Inflation, Geopolitics, and the Fed's Tightrope Walk

Forex traders can capitalise on emerging trading opportunities by staying informed about key economic indicators, policy decisions, and geopolitical developments.

The economic landscape has shifted, with the Federal Reserve widely expected to begin cutting interest rates at its September meeting. The recent uptick in the unemployment rate to 4.3% in July, coupled with slowing job gains, has solidified market expectations for a rate cut. This shift was further reinforced by Chair Powell's speech at Jackson Hole, where he acknowledged the cooling labour market and expressed confidence in the progress on disinflation.

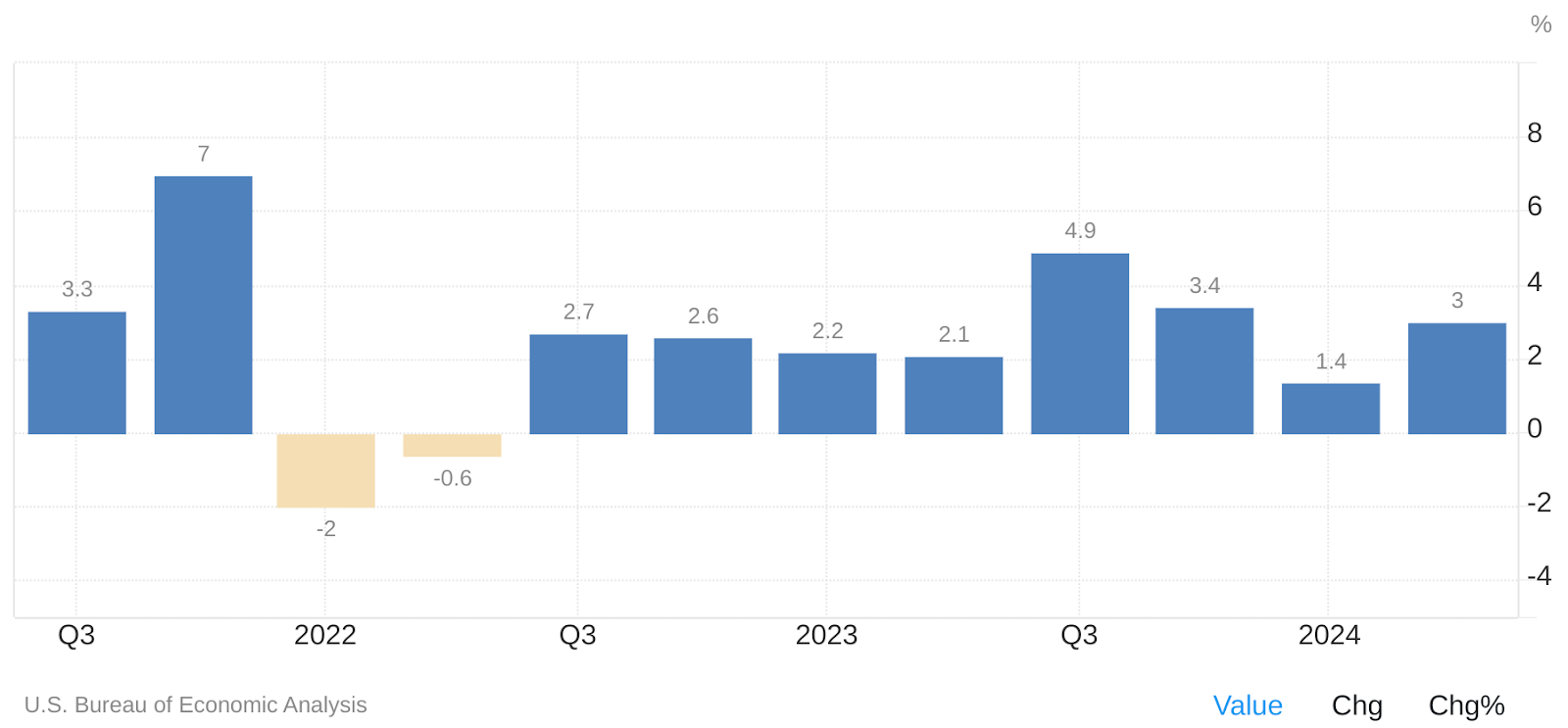

Adding to the intrigue are the latest economic data releases. The US economy expanded at an annualised rate of 3.0% in the second quarter, up from 1.4% in the first quarter, primarily driven by increased consumer spending. However, the manufacturing sector continues to contract, with the ISM Manufacturing PMI falling to 46.8 in July, the lowest since November 2023. This divergence between the services and manufacturing sectors, coupled with the Fed's data-dependent approach, creates a complex and uncertain environment for forex traders.

A World on Edge

The war in Ukraine continues to escalate, with Russia launching its largest air attack against the country on August 26th. This escalation has heightened concerns about energy security and the potential for further sanctions against Russia, which could impact global trade and investment flows.

Adding to the geopolitical risks are ongoing tensions between the US and China. The US recently imposed a 100% tariff on Chinese-made electric vehicles, signalling a potential escalation of the trade war. This move, coupled with China's investigation into European subsidies for dairy products, highlights the potential for further trade disruptions and retaliatory measures.

The situation in the South China Sea also remains tense, with the Philippines accusing a Chinese aircraft of "unsafe manoeuvres" on August 24th. These incidents underscore the ongoing territorial disputes in the region and the potential for escalation, which could disrupt trade routes and impact regional stability.

Looking ahead, the geopolitical landscape is likely to remain volatile, with several key events on the horizon. The upcoming Forum on Africa-China Cooperation in Beijing on September 4-6th could see the announcement of several high-profile bilateral cooperation agreements, potentially strengthening China's economic and political influence in Africa. Russian President Vladimir Putin's visit to Mongolia on September 3rd, a signatory of the International Criminal Court's Rome Statute, will be closely watched, as it could test international norms and potentially undermine the ICC's authority.

