Forex Briefing (WN23 2026): Central Bank Repricing and Geopolitical Crosscurrents

In the days ahead, markets are laser-focused on whether those tentative US-Iran peace drafts can actually reopen the Strait of Hormuz for good. A permanent fix would clear out the heavy geopoliti

WHAT HAS HAPPENED: Global markets are in choppy waters right now. Geopolitical tension and central bank repricings have everything feeling pretty bumpy.

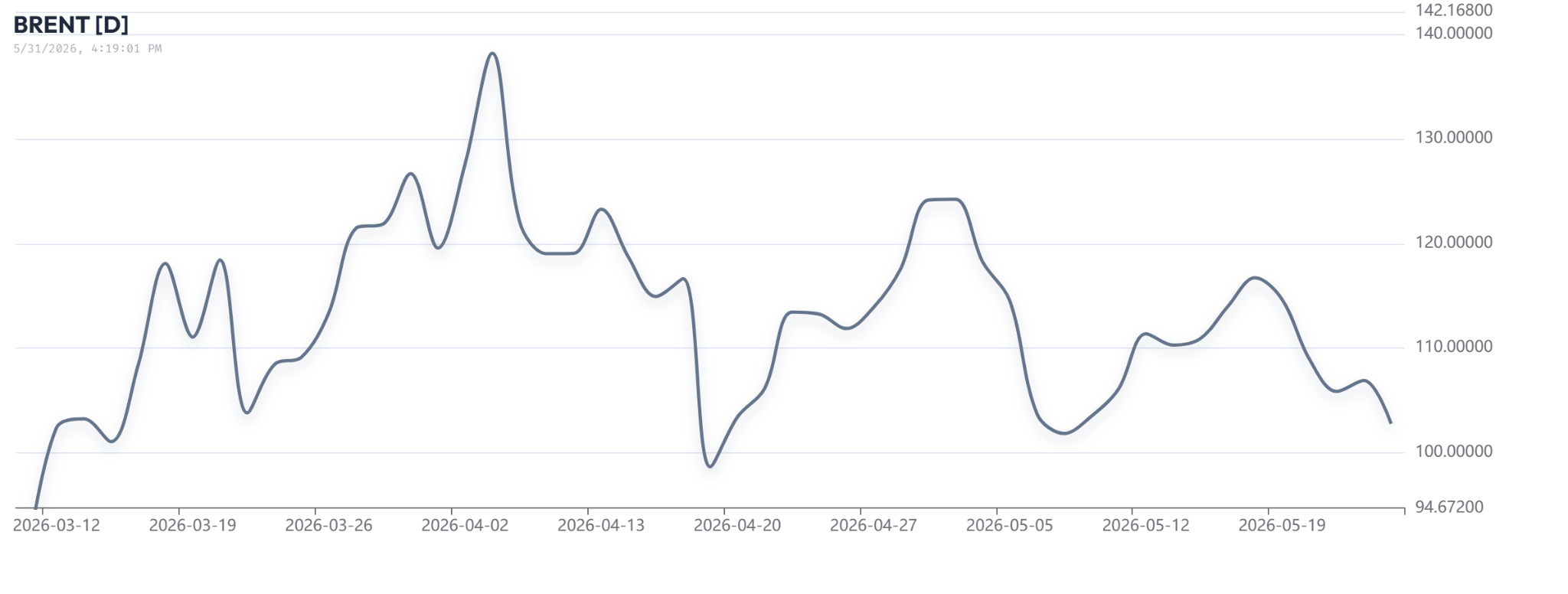

The prolonged Strait of Hormuz closure keeps pushing crude prices higher. It’s fueling those persistent inflationary fears.

Under its new hawkish leadership, the Federal Reserve has anchored rates higher. Sticky CPI data backs that up.

Meanwhile, the Reserve Bank of New Zealand surprised G10 markets with a hawkish split vote. They’re signaling imminent tightening despite soft domestic growth.

WHAT COULD HAPPEN NEXT: In the days ahead, markets are laser-focused on whether those tentative US-Iran peace drafts can actually reopen the Strait of Hormuz for good.

A permanent fix would clear out the heavy geopolitical risk premiums fast. Energy prices would plunge, with Brent crude sliding toward 90 USD per barrel.

That shift would instantly ease the imported stagflation squeezing the Euro Area and UK right now. Their CPIs, hovering above 3%, could cool off quickly.

Meanwhile, currency traders are bracing hard for the upcoming G10 central bank meetings. Stark policy divergence is going to drive the big directional moves.

Everyone will be watching the ECB on June 11 and the Fed on June 17 to see if policymakers budge from their restrictive path.

Will the Fed hold onto its strong yield advantage? Or does new Chair Kevin Warsh signal more hikes to tackle 3.8% inflation and keep the US Dollar well fortified?

On the flip side, BOJ decisions on June 16 and SNB on June 18 could trigger massive unwinds from carry trades. Those low-yielding currencies have been the main funding base.

For the New Zealand Dollar, that heavily crowded speculative net-short of over 25,000 contracts is coiled like a spring.

Any continued hawkish tone into the RBNZ meeting on July 8, or dairy payouts staying resilient near 9.50 USD, could spark a rapid short-covering rally and send the Kiwi sailing higher.