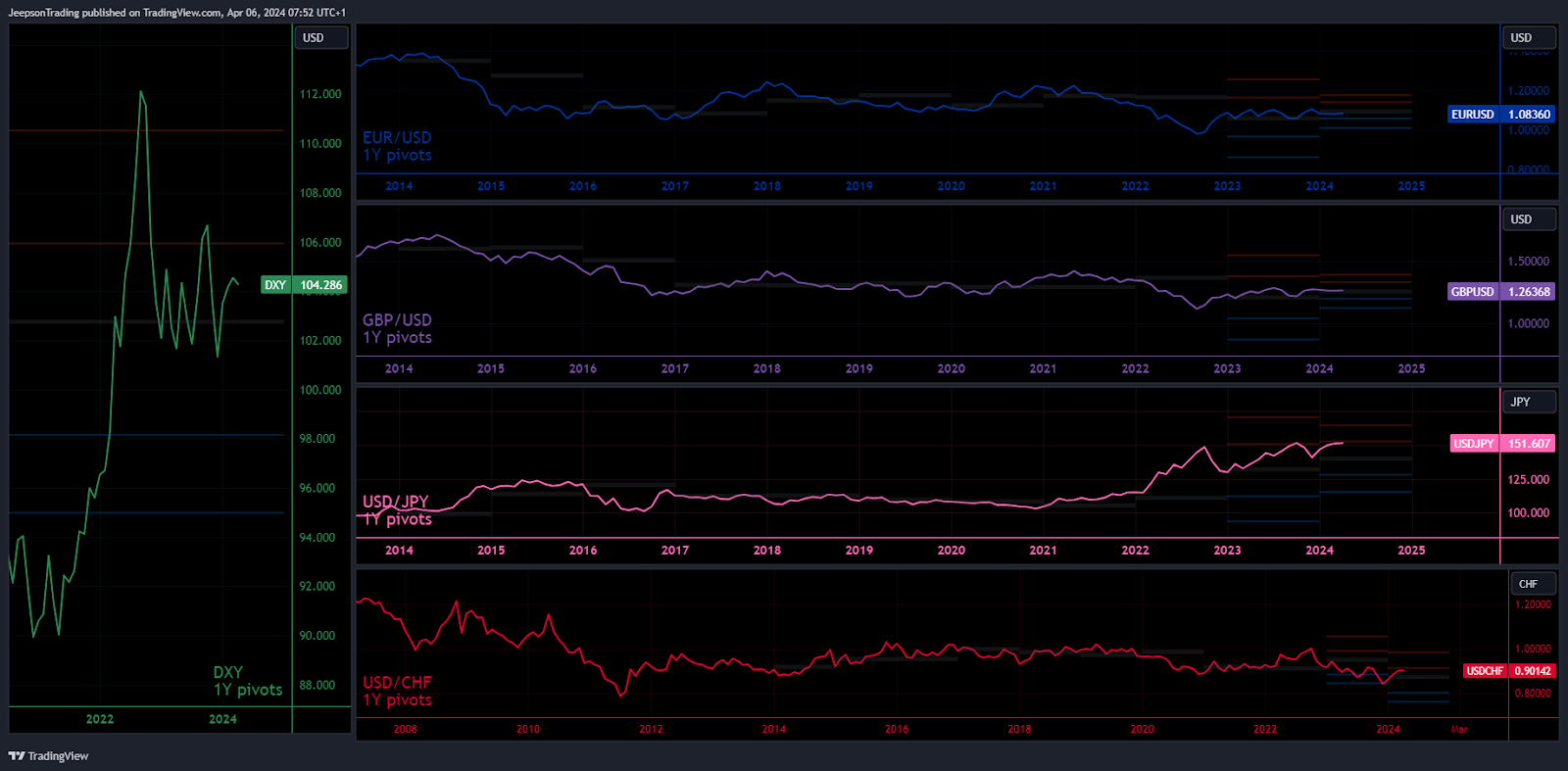

Major Currencies Fundamental Analysis: Dollar Navigates Mixed Signals, Euro Faces Headwinds, Sterling's Path Hinges on Inflation, Yen's Balancing Act