Furthermore, the upcoming state elections in eastern Germany on September 1st could see significant gains for populist parties, potentially disrupting the implementation of federal policies and weakening mainstream parties ahead of the country's next general election in September 2025.

The geopolitical landscape will continue to be a key driver of currency valuations in the coming months. Forex traders need to closely monitor these developments and assess their potential impact on risk sentiment, trade flows, and economic growth.

The current geopolitical landscape presents a complex and challenging environment for forex traders. The potential for further escalation in any of these areas could trigger risk aversion, leading to a flight to safety and impacting currency valuations.

US Fiscal Policy: Navigating a Sea of Red Ink

The US fiscal landscape is characterised by a delicate balancing act between addressing pressing needs and managing a growing budget deficit. The Biden administration's significant investments in infrastructure, clean energy, and social programs, coupled with the ongoing economic recovery, have contributed to a widening deficit. The Fiscal Responsibility Act of 2023, enacted earlier this year, aims to address this issue by enacting roughly $1 trillion in savings over the next decade. However, the long-term sustainability of US public finances remains a concern, particularly as interest rates rise and the cost of servicing the debt increases.

US Capitol Building

Market traders are closely monitoring the government's spending and revenue projections, as outlined in the US Treasury's budget for fiscal year 2025. The government's ability to address pressing needs while maintaining fiscal discipline will be crucial for ensuring long-term economic stability and maintaining confidence in the US dollar.

The recent release of the US second-quarter GDP data, showing an annualised growth rate of 3.0%, has provided some reassurance to markets. However, the weaker-than-expected demand at the 10-year US bond auction on August 7th highlighted the fragility of markets in the aftermath of historical volatility. This event, coupled with the ongoing concerns about the US budget deficit, suggests that fiscal policy will remain a key focus for market participants in the coming months.

