Forex Briefing (WN14 2026): Geopolitical Fury Shakes Global Markets

A geopolitical crisis in the Middle East has closed the Strait of Hormuz, spiking Brent crude oil prices past 110 USD. This energy shock, coinciding with US tariffs, has compelled central banks, inclu

Monday, March 30, 2026

Global markets are paralyzed by fear as Middle East energy shocks trigger stagflation panics! 🚨 Watch the upcoming USD Non-Farm Payrolls; another catastrophic jobs print could unleash unparalleled volatility! 💵📉

𝐖𝐇𝐀𝐓 𝐇𝐀𝐒 𝐇𝐀𝐏𝐏𝐄𝐍𝐄𝐃?

A geopolitical crisis in the Middle East has closed the Strait of Hormuz, spiking Brent crude oil prices past 110 USD. This energy shock, coinciding with US tariffs, has compelled central banks, including the Federal Reserve and ECB, to halt easing and fight imported inflation. Australia’s central bank hiked rates to 4.10% due to domestic pressures.

𝐖𝐇𝐀𝐓 𝐈𝐒 𝐇𝐀𝐏𝐏𝐄𝐍𝐈𝐍𝐆 𝐍𝐎𝐖?

Currently, markets are gripped by acute stagflationary fears. The USD sees massive safe-haven inflows, crushing risk-sensitive peers. The BoJ holds rates at 0.75%, letting JPY weaken near the 160.00 intervention line due to high energy costs. GBP suffers intense liquidation as retail sales collapse and Gilt yields spike toward 5.00%, paralyzing the BoE.

𝐖𝐇𝐀𝐓 𝐂𝐎𝐔𝐋𝐃 𝐇𝐀𝐏𝐏𝐄𝐍 𝐍𝐄𝐗𝐓?

Looking ahead, extreme cross-asset volatility is guaranteed due to the energy crisis and labor market woes. Failure to unblock the Strait of Hormuz could push oil higher, forcing central banks into hawkish repricing and benefiting the safe-haven USD. Monitor the ECB and RBA for volatility.

𝐌𝐎𝐍𝐃𝐀𝐘 March 30, 2026

Switzerland KOF Leading Indicator: Markets expect 101.1 points; a miss could slightly weaken CHF safe-haven momentum.

𝐓𝐔𝐄𝐒𝐃𝐀𝐘 March 31, 2026

Euro Area Flash CPI: Consensus forecasts 2.60 percent; hotter prints will aggressively boost EUR hawkish yield bets.

Canada Gross Domestic Product (Jan): Expected at 0.0 percent; another contraction could severely punish CAD valuations.

United Kingdom GDP Final (Q4): Confirmation of 0.1 percent growth; lack of upward revision keeps GBP heavily pressured.

𝐖𝐄𝐃𝐍𝐄𝐒𝐃𝐀𝐘 April 01, 2026

United States ISM Manufacturing PMI: Forecasted at 52.3 points; expansionary data will ease broad stagflation and recession fears.

Euro Area Manufacturing PMI Final: Expected near 51.4 points; success in expansion will support regional equity indices.

𝐓𝐇𝐔𝐑𝐒𝐃𝐀𝐘 April 02, 2026

United States Initial Jobless Claims: Consensus is 210,000 claims; sudden spikes will rapidly escalate USD labor market anxieties.

Switzerland Consumer Price Index: Forecasted at 0.6 percent year-over-year; low inflation supports SNB’s zero-rate policy stance.

𝐅𝐑𝐈𝐃𝐀𝐘 April 03, 2026

United States Non-Farm Payrolls: Forecasted at 50,000 jobs; a negative print will trigger catastrophic USD algorithmic volatility.

United States Unemployment Rate: Expected at 4.4 percent; rising joblessness guarantees intense Federal Reserve internal policy friction.