Saturday, April 6, 2024 (Week 14)

Saturday, April 6, 2024 (Week 14): The US dollar navigates a mixed landscape of robust labour markets, persistent inflation, and anticipated Fed rate cuts. The euro faces headwinds amid growth concerns and a dovish ECB outlook, while sterling's path hinges on the UK's inflation fight and growth prospects. Japan's yen seeks balance as the BoJ cautiously normalises policy amid economic recovery.

Economic Performance and Fed Outlook Shape Dollar's Path

The US economy in March and early April 2024 presented a mixed picture, with a resilient labour market and moderating yet elevated inflation. Nonfarm payrolls expanded by an impressive 303,000 jobs in March, surpassing the average monthly gain of 231,000 over the previous 12 months. This robust job growth was accompanied by an unexpected dip in the unemployment rate to 3.8%, underscoring the labour market's resilience. However, inflationary pressures, while moderating, remained elevated, with the Consumer Price Index (CPI) rising 3.2% year-over-year in March. This persistent inflation could pose challenges for the Federal Reserve's efforts to achieve price stability.

On the consumer front, retail sales grew a modest 0.6% in February, suggesting a potential cooling in consumer demand, a key driver of economic growth. The housing market presented a mixed picture, with building permits and housing starts surging, indicative of a recovery in the sector. However, construction spending contracted for the second consecutive month, tempering optimism about the housing market's recovery.

In the external sector, the US trade deficit widened to $68.9 billion in February, the highest level in 10 months. This spike was driven by a rise in imports outpacing export growth, potentially reflecting a slowdown in global demand for US goods and services. Business indicators were also mixed, with factory orders rebounding by 1.4% in February after a sharp decline in January. However, the ISM Manufacturing Purchasing Managers' Index (PMI) contracted for 16 consecutive months until March when it finally returned to expansionary territory, indicating a potential turnaround in the manufacturing sector.

Looking ahead, the US economy is projected to grow at a rate of 2.1% in 2024, according to the Federal Reserve's latest projections. However, moderating consumer spending, driven by factors such as higher borrowing costs and inflationary pressures, could pose headwinds to economic growth. Additionally, the widening trade deficit could further weigh on GDP growth if it persists.

Amid these economic crosscurrents, the Federal Reserve maintained a cautious stance, keeping the federal funds rate unchanged at 5.25%-5.5% in its March meeting, marking the fifth consecutive meeting without a rate hike. Policymakers signalled their intention to implement three interest rate cuts in 2024, followed by gradual reductions in 2025 and 2026, aiming to support economic recovery while maintaining a watchful eye on inflationary pressures.

The outlook for the US dollar's value is likely to be influenced by the evolving economic landscape and the Federal Reserve's policy stance. In the near term, the resilient labour market and elevated inflation could support the dollar's strength against other major currencies, as traders anticipate the Fed's resolve in maintaining a hawkish stance. However, if economic growth moderates as projected and inflationary pressures ease, the anticipated interest rate cuts could gradually weaken the greenback against its counterparts.

Forex traders should closely monitor a range of economic indicators, including employment data, inflation reports, retail sales figures, and trade balances, as these will shape the Fed's future policy decisions and, consequently, the dollar's value. Additionally, geopolitical developments, such as the ongoing Russia-Ukraine conflict and tensions in the Middle East, could impact global risk sentiment and influence currency flows.

Euro Confronts Growth Concerns and Dovish ECB Outlook

The Euro Area economy exhibited mixed signals in recent months, with some indicators pointing to resilience while others raised concerns about the growth trajectory. In the first quarter of 2024, GDP growth is expected to be a modest 0.2%, reflecting the ongoing challenges posed by high inflation, record borrowing costs, and weak external demand.