Looking ahead, the fiscal policy landscape is likely to be shaped by several key factors. The upcoming debate on the 2025 budget, the potential for further tax cuts, and the ongoing debate on government spending will all influence the trajectory of the US fiscal position. Additionally, the outcome of the US presidential election in November could have significant implications for fiscal policy, depending on the winner's priorities and the composition of Congress.

The US fiscal policy landscape will continue to be a key driver of the US dollar's performance in the coming months. Forex traders need to closely monitor these developments and assess their potential impact on economic growth, inflation, and interest rates.

The current fiscal policy landscape presents a mixed picture for forex traders. While the recent GDP data has provided some reassurance, the weaker-than-expected demand at the bond auction and the ongoing concerns about the US budget deficit suggest that fiscal policy will remain a key focus for market participants in the coming months.

US Economic Fundamentals

The US economy continues to send mixed signals, with some indicators pointing to continued strength while others suggest a potential slowdown. The labour market, while still robust, is showing signs of cooling, with the unemployment rate ticking up to 4.3% in July and job gains slowing. Inflation, while down from its peak, remains stubbornly high, eroding consumer purchasing power. The housing market has cooled significantly, with rising mortgage rates and high home prices weighing on affordability.

US GDP Growth Rate -Trading Economics

Market traders are closely monitoring a range of economic indicators, seeking to gauge the health of the economy and its resilience in the face of multiple headwinds. The recently released US second-quarter GDP and PCE data provide a key update on the economy's performance and offer insights into the potential for a recession.

The recent release of the US July retail sales data, showing a 1% month-over-month increase, has provided some support to the view that the US economy is holding up. However, the weaker-than-expected performance of several "Magnificent Seven" megacaps during the recent earnings season has raised concerns about the sustainability of the current bull market. Additionally, the ongoing contraction in the manufacturing sector, as evidenced by the ISM Manufacturing PMI, suggests that the economy is facing headwinds.

Looking ahead, the economic landscape is likely to be shaped by several key factors. The upcoming US jobs report for August, scheduled for release on September 6th 2024, will be crucial for gauging the health of the labour market and assessing the risk of a recession. The release of the CPI data for August on September 11th will provide further insights into the trajectory of inflation. Additionally, the development of the trade war between the US and China, the potential for a currency board in Libya, and the outcome of the US presidential election in November could all have significant implications for the US economy.

The US economic landscape will continue to be a key driver of the US dollar's performance in the coming months. Forex traders need to closely monitor these developments and assess their potential impact on economic growth, inflation, and interest rates.

The current economic landscape presents a mixed picture for forex traders. While the recent retail sales data has provided some support, the weaker-than-expected performance of several megacaps and the ongoing contraction in the manufacturing sector suggest that the economy is facing headwinds.

Walking the Path to Rate Cuts

The Federal Reserve is facing a challenging environment as it seeks to balance its dual mandate of maximising employment and maintaining price stability. Inflation, while down from its peak, remains stubbornly high. However, there are strong expectations for a shift towards a more dovish stance in the near-term, with a rate cut widely anticipated at the September FOMC meeting. This expectation is driven by signs of cooling inflation and a moderating labour market.

Chair Powell's recent speech at Jackson Hole provided valuable insights into the Fed's thinking, emphasising a data-dependent approach to policy decisions. Market participants are closely monitoring economic data and Fed communications, seeking to anticipate the timing and magnitude of future rate cuts and their potential impact on financial markets.

The recent uptick in the unemployment rate to 4.3% in July, coupled with slowing job gains, has solidified market expectations for a rate cut in September. This shift was further reinforced by Chair Powell's speech at Jackson Hole, where he acknowledged the cooling labour market and expressed confidence in the progress on disinflation.

