNZ is raising rates into rising energy costs, while the yen continues to slide despite the Bank of Japan’s move to 1.0%. Japan’s heavy reliance on oil imports makes it vulnerable to the Hormuz blockade, whereas New Zealand’s higher yields are pulling in capital.

Base (NZD): FSS +48 (Hawkish RBNZ policy backed by 4.1% inflation).

Quote (JPY): FSS -24 (Weak energy importer struggling with high crude and slow BoJ policy).

Signal Tag: Programmatic FSS Divergence: +72.0 delta / LONG bias.

July Drivers: The RBNZ’s July 8 rate hike and hot Q2 CPI data will keep yield differentials moving in favor of the Kiwi over the yen.

3-Month Outlook: The BoJ might hike again late in the summer, but the real-yield advantage still favors New Zealand heading into October.

Trade Invalidation: A peace deal between the US and Iran that reopens the Strait of Hormuz, driving crude lower and sparking a fast yen recovery.

Short AUD/NZD

A straight divergence between two neighboring central banks. The RBNZ is actively raising rates to curb inflation, while the RBA stays on hold at 4.35% due to choppy economic performance.

Base (AUD): FSS -7 (Neutral central bank stance with mixed economic data).

Quote (NZD): FSS +48 (Active rate hikes backed by 4.1% inflation).

Signal Tag: Programmatic FSS Divergence: -55.0 delta / SHORT bias.

July Drivers: Markets will continue moving capital from the Australian Dollar to the New Zealand Dollar to grab higher yields.

3-Month Outlook: The RBA will likely hold rates again in August. Unless China rolls out aggressive economic stimulus to boost Australian exports, the Kiwi stays in control.

Trade Invalidation: A big drop in New Zealand employment data or a massive Chinese stimulus package that boosts demand for Australian commodities.