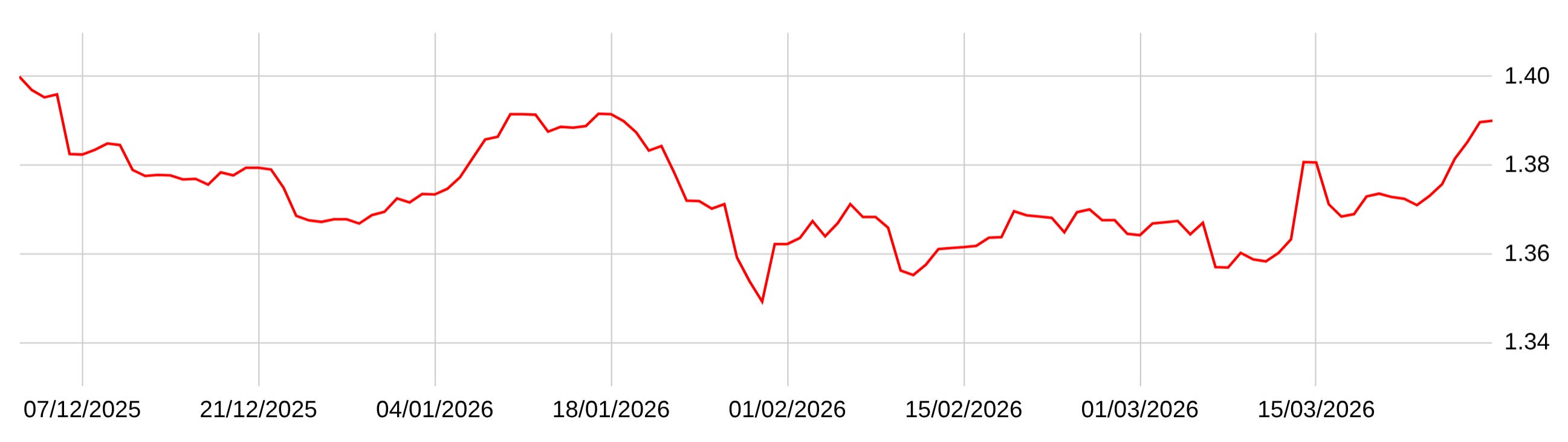

USD/CAD: UPSIDE BREAKOUT expected in the coming days due to extreme divergence between safe-haven flows and collapsing Canadian labor data.

The USD/CAD pair presents highly compelling tradeable opportunities as the USD capitalises on unprecedented global safe-haven demand, while the CAD collapses under the weight of catastrophic domestic employment contractions.

During the previous 7 months, USD/CAD trended higher as the Bank of Canada initiated easing while United States exceptionalism reigned supreme. Over the previous 7 weeks, the pair surged toward 1.3700 as Middle East energy shocks paradoxically failed to boost the CAD, which was suffocated by a devastating 84,000 domestic job loss.

For the upcoming 7 days and 7 weeks, highly convincing upside movement is expected. The Federal Reserve’s hawkish hold at 3.50 to 3.75 percent will sustain USD yields, overwhelming the Canadian economy’s annualized 0.6 percent contraction and rendering the CAD’s petro-currency status irrelevant amidst the overarching global stagflation panic.

Jan 28 2026: Bank of Canada holds rates at 2.25 percent; CAD neutral as hawkish hold pauses easing cycle.

Feb 27 2026: Canadian Q4 GDP contracts 0.6 percent annualized; USD/CAD remains bid on severe domestic weakness.

Mar 13 2026: Canadian economy sheds 84,000 jobs; CAD aggressively sold off despite surging global oil prices.

Mar 31 2026: Canada January GDP release; expected at 0.2 percent, missing this will heavily punish CAD further.

Apr 03 2026: United States Non-Farm Payrolls; a disastrous print could inject wild, unpredictable volatility into USD/CAD pricing.

Apr 10 2026: Canadian Labour Force Survey; further massive job losses will mathematically guarantee CAD depreciation momentum.