Looking ahead, the monetary policy landscape is likely to be shaped by several key factors. The upcoming US jobs report for August, scheduled for release on September 6th 2024, will be a key data point for the Fed, as it will provide insights into the strength of the labour market and the potential for wage-push inflation. The release of the CPI data for August on September 11th will provide further insights into the trajectory of inflation. Additionally, the development of the trade war between the US and China and the potential for a currency board in Libya could also influence the Fed's policy decisions.

"We will continue to make our decisions meeting by meeting, based on the totality of incoming data and their implications for the outlook for economic activity and inflation." - Chair Jerome Powell, July 31, 2024 FOMC Statement

The Federal Reserve's data-dependent approach to monetary policy will continue to be a key driver of the US dollar's performance in the coming months. Forex traders need to closely monitor economic data releases and Fed communications, seeking to anticipate the timing and magnitude of future rate cuts and their potential impact on financial markets.

The current monetary policy landscape is pointing towards a rate cut in September, but the exact timing and magnitude remain uncertain. The upcoming US jobs report for August and the CPI data for August will be crucial for gauging the Fed's next move.

A Data-Dependent Path Ahead

The US macroeconomic outlook is currently characterised by a high degree of uncertainty, with the path ahead heavily dependent on incoming economic data and the Federal Reserve's response to those data. While the economy has shown resilience, with solid consumer spending and a robust labour market, persistent inflation and the lagged effects of the Fed's aggressive tightening cycle pose significant risks.

In the near-term, the US economy is expected to continue expanding, albeit at a slower pace. The labour market is likely to remain strong, supporting consumer spending. However, inflation is expected to remain elevated. The recently released US second-quarter GDP and PCE data provide a key update on the economy's performance and offer insights into the potential for a recession.

The short-term risks to the economic outlook are tilted to the downside. The lagged impact of the Fed's aggressive tightening cycle could begin to weigh more heavily on economic activity, increasing the risk of a recession. Additionally, persistent inflation could erode consumer confidence and further dampen spending. The release of the US jobs report for August on September 6th 2024 will be crucial for gauging the health of the labour market and assessing the risk of a recession. This report will be particularly important in light of Chair Powell's comments at Jackson Hole, where he emphasised the importance of the labour market in the Fed's policy decisions.

In the mid-term, the outlook hinges on the Federal Reserve's ability to navigate a delicate balancing act. The central bank needs to bring inflation down to its 2% target without causing a sharp slowdown in economic activity. A soft landing, while challenging, is still possible, but it will require careful monitoring of incoming data and a flexible approach to monetary policy. The development of the trade war between the US and China will also be a key factor to watch, as any further escalation could have significant implications for global trade flows, economic growth, and currency valuations.

The US macroeconomic outlook is currently characterised by a high degree of uncertainty, with the path ahead heavily dependent on incoming economic data and the Federal Reserve's response to those data. While the economy has shown resilience, with solid consumer spending and a robust labour market, persistent inflation and the lagged effects of the Fed's aggressive tightening cycle pose significant risks.

Key Economic Indicators to Watch

The following economic indicators are key to tracking the macroeconomic outlook for the US dollar in the coming month:

Economic Growth:

Gross Domestic Product (GDP): The advance estimate for third-quarter GDP will be released on November 13th. This indicator is expected to show a slowdown in economic growth compared to the second quarter, reflecting the lagged impact of the Fed's aggressive tightening cycle. Lagging indicator.

Industrial Production: The next release of Industrial Production data is scheduled for September 17th. This indicator is expected to show continued weakness in the manufacturing sector, reflecting weak demand and ongoing supply chain disruptions. Coincident indicator.

Price Changes (Inflation):

Consumer Price Index (CPI): The next CPI release is scheduled for September 11th. This indicator is expected to show a moderation in inflation compared to June, reflecting the easing of supply chain disruptions and the cooling of the housing market. However, inflation is likely to remain elevated. Lagging indicator.

