🇺🇸 United States Dollar Forex Handbook December

Soft landing appears to be more likely...

DERBYSHIRE GB / DEC 04 - December report created.

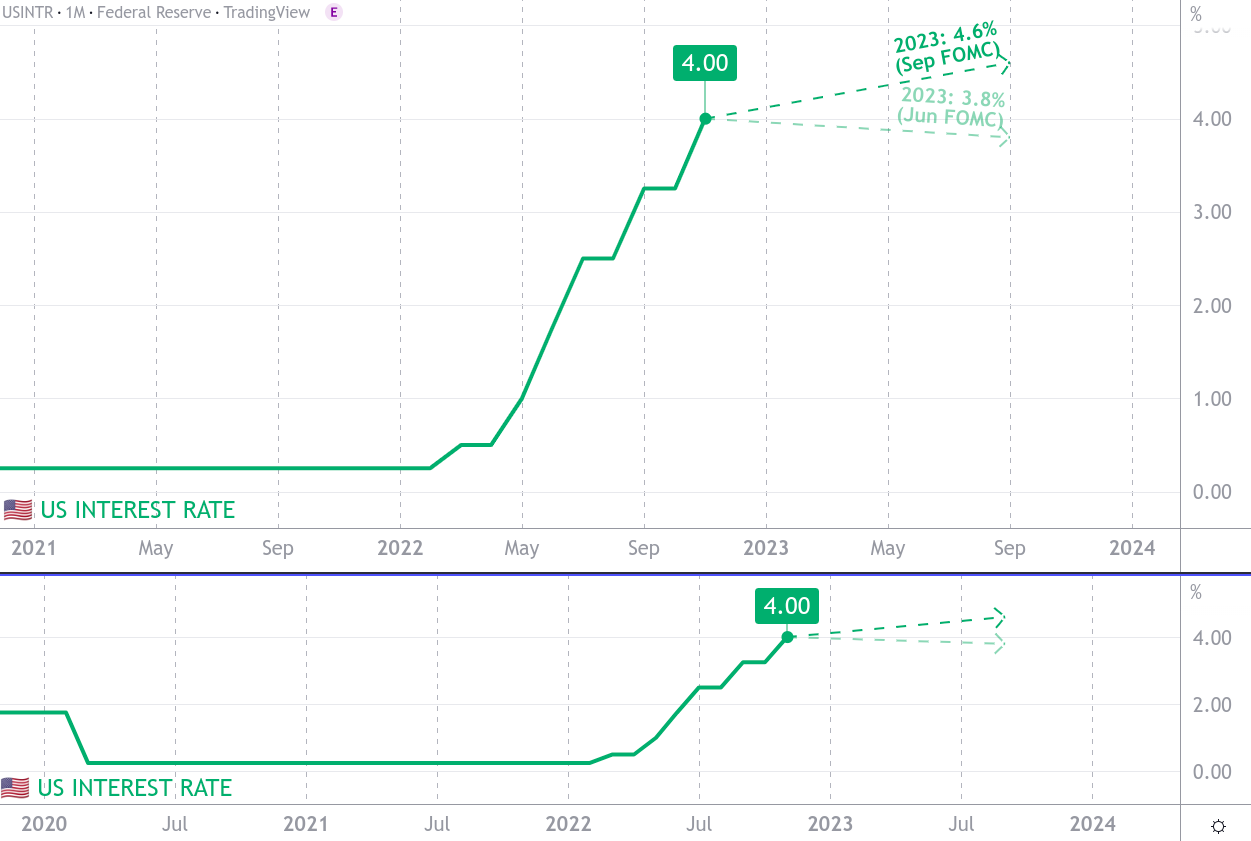

-FEDERAL FUNDS RATE-

source: The Federal Reserve

On the 2nd of November, the Federal Funds Rate was hiked by 75bps to between 3.75 and 4.00 percent. This matched the market expectations and also matched the previous hike at the September meeting.

This is the sixth consecutive rate hike and borrowing costs are now at the highest since 2008. During the press conference, Chair Powell commented that the rates will be higher than previously expected.

The next meeting is on Wednesday the 14th of December and the long term outlook is for higher rates although it is likely that rates will be more hawkish than expected.

The Federal Reserve is the central banking system in the United States and policy decisions are made by the Board and the Federal Open Market Committee (FOMC). The Board has seven members and they decide on changes in discount rates. The FOMC has twelve members who decide on the levels of central bank money and the federal funds rate. The FOMC members include all members of the board, the president of the New York Fed and four presidents from the remaining eleven Reserve Banks on a rotating basis.

_

-FOMC STATEMENT HIGHLIGHTS (NOV)-

Recent indicators point to modest growth in spending and production.

Job gains have been robust in recent months, and the unemployment rate has remained low.

Inflation remains elevated, reflecting supply and demand imbalances related to the pandemic, higher food and energy prices, and broader price pressures.

Russia's war against Ukraine is causing tremendous human and economic hardship. The war and related events are creating additional upward pressure on inflation and are weighing on global economic activity. The Committee is highly attentive to inflation risks.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run.

The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.

In determining the pace of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.

In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in the Plans for Reducing the Size of the Federal Reserve's Balance Sheet that were issued in May.

The Committee is strongly committed to returning inflation to its 2 percent objective.

