United States Macroeconomics

Mixed Fundamentals While the Dollar Maintains Resilience Amid Trade Tensions and Fiscal Uncertainty

The US economy displays moderate fundamental strength despite policy volatility, while Dollar sentiment remains cautiously positive due to safe-haven status despite trade-related headwinds.

Trump's Economic Restructuring Creates Volatility Amid Global Trade Tensions

If you've been following the US economy lately, you've likely noticed we're in a period of significant transition. The Trump administration has implemented major changes since January 2025, including broad tariffs on trading partners and aggressive federal workforce cuts through the Department of Government Efficiency (DOGE). Despite these disruptions, the US remains the world's largest economy with a diverse industrial base spanning technology, finance, healthcare, and energy sectors.

Current Situation and Near-Term Outlook

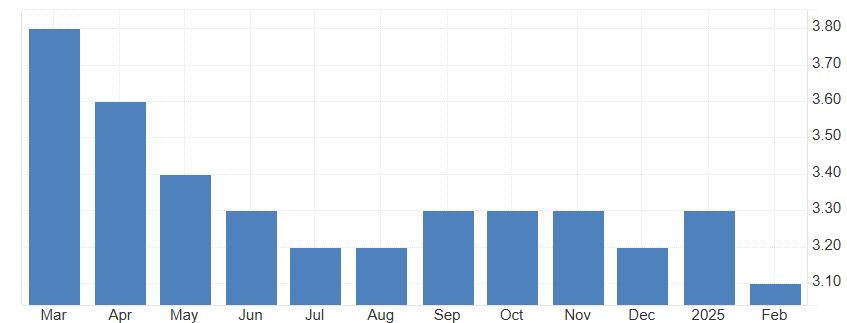

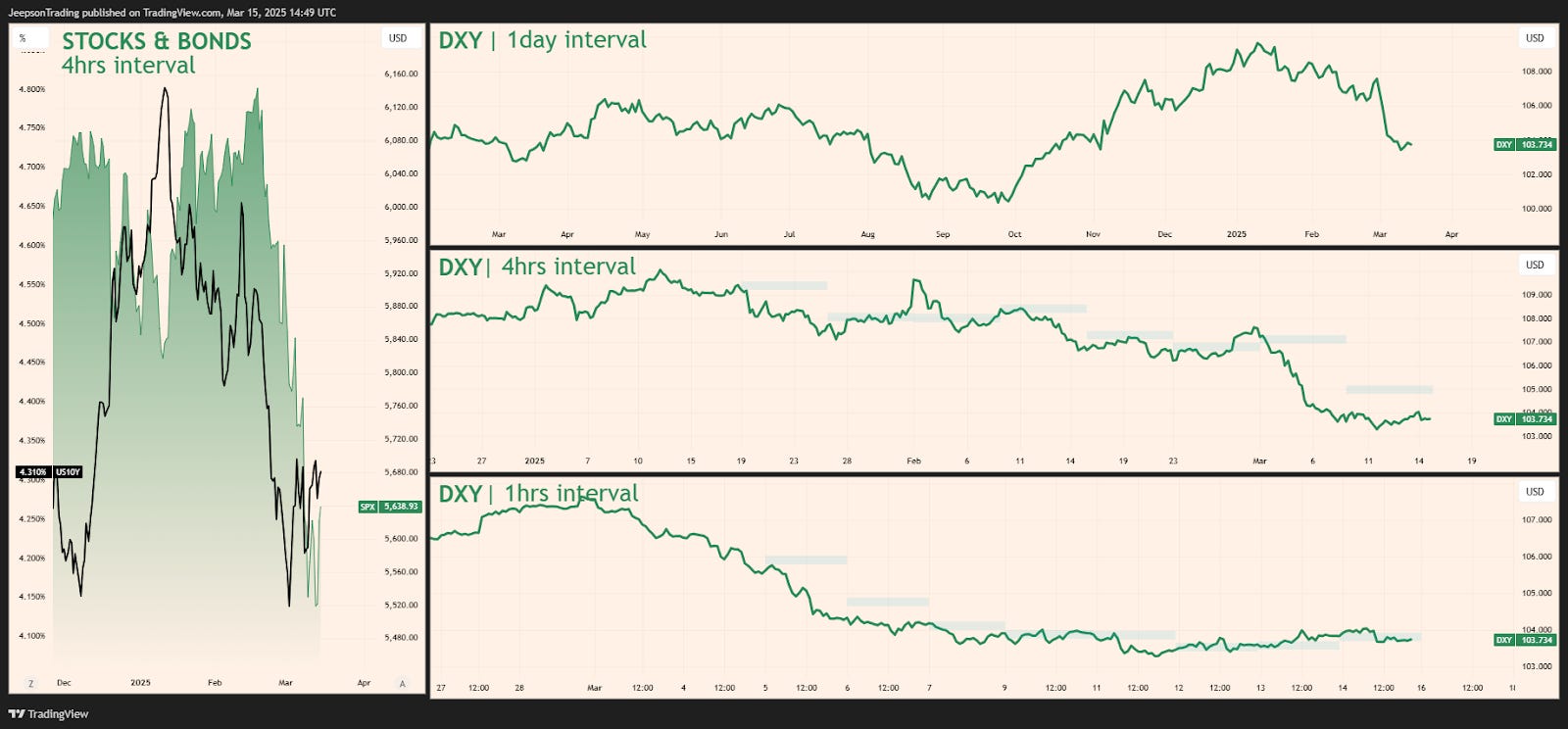

The latest data presents a mixed picture for your trading decisions. Inflation has cooled to 2.8% in February, down from 3% in January, showing progress toward the Fed's 2% target. However, unemployment has ticked up to 4.1%, and job creation is slowing with only 151,000 positions added in February. The S&P 500 entered correction territory on March 13, down 10% from its February peak, reflecting concerns about the administration's policies. Meanwhile, the US Dollar Index stands resilient at 103.77 and is forecast to strengthen to 104.17 by quarter's end, potentially reaching 104.95 within a year. This dollar strength reflects both relatively high interest rates and the currency's safe-haven appeal amid global uncertainties.

Aggressive Policy Implementation Reshapes Economic Landscape Since Inauguration

Looking back over the past seven months, the economic environment has undergone dramatic shifts. After initiating a gradual easing cycle with a rate cut in September 2024, followed by additional reductions through December totalling 100 basis points, the Federal Reserve has since paused amid policy uncertainty.

Everything changed following Trump's election victory and January 2025 inauguration. His administration has wasted no time implementing an ambitious agenda, beginning with executive orders on February 1 imposing significant tariffs on major trading partners (25% on Canada and Mexico, an additional 10% on China). These actions have triggered retaliatory measures, with Canada imposing 25% tariffs on $155 billion of US imports, creating supply chain disruptions throughout North America.

The DOGE initiative under Elon Musk has moved aggressively to restructure government operations. Federal employees were offered a "deferred resignation" scheme, and by March, significant workforce reductions had occurred. Around 1,300 CDC employees were laid off in February, including all first-year officers of the Epidemic Intelligence Service. Additionally, 168 NSF employees were fired, with plans to reduce that workforce by 25-50%.

The past seven weeks have been particularly tumultuous for markets. Perhaps most dramatic has been the administration's approach to foreign aid, with Musk bluntly stating "We're shutting it down" regarding USAID with Trump's agreement. By March 10, Secretary of State Rubio announced the cancellation of approximately 5,200 of 6,200 USAID programs, creating diplomatic tensions with aid recipients.

