How Will AUD, CAD, JPY, and EUR Move?

Thursday, September 26, 2024 Week 39

Welcome, this report covers AUD/USD, USD/CAD, GBP/JPY, and EUR/USD, providing insights for traders.

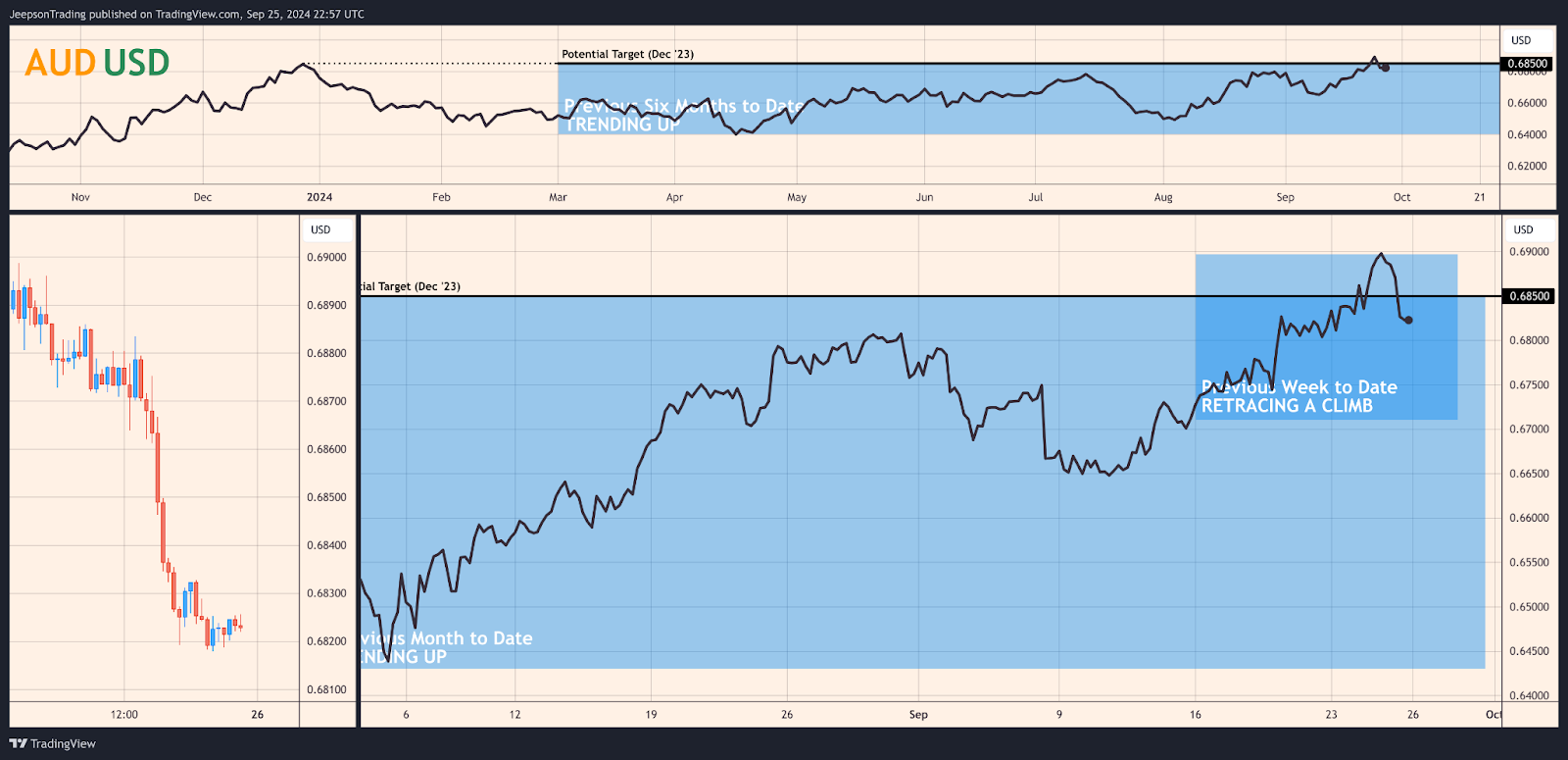

AUD/USD

Institutional investors, commodity traders, and central banks often trade AUD/USD. Iron ore price swings heavily influence liquidity, showing a strong positive correlation. Asset managers are net long AUD, according to the COT report, while leveraged funds are net short, hinting at differing views on the pair's direction.

