Selling the GBP/USD 🇬🇧 🇺🇸

Look to sell at higher levels...

-SUMMARY-

The long term downtrend of the GBP/USD is currently being retraced and has formed a short term uptrend. Price is a long way from resistance at $1.36 and that value is not currently expected to be achievable.

This uptrend is supported against moves lower due to the sentiment towards Fed Policy which is weakening the USD as markets price in a pivot due to the recently softer than expected CPI report.

This optimistic sentiment is likely to be tested on Wednesday when the FOMC minutes are released. Any hint of a dovish tilt is likely to further weaken the USD and spur the GBP/USD higher. As the meeting occurred before the soft CPI data, the risk that it will be interpreted as hawkish is likely to be negated.

Analysis indicates that Sterling has a weak outlook ahead and so Risk Level One orders to sell the GBP/USD while below 1.226 have been placed.

FUNDAMENTALS

-UNITED KINGDOM-

On the 3rd of November, the Bank Rate was hiked by 0.75 to 3.00 percent. This matched the market expectations and was higher than the 0.50 percent hike at the September meeting.

This is the eighth consecutive rate hike and the largest hike since 1989. The MPC remarked that further hikes may be required although at a lower peak than currently priced into markets.

The next meeting is on Thursday the 15th of December and the long term outlook is for higher rates although it is likely that rates will be less hawkish than expected.

The outlook for:

UK GDP is pessimistic deterioration (pr. )

UK CPI is indifferent improvement (pr. )

UK Unemployment is pessimistic deterioration (pr. pessimistic indifference)

-UNITED STATES-

On the 2nd of November, the Federal Funds Rate was hiked by 75bps to between 3.75 and 4.00 percent. This matched the market expectations and also matched the previous hike at the September meeting.

This is the sixth consecutive rate hike and borrowing costs are now at the highest since 2008. During the press conference, Chair Powell commented that the rates will be higher than previously expected.

The next meeting is on Wednesday the 14th of December and the long term outlook is for higher rates although it is likely that rates will be more hawkish than expected.

The CME FedWatch tool indicates 71 percent odds of a 0.50 hike and 29 percent of a 0.75 hike (pr. 80/20).

The outlook for:

US GDP is pessimistic deterioration (pr. )

US CPI is optimistic indifferent improvement (pr. )

US Unemployment is pessimistic deterioration (pr. )

SENTIMENT

-BOE POLICY SUPPORTS THE GBP/USD AGAINST MOVES LOWER-

On Thursday the 3rd of November the Bank of England hiked rates by 0.75 percent and commented that higher rates are necessary to control inflation but probably not as high as has been priced in. This was interpreted as a dovish move but in reality it is simply less-hawkish.

The outlook is still dire as the bank projects a two-year recession but the not-as-bad as expected moves on rates will improve sentiment towards borrowing costs. This in turn will move the FTSE 100 away from overly-bearish moves as earnings pick up due to less-than-terrible consumer spending and foreign investment. There may also be some pick up on government bonds resulting in a lower peak yield than had been expected.

-FED POLICY TO KEEP GBP/USD IN A RANGE-

On Wednesday the 2nd of November the Federal Reserve hiked rates by 0.75 percent and commented that it would be better to raise too-high rather than too-low. This has been interpreted as a hawkish move.

A couple of weeks ago, US CPI came in a little lower (better) than expected and speculators are re-positioning for a Fed pivot. However - this would be against the grain of what was mentioned at the previous Fed meeting where rates were hiked 0.75 percent and Chairman Powell remarked that it would be better to raise too-high than too-low.

TECHNICALS

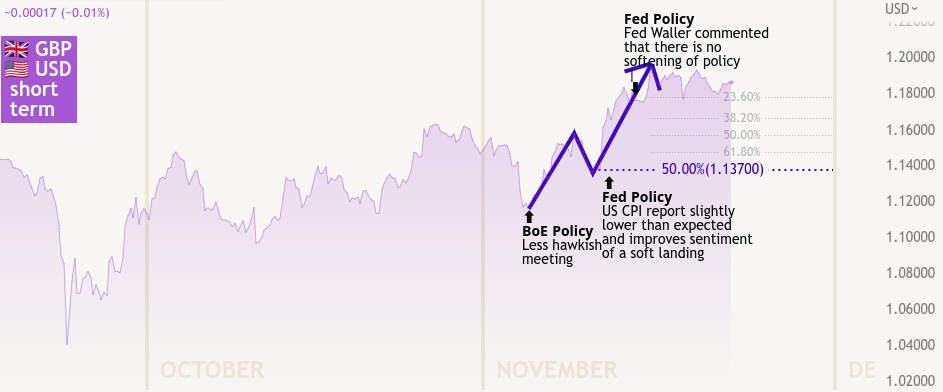

-SHORT TERM-

The short term view (month on month) shows that the GBP/USD has been uptrending since the start of the month (November) when the BoE hiked rates but commented that markets had priced in higher rates than may be required.

This uptrend was further supported when the US CPI report came in slightly lower than expected and weakened the US dollar.

The pair has since found a stable level above 1.18 which held as the latest budget announcement was made indicating investor confidence.

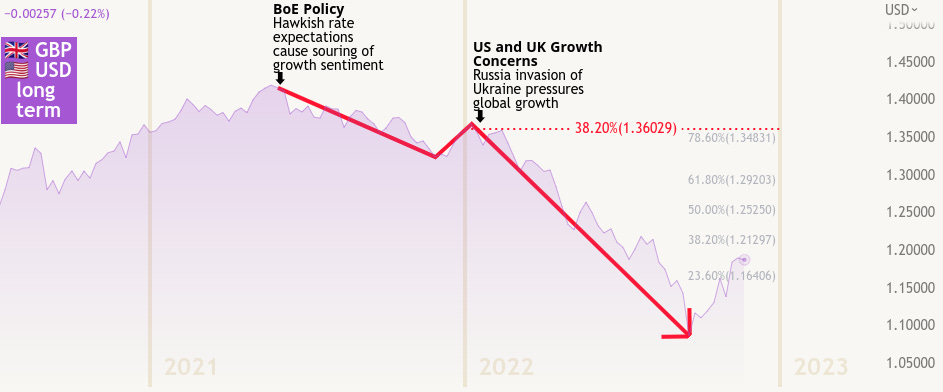

-LONG TERM-

The long term view (year on year) shows that the GBP/USD has been downtrending since last year, which began in mid-2021 when the inflation rate began to pick up in the UK and expectations were elevated that the Bank of England would look to raise rates sooner than had been previously expected.

This fall in sterling was pressured further as safe haven flows into the US dollar picked up this year in February 2022 as Russia invaded Ukraine. The subsequent sanctions that followed and lack of supply to the energy markets pushed global inflation higher than had been anticipated and central banks have had to tighten at a record pace. This has lowered global growth which keeps the USD higher and GBP lower.

Recently, the GBP/USD is retracing the fall although the price is far below the confirmed previous retracement at $1.36.

-END DISCLAIMER-

- Copy the trade plan with an investment at www.etoro.com/people/jeepsontrading

- Detailed analysis over at at www.jeepsontrading.substack.com

- The content provided is intended for informational purposes only. Investments on the forex markets and trading decisions are made at your own risk