Pound at the Precipice: Policy Shifts Meet Political Change

Saturday, November 09, 2024 (Week 45)

Welcome to our deep dive into the fundamental forces shaping the British pound's trajectory. As Forex traders prepare for the coming week, attention centres squarely on Thursday's crucial GDP release and its implications for sterling's strength following the Bank of England's latest policy shift. This analysis distils the complex interplay of monetary policy, economic indicators, and market dynamics to provide actionable insights for currency traders navigating these pivotal market conditions.

Monetary Policy Takes Center Stage

The Bank of England's carefully orchestrated 25-basis-point rate reduction to 4.75% on November 7th has fundamentally reshaped sterling's near-term outlook. In a decisive move that exceeded market expectations, eight out of nine Monetary Policy Committee members backed the cut, signalling growing confidence in the bank's ability to navigate declining inflation while supporting economic growth. This shift in stance has triggered a comprehensive repricing of interest rate expectations, with markets now anticipating two additional quarter-point reductions through 2025.

Political Crosscurrents Emerge

The surprise victory of Donald Trump in the U.S. presidential election has introduced a new layer of complexity to sterling's fundamental outlook. Market participants have begun factoring in potential implications for UK-US trade relationships, particularly given the previous Trump administration's stance on international trade agreements. This emerging narrative has contributed to increased volatility in sterling crosses, especially during the latter half of the week.

Global Forces Shape Sterling's Path: Geopolitical Dynamics

Sterling's fundamental position reflects the UK's role as a major financial hub particularly sensitive to shifts in global trade dynamics and international capital flows. The past week has seen this sensitivity amplified by Trump's unexpected victory, which dominated market sentiment and prompted a reassessment of the pound's risk premium. While Middle East tensions persist, their impact on sterling has been notably overshadowed by the implications of domestic policy shifts and U.S. political developments.

Monetary Strategy in Focus: Central Bank Policy Evolution

The Bank of England maintains its primary mandate of price stability through a 2% inflation target, while carefully weighing broader economic considerations. Under Governor Andrew Bailey's leadership, the bank has demonstrated increased willingness to respond proactively to changing economic conditions.

Recent Policy Developments

November 7th's rate decision marked a significant milestone in the BoE's policy evolution. The 25-basis-point reduction to 4.75%, supported by an overwhelming majority of the MPC, reflected the bank's growing confidence in controlling inflation pressures. The bank's updated projections now anticipate inflation reaching 2.5% by year-end, incorporating the stimulative effects of recent government budget measures that could boost GDP by approximately 0.75% at peak impact.

Economic Pulse Check: Key Performance Indicators

Growth Dynamics

GDP (August 2024):

Monthly: +0.2% (In line with expectations)

Next release: November 14th

Growth trend: Shows gradual expansion despite global headwinds

Price Stability

Inflation (September 2024):

Headline: 1.7% YoY (Below 1.9% forecast)

Core: 3.2% YoY (Below 3.4% forecast)