Inflation moderated in March, with the headline rate declining to 2.4% year-over-year, marking a 28-month low. Core inflation, which excludes volatile food and energy prices, also cooled to 2.9%. However, services inflation remained elevated at 4.0%, underscoring the persistence of underlying price pressures. The labour market remained robust, with the unemployment rate holding steady at 6.5% in February, matching January's revised figure and slightly lower than the previous year. Employment growth accelerated to 0.3% in the fourth quarter of 2023, providing some leeway for the European Central Bank (ECB) to maintain restrictive interest rates.

On the trade front, the Euro Area posted a trade surplus of €11.4 billion in January 2024, a significant improvement from the previous year's deficit. However, consumer spending showed signs of weakness, with retail trade volume increasing by a modest 0.1% in January compared to the previous month. Looking ahead, the ECB has revised its growth projection for 2024 downward to 0.6%, indicating subdued economic activity in the near future. However, a gradual recovery is anticipated, with growth projected to reach 1.5% in 2025 and 1.6% in 2026, supported initially by consumption and later by investment.

In its March meeting, the European Central Bank (ECB) maintained its key interest rates at their current levels, with the main refinancing operations rate remaining at 4.5% and the deposit facility rate at 4%. This decision comes as policymakers grapple with the challenge of balancing concerns over a potential recession with persistently high underlying inflation. The ECB has revised its inflation projections, with the headline rate expected to average 2.3% in 2024, 2.0% in 2025, and 1.9% in 2026. Core inflation is projected to be 2.6% in 2024, 2.1% in 2025, and 2.0% in 2026, suggesting a gradual decline towards the ECB's 2% target in the medium term.

The outlook for the euro currency is closely tied to the ECB's monetary policy decisions and the broader economic performance of the Euro Area. In the near term, the ECB's decision to maintain high interest rates could lend some support to the euro, as traders anticipate a hawkish stance from the central bank in its efforts to control inflation. However, growing concerns over the region's growth prospects and the potential for a more accommodative monetary policy stance in the future could weigh on the euro's value.

Forex traders should closely monitor key economic indicators, such as inflation reports, employment data, wage growth figures, and consumer spending metrics, as these will shape the ECB's policy outlook and, consequently, the euro's performance against other major currencies. Additionally, developments in the Euro Area's trade balance and external competitiveness could influence the currency's value.

Sterling's Trajectory Tied to Inflation Fight and Growth Prospects

The UK economy exhibited mixed signals in recent months, reflecting the challenges posed by persistent inflationary pressures and subdued growth prospects. In the first quarter of 2024, GDP growth is expected to be a modest 0.2%, following a 0.3% contraction in the previous quarter. The services sector, particularly retail trade, human health, and education, drove the rebound, while construction grew by 1.1% and industrial output fell by 0.2%.

Inflation moderated in February, with the annual CPI rate easing to 3.4%, the lowest in nearly two-and-a-half years. However, core inflation remained elevated at 4.5%, underscoring the persistence of underlying price pressures. On the labour market front, the unemployment rate edged up to 3.9% in January, while regular pay growth (excluding bonuses) slowed to 6.1% year-over-year, the lowest since October 2022.

Consumer spending showed signs of weakness, with retail sales growth slowing to 1% year-over-year in February, the lowest since August 2022 and below the 4% consumer inflation rate. However, the housing market exhibited some resilience, with mortgage approvals rising to 60.4 thousand in February, the highest level since September 2022, supported by a sharp fall in interest rates on newly drawn mortgages.

The Bank of England maintained the Bank Rate at 5.25% in its March 2024 meeting, the highest level since 2008. The Monetary Policy Committee voted 8-1 in favour of keeping rates unchanged, with one member advocating for a 25 basis point decrease. This decision deviated slightly from market expectations of a more hawkish 7-2 vote. The current restrictive monetary policy stance aims to address persistent inflationary pressures while supporting growth and employment. The Bank of England's decision to maintain the interest rate at 5.25% reflects a cautious approach, as policymakers await clearer signals that inflationary pressures have subsided before considering rate cuts.

