Trading Opportunities: AUDUSD, USDJPY, and USDCAD in Focus

Tuesday, August 6, Week 32

This report focuses on the AUDUSD, USDJPY, and USDCAD currency pairs due to their significant economic and geopolitical implications, as well as their potential for volatility in the current market environment. These pairs represent major economies with distinct monetary policy stances, economic outlooks, and sensitivities to global events, making them attractive for forex traders seeking opportunities.

Market sentiment towards these currency pairs has been particularly dynamic in the past week. The Australian dollar weakened after the RBA held rates steady but maintained a hawkish bias, while the US dollar experienced a broad selloff following a disappointing jobs report, boosting the Japanese yen and Canadian dollar. The Japanese yen's strength was further fueled by the Bank of Japan's hawkish policy adjustments on July 31st. This week, the Aussie has shown some signs of recovery, while the USDJPY and USDCAD remain sensitive to shifts in risk sentiment and monetary policy expectations. Looking ahead, the upcoming days will be crucial for these currency pairs, with key economic data releases and central bank announcements likely to drive further price movements.

AUDUSD: Aussie Seeks Footing as RBA Holds Firm

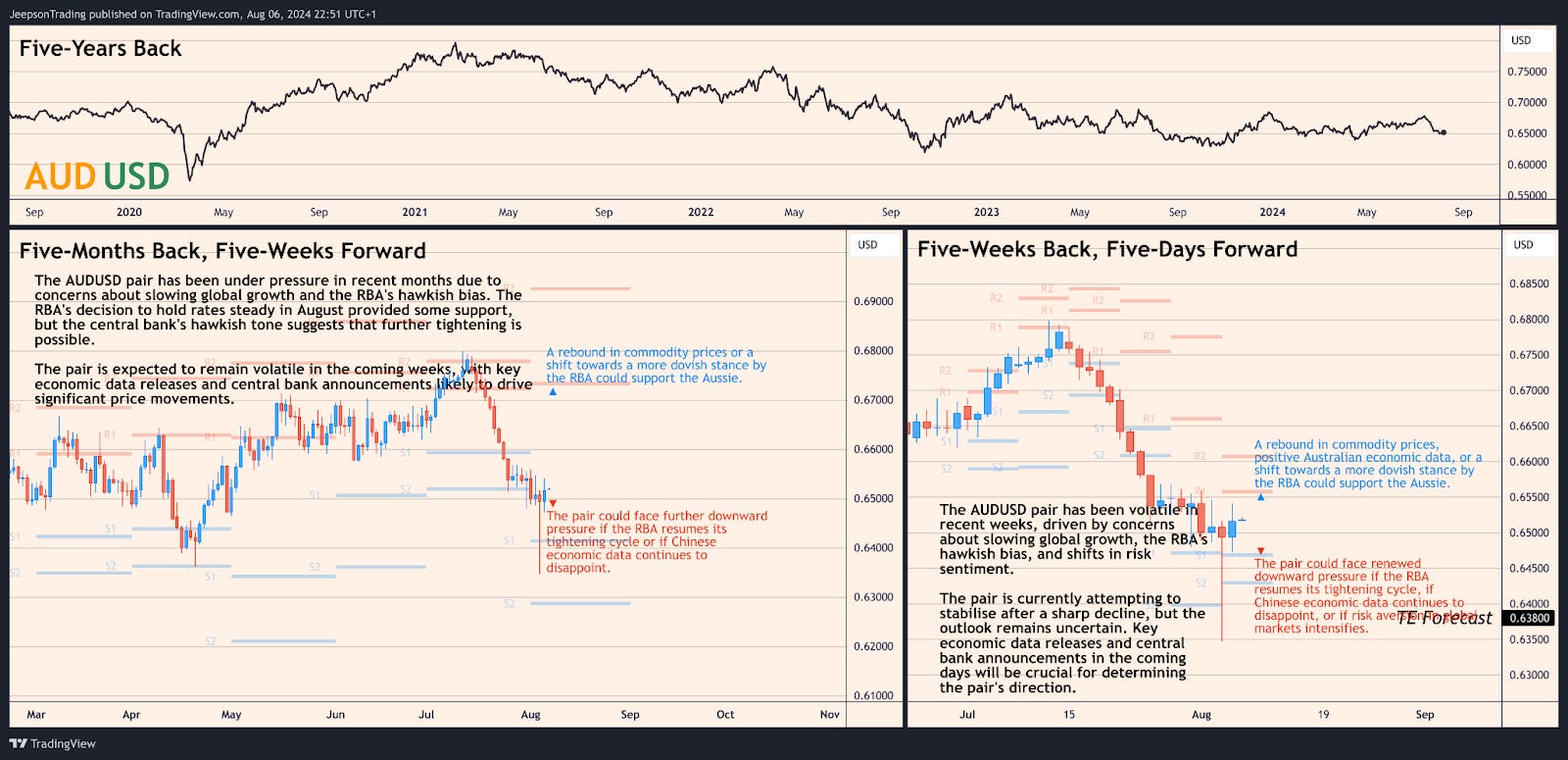

The AUDUSD pair experienced a volatile month, initially reaching a high of 0.6770 on May 15th before declining to a low of 0.6495 on August 2nd. This downward trend was driven by concerns about slowing global growth, particularly in China, Australia's largest trading partner, and the RBA's hawkish stance on monetary policy. The release of weaker-than-expected Q1 GDP growth data on July 31st, showing an expansion of just 0.1% qoq, further weighed on the Aussie. The RBA's decision on August 6th to hold the cash rate steady at 4.35% for the sixth consecutive meeting was widely anticipated, but the central bank's hawkish tone, signalling potential for further rate hikes, initially sent the AUDUSD lower.

However, the Aussie has shown some signs of recovery this week, with the pair trading back above 0.6500. This rebound could be attributed to a slight easing of risk aversion in global markets and a potential short-covering rally. Looking ahead, the outlook for the AUDUSD pair remains uncertain. The pair could face renewed downward pressure if the RBA resumes its tightening cycle or if Chinese economic data continues to disappoint. However, a potential rebound in commodity prices or a shift towards a more dovish stance by the RBA could support the Aussie.