_

-FOMC PROJECTION HIGHLIGHTS (SEP)-

Changes in Real GDP - FOMC Projection (Sep)

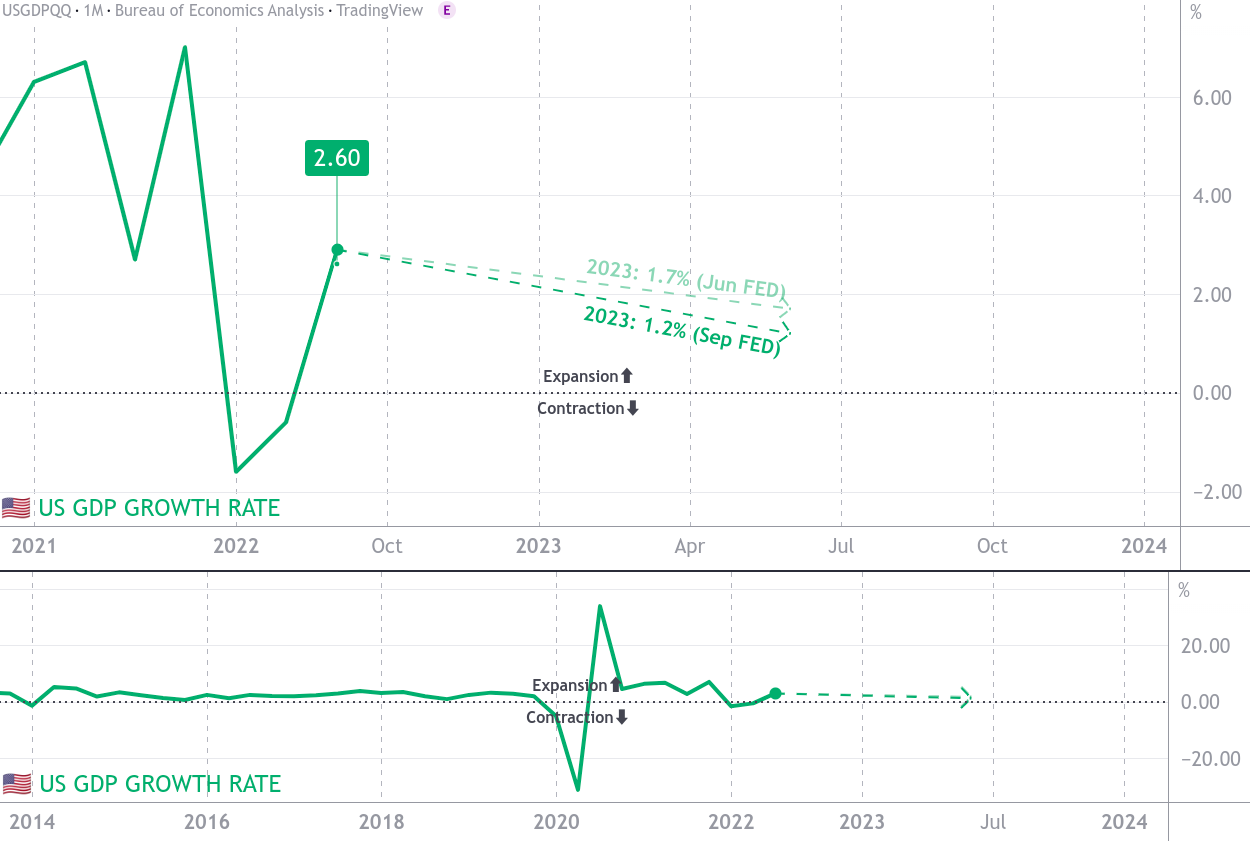

2022 at 0.2% (1.7 Jun)

2023 at 1.2% (1.7 Jun)

2024 at 1.7% (1.9 Jun)

Unemployment Rate - FOMC Projection (Sep)

2022 at 3.8% (3.7 Jun)

2023 at 4.4% (3.9 Jun)

2024 at 4.4% (4.1 Jun)

PCE Inflation - FOMC Projection (Sep)

2022 at 5.4% (5.4 Jun)

2023 at 2.8% (2.6 Jun)

2024 at 2.3% (2.2 Jun)

Federal Funds Rate - FOMC Projection (Sep)

2022 at 4.4% (3.4 Jun)

2023 at 4.6% (3.8 Jun)

2024 at 3.9% (3.4 Jun)

_

-GROSS DOMESTIC PRODUCT GROWTH RATE-

source: Bureau of Economic Analysis

On the 30th of November, the second estimate of the GDP Growth Rate for the three months to September (Q3) was reported at an expansion of 2.9 percent since Q2. This is better than the market consensus of a 2.7 percent expansion and far better than the advance estimate which showed a 2.6 percent expansion over Q2.

Imports contracted 7.3 percent and exports expanded 15.3 percent.

Residential investment (housing market) contracted 26.8 percent.

Consumer spending expanded 1.7 percent driven by health care.

The final Q3 report is out on Thursday the 22nd of December and the long term outlook is for pessimistic deterioration.

Measures the quarter on quarter change of the inflation-adjusted value of goods and services that are produced and then that number is annualised (multiply by four).

_

-CONSUMER PRICE INDEX-

source: Bureau of Labor Statistics

On the 10th of November, the Consumer Price Index (CPI) for the twelve months to October was reported at 7.7 percent inflation. This is far better than the market consensus of 8.0 percent inflation and also far better than the previous month’s report of 8.2 percent.