The outlook for the British Pound is closely tied to the Bank of England's monetary policy decisions and the broader economic performance of the UK. In the near term, the central bank's decision to maintain high interest rates could lend some support to the Pound, as traders anticipate a hawkish stance from the Bank of England in its efforts to control inflation. However, growing concerns over the UK's growth prospects and the potential for a more accommodative monetary policy stance in the future could weigh on the Pound's value.

Forex traders should closely monitor key economic indicators, such as inflation reports, employment data, wage growth figures, consumer spending metrics, and trade data, as these will shape the Bank of England's policy outlook and, consequently, the Pound's performance against other major currencies.

Yen Seeks Balance as BoJ Cautiously Normalises Policy

Japan's economy exhibited signs of recovery in recent months, albeit with some mixed signals. In the fourth quarter of 2023, the economy expanded by 0.4% on an annualised basis, supported by a strong rebound in business spending and positive net trade contributions. However, private consumption remained weak due to inflationary pressures and sluggish wage growth.

Inflation rates continued to rise in February 2024, with the core consumer price index (CPI) and the overall inflation rate both reaching 2.8% year-over-year, accelerating from the previous month and exceeding the Bank of Japan's (BoJ) 2% target for 23 consecutive months. Producer prices also increased by 0.6% year-over-year in February, marking the highest producer inflation since October 2023.

In March 2024, the Bank of Japan (BoJ) raised its key short-term interest rate to around 0% to 0.1% from -0.1%, ending eight years of negative interest rates. This move, which matched market expectations, came as inflation had exceeded the central bank's 2% target for over a year and the largest companies in Japan had agreed to raise salaries by 5.28%, the most significant wage hike in more than three decades. The BoJ also terminated yield curve control for 10-year government bonds and discontinued purchases of ETFs and Japan real estate investment trusts (J-REITs). Furthermore, the central bank announced plans to gradually reduce the pace of corporate bond buying before fully stopping it in about a year.

The outlook for the Japanese yen is closely tied to the BoJ's policy decisions and the broader economic recovery. In the near term, the yen has appreciated, touching its highest levels in two weeks, as Japanese authorities ramped up verbal interventions to stem sharp yen declines. Finance Minister Shunichi Suzuki repeated warnings that the government would take appropriate measures to support the currency, while BoJ Governor Kazuo Ueda stated that the central bank could ""respond with monetary policy"" if the yen's weakness affected the economy. However, the yen's recent weakness came amid speculations that BoJ monetary policy will stay accommodative for some time despite the recent pivot against negative rates. If the BoJ maintains a cautious approach to tightening monetary policy, the yen could face further downward pressure.

Forex traders should closely monitor Japan's inflation data, wage growth, and the BoJ's policy statements, as they can have a significant impact on the yen's value. Higher inflation and the prospect of further monetary policy normalisation may support the yen, while a more cautious approach from the BoJ could lead to a weaker currency.

In conclusion, the forex market faces a complex interplay of economic, political, and geopolitical factors. The US dollar navigates a mixed landscape of robust labour markets, persistent inflation, and anticipated Fed rate cuts. The euro faces headwinds amid growth concerns and a dovish ECB outlook, while sterling's path hinges on the UK's inflation fight and growth prospects. Japan's yen seeks balance as the BoJ cautiously normalises policy amid economic recovery. Traders must remain vigilant, closely monitoring key indicators, central bank communications, and global developments to navigate potential currency fluctuations in the coming weeks. By staying informed and adaptive, forex traders can effectively manage risks and capitalise on opportunities in this dynamic market environment.

Gavin Pearson

Retail trader since 2008

Specialises in forex

Funded account from the 5ers.com

Member of the eToro Popular Investors Program

Regular contributor to FXStreet.com analysis and education pages

Returned 27% in 2022 and -2.7% in 2023

Exclusively forex focused

Copy Trading available at eToro

Disclaimer

Past performance is not indicative of future results

Trading involves risk, and you could lose money

-end-