Key driver: Transport costs (-2.2%) significantly contributed to the decline

Next release: November 20th

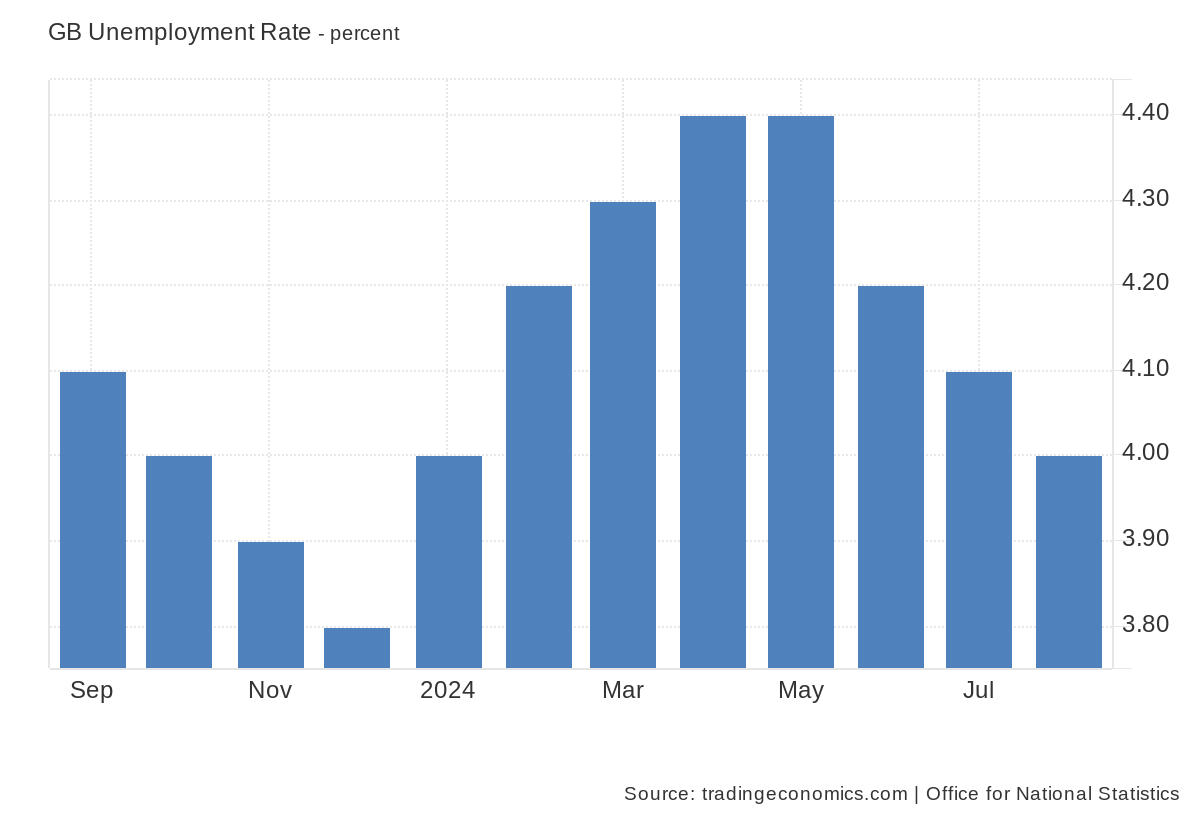

Labor Market Health

Employment (August 2024):

Unemployment rate: 4.0% (Better than 4.1% expected)

Employment change: Record +373K increase

Significance: Demonstrates remarkable labor market resilience

Next release: November 12th

Consumer Activity

Retail Sales (September 2024):

Monthly: +0.3% (Beating -0.3% forecast)

Annual: 3.9% YoY growth

Notable strength in non-food store sales (+2.5%)

Next release: November 22nd

Market Interconnections: Asset Class Relationships

The FTSE 100's movement has become increasingly correlated with sterling's performance, particularly following the BoE's rate decision and U.S. election results. UK government bond yields have responded dramatically to policy shifts, with the 10-year gilt yield surging above 4.51% on October 30th - its highest level in a year. This movement reflects both domestic policy evolution and broader global risk sentiment shifts, creating a complex web of market relationships that forex traders must navigate carefully.

Sterling's Fundamental Outlook: Currency Analysis

Current Position

The pound sterling currently sits at a crucial juncture, having demonstrated significant volatility throughout the week. Following an initial decline to $1.285 after Trump's victory announcement, sterling found support around the BoE rate decision, though remained vulnerable to shifting market sentiment.

Recent Trading Dynamics

The previous week saw sterling buffeted by multiple forces:

BoE's rate cut initially pressured the currency before markets digested the broader policy implications

Trump's election victory triggered risk-off flows affecting sterling crosses

Better-than-expected economic data provided periodic support

Global risk sentiment shifts influenced trading patterns

Upside Catalysts

Looking ahead through November, several potential catalysts could support sterling:

Stronger-than-forecast GDP data (November 14th release)

Continued labour market resilience

Signs of stabilising inflation expectations

Downside Risks

Key risks to monitor include:

Impact of evolving U.S. trade policy under Trump administration

Potential deterioration in economic indicators

Further monetary policy easing signals from the BoE

Key Insights: Conclusion

Sterling faces a complex landscape where domestic policy shifts intersect with evolving global dynamics. The currency's path forward will likely be shaped by the interplay between monetary policy effectiveness, economic performance, and international trade considerations.

Key Takeaways:

BoE's policy pivot represents a carefully calibrated response to evolving economic conditions

Political developments, particularly in the U.S., have introduced new uncertainties for sterling's outlook

Economic indicators suggest underlying resilience despite policy transitions

Sources

Bank of England, Office for National Statistics, S&P Global, GfK, Halifax, Nationwide, Bloomberg