The RBA's hawkish stance and China's economic slowdown are key themes impacting AUD/USD. The RBA held rates at 4.35% on Tuesday, September 24th, its seventh consecutive hold. Governor Bullock’s comments reinforced this hawkish position, projecting above-target inflation until 2026, despite easing to 2.7% in August. However, weakening demand from China due to its economic slowdown weighs on iron ore prices and, consequently, the AUD. China’s recent stimulus measures have offered only a temporary reprieve. An emerging theme is US recession fears, creating risk-off sentiment. The AUD, being risk-sensitive, is vulnerable.

This week, AUD/USD has climbed but is now retracing those moves. Over the longer term, the pair has formed an uptrend.

An October Fed rate cut could weaken the USD and strengthen AUD/USD. Global risk-on sentiment also favours AUD appreciation. However, China's uncertain economic outlook adds significant risk.

Conversely, a continued Chinese slowdown could trigger an AUD sell-off, overriding a potential Fed rate cut. Increased risk aversion, possibly from escalating geopolitical tensions, could exacerbate the decline, targeting 0.670. Conviction in this bearish scenario is moderate, given the AUD's sensitivity to risk and China's economic health.

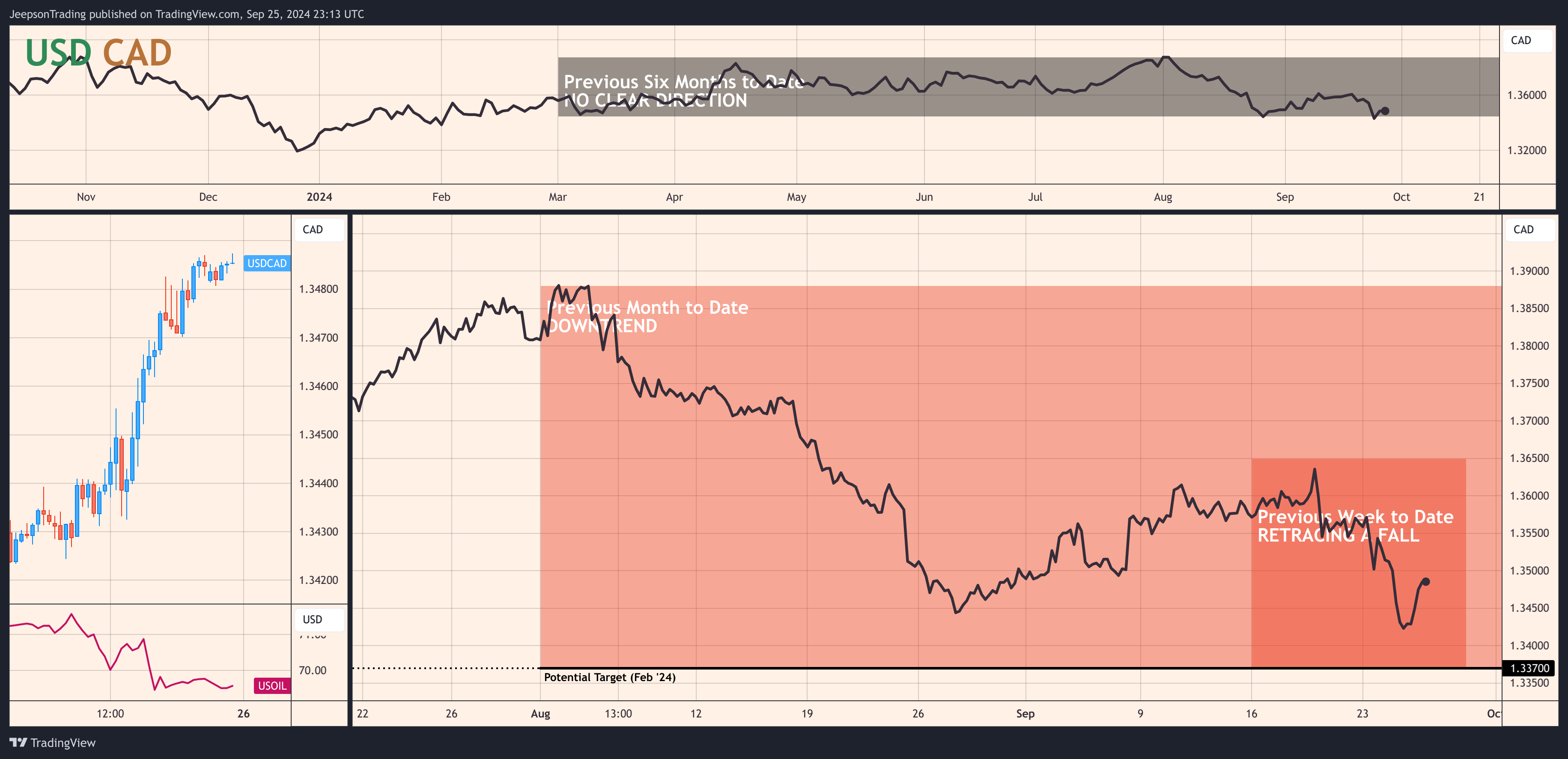

USD/CAD

Institutional investors and corporations trading across the US-Canada border frequently use the USD/CAD pair. Oil prices and interest rate differentials drive liquidity, with the pair typically inversely correlated to oil. Dealers are net long USD/CAD, while leveraged funds are net short, according to the COT report.

Oil price swings and the Fed easing cycle have significantly influenced USD/CAD. Rising Middle East tensions and Hurricane Francine's impact on US oil output boosted oil prices, benefiting the CAD. The Fed's rate cut and projections for further easing weakened the USD. However, Chair Powell's cautious remarks introduced uncertainty. An emerging theme is the anticipation of a BoC rate cut due to slowing inflation and economic data.

USD/CAD has fallen this week, although it is now retracing those moves. The pair has formed a longer term downtrend.

Continued Fed easing and high oil prices could push USD/CAD lower. Another Fed rate cut in October could further weaken the USD. Escalating Middle East tensions support high oil prices.

Conversely, de-escalation in the Middle East and falling oil prices might support USD/CAD, triggering a rebound. Conviction in this bullish scenario is low, considering the dominant themes.