Summary: The AUDUSD pair has been volatile in recent weeks, driven by concerns about slowing global growth, the RBA's hawkish bias, and shifts in risk sentiment. The pair is currently attempting to stabilise after a sharp decline, but the outlook remains uncertain. Key economic data releases and central bank announcements in the coming days will be crucial for determining the pair's direction.

Upside: A rebound in commodity prices, positive Australian economic data, or a shift towards a more dovish stance by the RBA could support the Aussie.

Downside: The pair could face renewed downward pressure if the RBA resumes its tightening cycle, if Chinese economic data continues to disappoint, or if risk aversion in global markets intensifies.

Action Points:

Monitor the RBA's communication for any shifts in its assessment of inflation risks and the outlook for economic growth.

Track key economic indicators, particularly inflation, GDP growth, and labour market data from both Australia and China.

Assess the impact of global risk sentiment on the Aussie dollar.

Key Economic Events:

Wednesday, August 7, Week 32: Ai Group Industry Index (July)

Thursday, August 8, Week 32: NAB Business Confidence (July)

Thursday, August 15, Week 33: Employment Change (July)

Wednesday, August 28, Week 35: Monthly CPI Indicator (July)

USDJPY: Yen Strengthens as US Dollar Falters, BoJ Turns Hawkish

The USDJPY pair experienced a sharp decline in the past month, falling from a high of 161.6255 on July 3rd to a low of 144.766 on August 6th. This move was primarily driven by a weaker-than-expected US jobs report released on August 2nd, which fueled expectations for a more dovish Federal Reserve and a broad selloff in the US dollar. The Bank of Japan's decision on July 31st to raise its key interest rate to 0.25% and announce plans to reduce its bond purchases was perceived by the market as a hawkish shift, further boosting the yen. The BoJ's quarterly outlook, released on the same day, projected core inflation for FY 2024 to fall to around 2.5%, less than April's forecasts of 2.8%, but this downward revision did not deter the market's hawkish interpretation of the BoJ's policy adjustments.