Producer Price Index (PPI): The next PPI release is scheduled for September 12th. This indicator is expected to show a moderation in producer price inflation, reflecting the easing of supply chain disruptions and the cooling of commodity prices. However, producer price inflation is likely to remain elevated, suggesting that inflationary pressures could persist. Leading indicator.

Core PCE Price Index MoM: The August Core PCE Price Index will be released on September 27th. This indicator is expected to show a moderation in core PCE inflation, reflecting the easing of supply chain disruptions and the cooling of the housing market. Lagging indicator.

Labour:

Non-Farm Payrolls: The next Non-Farm Payrolls report is scheduled for September 6th 2024. This indicator is expected to show a slowdown in job growth compared to June, reflecting the cooling of the labour market. Lagging indicator.

Unemployment Rate: The next Unemployment Rate release is also scheduled for September 6th 2024. This indicator is expected to show a slight increase in the unemployment rate, reflecting the cooling of the labour market. Lagging indicator.

Housing:

Building Permits: The next Building Permits release is scheduled for September 18th. This indicator is expected to show a further decline in building permits, reflecting the cooling of the housing market and the impact of rising mortgage rates. Leading indicator.

Housing Starts: The next Housing Starts release is also scheduled for September 18th. This indicator is expected to show a further decline in housing starts, reflecting the cooling of the housing market and the impact of rising mortgage rates. Leading indicator.

Business Confidence:

ISM Manufacturing PMI: The August ISM Manufacturing PMI will be released on September 3rd. This indicator is expected to show continued contraction in the manufacturing sector, reflecting weak demand and ongoing supply chain disruptions. Leading indicator.

ISM Services PMI: The August ISM Services PMI will be released on September 4th. This indicator is expected to show a moderation in services sector activity, reflecting the cooling of the economy and the impact of rising interest rates. Leading indicator.

Consumer Sentiment:

Michigan Consumer Sentiment: The preliminary reading for September's Michigan Consumer Sentiment will be released on September 13th. This indicator is expected to show a slight decline in consumer confidence, reflecting concerns about the economic outlook and persistent inflation. Leading indicator.

Trade:

Balance of Trade: The July Balance of Trade data will be released on September 4th. This indicator is expected to show a widening of the trade deficit, reflecting the strong US dollar and the slowdown in global growth. Lagging indicator.

Conclusion

The US dollar is currently navigating a complex and uncertain macroeconomic environment. While the economy has shown resilience, with solid consumer spending and a robust labour market, persistent inflation and the lagged effects of the Fed's aggressive tightening cycle pose significant risks. The Federal Reserve's data-dependent approach to monetary policy, the government's fiscal policies, and the evolution of the geopolitical landscape will continue to shape the trajectory of the US dollar in the coming months and years.

Key Takeaways for Forex Traders:

Monitor economic data releases closely: The upcoming US jobs report for August, CPI data for August, PPI data for August, and PCE data for August will be crucial for gauging the Fed's next move and the trajectory of the US dollar.

Pay attention to Fed communications: Chair Powell's speech at Jackson Hole emphasised a data-dependent approach to policy decisions. Forex traders need to closely monitor Fed communications for any hints about the timing and magnitude of future rate cuts.

Assess geopolitical risks: The ongoing war in Ukraine, the US-China trade war, and the potential for a currency board in Libya could all impact the US dollar's performance.

Consider fiscal policy developments: The US budget deficit and the government's debt management strategies could also influence the US dollar's trajectory.

The US dollar's path ahead is likely to be volatile, with periods of both strength and weakness. Forex traders who stay informed about key economic indicators, policy decisions, and geopolitical developments will be best positioned to navigate this uncertainty and capitalise on emerging trading opportunities.

Sources

U.S. Bureau of Economic Analysis (BEA)

Federal Reserve

U.S. Census Bureau

Institute for Supply Management (ISM)

National Association of Home Builders (NAHB)

Standard & Poor's

Trading Economics

Newsquawk

Stratfor Worldview