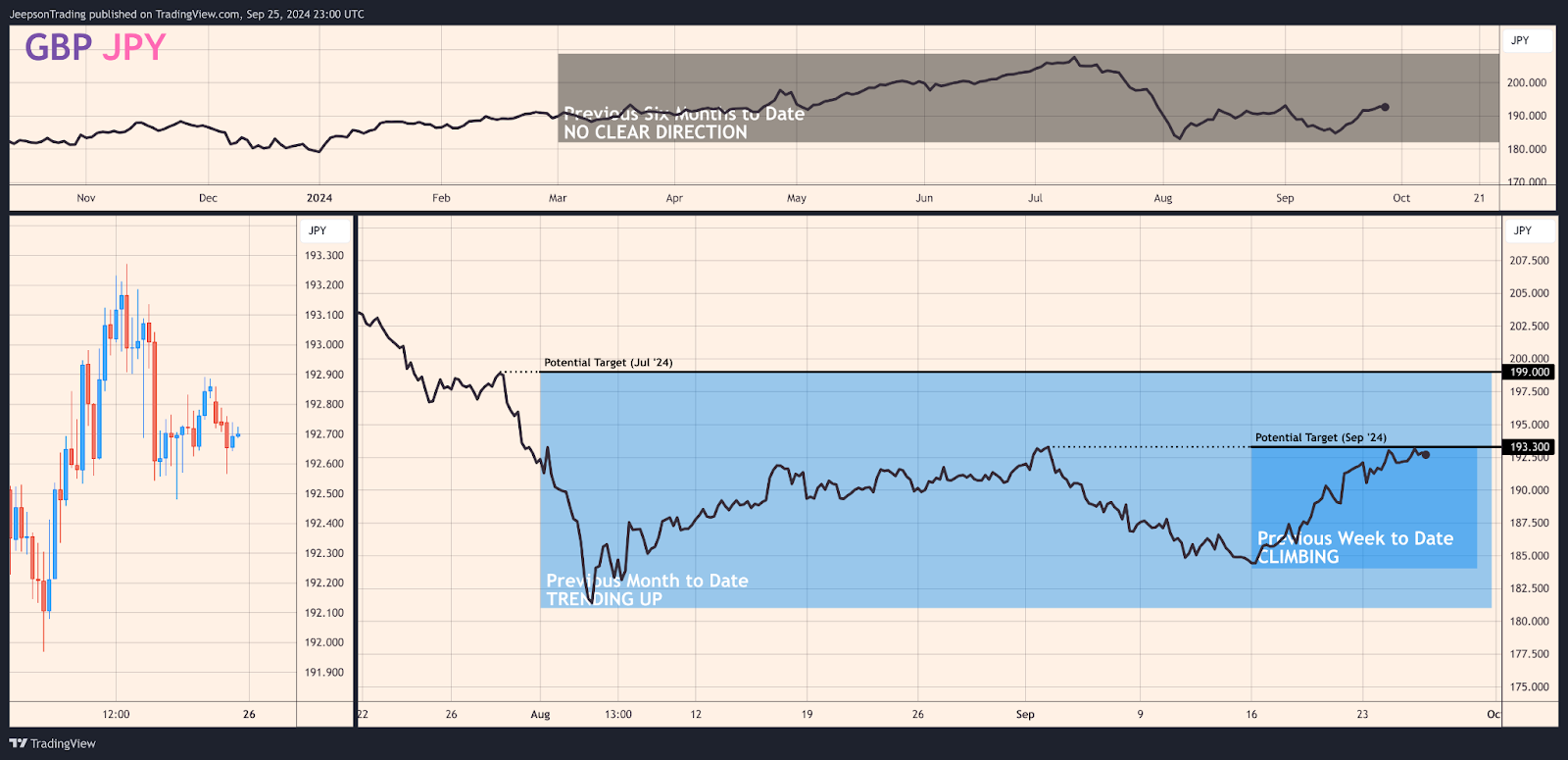

GBP/JPY

Carry traders and institutional investors are drawn to GBP/JPY. Interest rate differentials are key drivers of liquidity. The pair's link to intermarkets is influenced by global risk sentiment and UK/Japan economic releases. Leveraged funds are net long GBP and short JPY, with asset managers also net long GBP, as per the COT report. This suggests a speculative bias towards GBP strength.

Diverging monetary policy between the BoE and BOJ is the dominant GBP/JPY theme. The BoE's relatively hawkish stance compared to the BOJ has boosted the GBP, making it appealing for carry trades. Escalating Middle East tensions could increase risk aversion, benefiting the JPY and weighing on the pair.

GBP/JPY rose this week, hitting 191.965 on Tuesday. This continues the monthly uptrend from 187.668.

A sustained hawkish BoE and dovish BOJ could push GBP/JPY higher, targeting 193.3. Positive UK economic data would reinforce the BoE's stance.

However, weak UK economic data could push the BoE towards rate cuts, weakening the GBP. Increased risk aversion could also strengthen JPY. This bearish scenario has moderate conviction, given the pair's sensitivity to policy changes and risk sentiment.