The USDJPY pair has continued to fluctuate this week, with the yen remaining sensitive to shifts in global risk sentiment and monetary policy expectations. The BoJ's Summary of Opinions, due on Thursday, August 8th, will be closely watched for further clues about the central bank's policy trajectory. Looking ahead, the outlook for the USDJPY pair remains uncertain. The pair could face further downward pressure if the US economy slows more than expected, prompting the Fed to cut interest rates. However, a rebound in US economic data or further hawkish signals from the BoJ could support the USDJPY.

Summary: The USDJPY pair has weakened significantly in recent weeks, driven by US dollar weakness and the BoJ's hawkish policy shift. The pair is expected to remain volatile in the coming days, with key economic data releases and central bank announcements likely to drive further price movements.

Upside: A rebound in US economic data, further hawkish signals from the BoJ, or a return of risk appetite in global markets could support the USDJPY.

Downside: The pair could face further downward pressure if the US economy slows more than expected, prompting the Fed to cut interest rates, or if safe-haven demand for the yen intensifies.

Action Points:

Monitor the BoJ's communication for any shifts in its policy stance.

Track key economic indicators from both the US and Japan, particularly inflation and GDP growth data.

Assess the impact of global risk sentiment on the yen's valuation.

Key Economic Events:

Thursday, August 8, Week 32: BoJ Summary of Opinions

Thursday, August 15, Week 33: US GDP Growth Rate QoQ Prel Q2

Friday, August 23, Week 34: Japan Inflation Rate YoY (July)

USDCAD: Loonie Weathers US Dollar Storm, But BoC Rate Cuts Weigh

The USDCAD pair broke out to the upside in late July, reaching an eight-month high of 1.3881 on August 1st. This move was driven by a slowdown in the Canadian economy, highlighted by the release of the June jobs report on July 5th, which showed a decline in employment and an increase in the unemployment rate to 6.4%. The Bank of Canada's (BoC) decision to cut interest rates by 25 bps in both June and July, bringing the policy rate to 4.5%, also weighed on the loonie. The BoC's dovish shift, coupled with concerns about the impact of slowing US growth on the Canadian economy, contributed to the CAD's weakness.

However, the USDCAD pair has since retreated from its August 1st high, falling to a low of 1.3784 on August 6th. This pullback has been driven by a broad weakening of the US dollar, fueled by concerns about a potential US recession following a disappointing jobs report on August 2nd. Looking ahead, the outlook for the USDCAD pair remains uncertain. The pair could face renewed upward pressure if the US economy slows more than expected, prompting the Fed to cut interest rates more aggressively. However, a rebound in oil prices or a shift towards a more hawkish stance by the BoC could support the Canadian dollar.

Summary: The USDCAD pair has been volatile in recent weeks, driven by the BoC's rate cuts, slowing Canadian economic growth, and uncertainty about the US economic outlook. The pair's recent breakout to the upside has stalled, and the Canadian dollar is currently being supported by US dollar weakness. The pair is expected to remain volatile in the coming days, with key economic data releases and central bank announcements likely to drive further price movements.

Upside: The pair could face renewed upward pressure if the US economy slows more than expected, prompting the Fed to cut interest rates more aggressively, or if oil prices decline.

Downside: A rebound in oil prices, positive Canadian economic data, or a shift towards a more hawkish stance by the BoC could support the Canadian dollar.

Action Points:

Monitor the BoC's communication for any shifts in its policy stance.

Track key economic indicators from both the US and Canada, particularly inflation, GDP growth, and labour market data.

Assess the impact of oil price movements on the Canadian dollar.

Key Economic Events:

Wednesday, August 7, Week 32: US EIA Crude Oil Stocks Change

Thursday, August 8, Week 32: Canadian Ivey PMI (July)

Friday, August 9, Week 32: Canadian Labour Force Survey (July)

Sources:

Australian Bureau of Statistics

Bank of Canada

Bank of Japan

Trading Economics

Newsquawk

Westpac Banking Corporation

Melbourne Institute

National Australia Bank

S&P Global

Ivey Business School