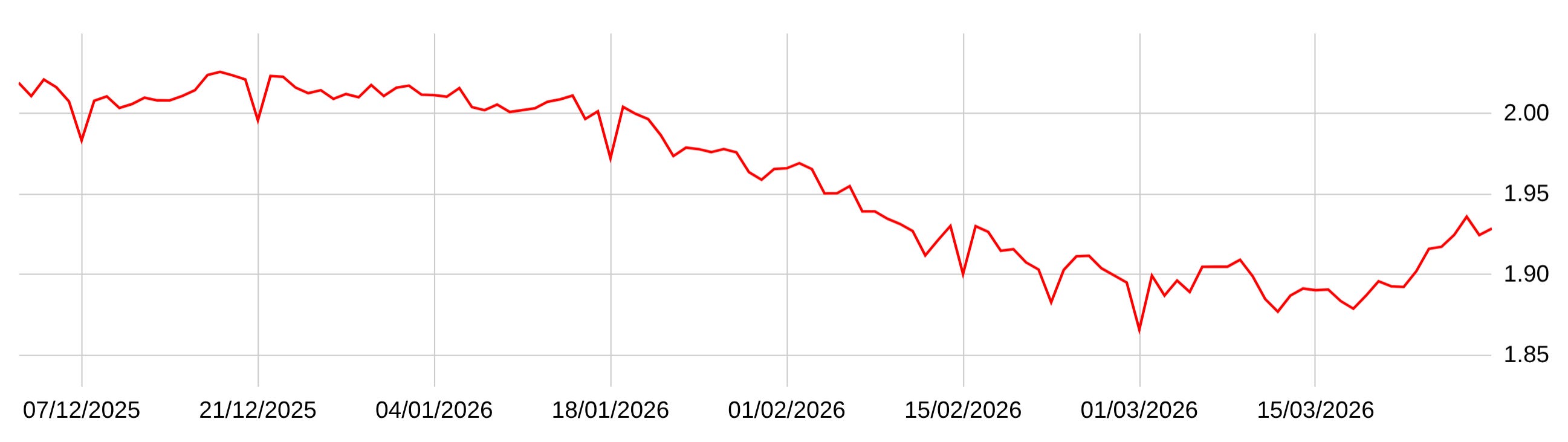

GBP/AUD: DOWNSIDE ACCELERATION expected in the coming days due to RBA rate hikes overwhelming stagflationary UK stagnation.

The GBP/AUD cross offers exceptional tradeable opportunities as the Reserve Bank of Australia’s aggressive 4.10 percent interest rate hike completely overwhelms a British economy paralyzed by stagnant growth and crushing fiscal deficits.

Over the previous 7 months, GBP/AUD experienced volatile distribution as the Bank of England cut rates to 3.75 percent while the RBA maintained a hawkish posture. During the previous 7 weeks, downside momentum accelerated aggressively after the RBA shocked markets with a 25-basis-point hike to 4.10 percent, creating a massive yield advantage.

For the upcoming 7 days and 7 weeks, highly convincing downside movement is projected. Australia’s exceptionally tight labor market and 67 percent implied probability of another rate hike will effortlessly overpower the GBP, which is fundamentally crippled by 0.1 percent growth, collapsing retail sales, and soaring Gilt yields reflecting deep stagflationary rot.

Dec 18 2025: Bank of England cuts Bank Rate to 3.75 percent; GBP weakens on dovish policy pivot.

Mar 17 2026: RBA hikes cash rate to 4.10 percent; AUD spikes aggressively on massive hawkish yield divergence.

Mar 19 2026: UK Unemployment hits 5.2 percent; GBP sold off on structural deterioration in labor demand.

Mar 30 2026: UK Final Q4 GDP; confirmation of 0.1 percent stagnation will heavily suppress GBP recovery momentum.

Apr 14 2026: UK Unemployment Rate update; another rise will cement BoE paralysis and crush GBP support.

Apr 29 2026: Australian Consumer Price Index; sticky inflation above 3.8 percent will guarantee relentless AUD yield dominance.