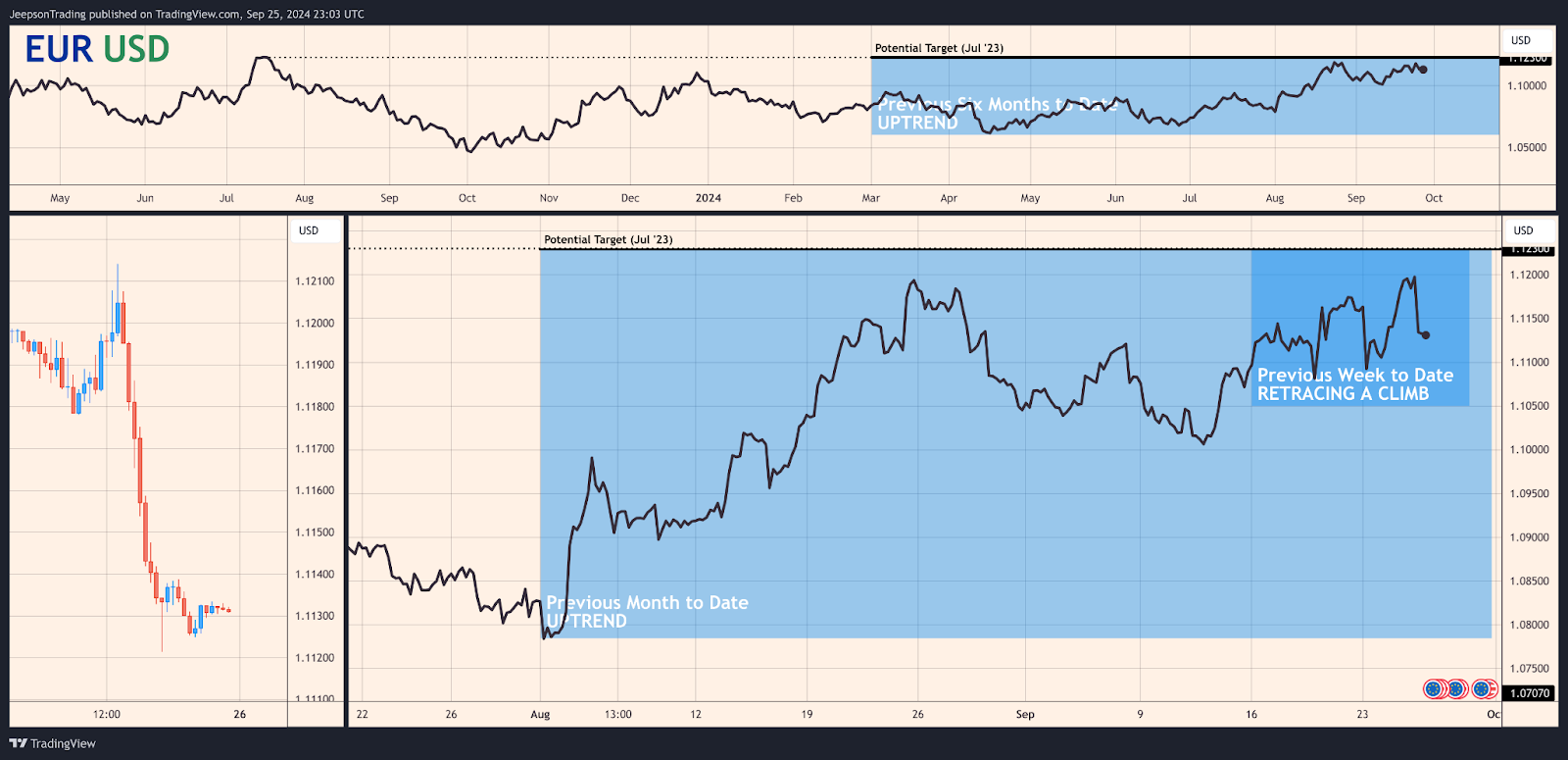

EUR/USD

EUR/USD, actively traded by various participants, has high liquidity driven by factors like interest rate differentials. It typically shows an inverse correlation with the DXY. Asset managers are net long EUR and net short USD, while leveraged funds are moderately long EUR and short USD, according to the COT report.

If the Fed continues to ease and the ECB remains more cautious, EUR/USD could climb, potentially targeting 1.123. Global risk-on sentiment would further support the euro.

However, a less dovish Fed or increased Eurozone economic concerns could dampen the EUR/USD rally. A stronger USD, due to positive US data or safe-haven flows, might trigger a retracement. Conviction in this scenario is low, considering the EUR/USD's current momentum.

Sources

Federal Reserve (Fed)

Bank of England (BoE)

European Central Bank (ECB)

Bank of Japan (BOJ)

Reserve Bank of Australia (RBA)

Reserve Bank of New Zealand (RBNZ)

US Bureau of Labor Statistics

Statistics Canada

Office for National Statistics (UK)

Eurostat

Australian Bureau of Statistics

Statistics New Zealand

Trading Economics

Bloomberg

Reuters

Financial Times

The Wall Street Journal

ForexLive