These policies have faced significant judicial pushback, with multiple federal judges ruling against various executive orders. The federal funding freeze affecting thousands of programs has sparked legal challenges, with judges ordering the administration to restore funding in some cases.

Despite these disruptions, inflation has improved more than expected, with February's annual core inflation rate falling to 3.1% - the lowest since April 2021. However, consumer confidence has suffered, with the Michigan Consumer Sentiment index falling to a disappointing 57.9 in preliminary March readings.

Limited Rate Cuts and Continued Trade Tensions Will Shape Dollar's Path Forward

Looking ahead to the next seven months, you should prepare for a measured, data-dependent approach from the Federal Reserve. Current market expectations suggest just two to three 25-basis-point rate cuts for all of 2025, with the next cut not fully priced in until July. This represents a much slower pace than markets anticipated just a few months ago.

For your immediate trading decisions, several key events deserve your attention. The March 19 FOMC meeting will almost certainly result in unchanged rates as officials continue evaluating the impact of the administration's policies. Watch Chair Powell's press conference carefully for signals about how the Fed views the balance of risks between inflation and growth concerns.

In the coming weeks, key data releases include retail sales on March 17, building permits on March 18, final Q4 GDP on March 27, PCE inflation on March 28, and the March employment report on April 4. Each of these will provide crucial information about whether the economy is maintaining momentum amid policy shifts.

The implementation of tariffs creates a significant complication for both monetary policy and dollar valuation. The one-month pause on tariffs for Canada and Mexico ends on April 2, potentially leading to further escalation if negotiations fail. While tariffs typically push prices higher, potentially slowing the disinformation process, they could also dampen economic growth if they reduce trade volumes.

Economic growth is forecast at approximately 2% annually for 2025 as the effects of tariffs weigh on export volumes and domestic investment. Inflation is projected to trend lower toward the Fed's target of 2%, while unemployment may rise slightly due to federal workforce reductions and slower job creation.

For your forex trading strategy, this environment creates a complex dollar outlook. The competing forces of relatively high interest rates (supporting the dollar) versus policy uncertainty and potential growth concerns (weighing on the currency) will likely create trading opportunities in the coming months. While forecasts suggest continued dollar strength, with the index rising to 104.17 by the end of Q1 and 104.95 in 12 months, you'll want to watch carefully for any shifts in Fed rhetoric that might signal a change in the expected rate path.

The risk-off market environment is likely to persist, with safe-haven currencies potentially outperforming during periods of heightened tension. Gold is expected to remain elevated as geopolitical risks persist, having reached historic highs near $3,000 per ounce as investors seek stability amid uncertainty.

Sources

Federal Reserve, Trading Economics, U.S. Bureau of Labor Statistics, Congressional Budget Office, Reuters, Bloomberg, CFTC Commitments of Traders Report, Forbes, ING Think, Brookings Institution, Investopedia, TradingView, The New York Times, Committee for a Responsible Federal Budget.