US dollar rebound stalls as CPI reports loom, China retail sales data due

Market Analysis for Week Number 46 2023

US dollar rebound stalls as CPI reports loom, China retail sales data due

DERBYSHIRE UK, Nov 12, 2023, Week 46. The dollar has been recovering from its dips as Fed policymakers push back against the market narrative that they are at peak rates. This week's key focus is the CPI reports due out for the US, UK, and EA, all of which are expected to show declines. This could lead to traders reassessing central bank pivots away from the hawkish stance that has been in place for the past 18 months.

Recent concerns of a global slowdown may be allayed by Chinese retail sales data, which is expected to show an increase from 5.5% to 7.1%.

Trading involves a possibility of losing money therefore all decisions in market speculation are undertaken at your own financial risk.

Economic Events of Interest

This shows the market expectations at time of writing, monitor for deviations upon release as these can have significant impacts on market moves.

Tuesday, November 7th

CN Balance of Trade: Was lower than forecast, lower than previous

Wednesday, November 8th

EA Retail Sales: Was lower than expected but higher than previous

Thursday, November 9th

CN CPI: Was lower than previous and deflation expected

Fed Chair Powell Speech: “The biggest mistake remains not getting rates high enough”

Friday, November 10th

UK GDP: Was better than expected but lower than previous

ECB President Lagarde Speech: “If Kept Long Enough, Rates Will Take Us To 2%”

US Michigan Consumer Sentiment: Was much lower than previous

Monday, November 13th

Tuesday, November 14th

0800 (GMT) GB Unemployment rate: slightly higher than previous expected

0800 (GMT) GB Average earnings: lower than previous expected

1100 (GMT) EA GDP: small contraction expected, second estimate

1100 (GMT) EA ZEW Sentiment: better than previous expected

1430 (GMT) US Inflation rate: slower than previous expected (3.3 vs 3.7)

Wednesday, November 15th

0200 (GMT) CN Industrial Production: same as previous

0200 (GMT) CN Retail Sales: Significant increase expected

0200 (GMT) CN Unemployment rate: Same as previous expected

0800 (GMT) GB Inflation rate: far slower expected (4.9 vs 6.7)

1100 (GMT) EA Balance of Trade: Much better than previous expected

1430 (GMT) US PPI: lower than previous expected

1430 (GMT) US Retail Sales: Much lower than previous expected

Thursday, November 16th

1230 (GMT) ECB Lagarde speech:

Friday, November 17th

0800 (GMT) GB Retail Sales: Much lower than previous expected

0930 (GMT) ECB Lagarde speech:

1100 (GMT) EA Inflation rate: Far slower expected (2.9 vs 4.3)

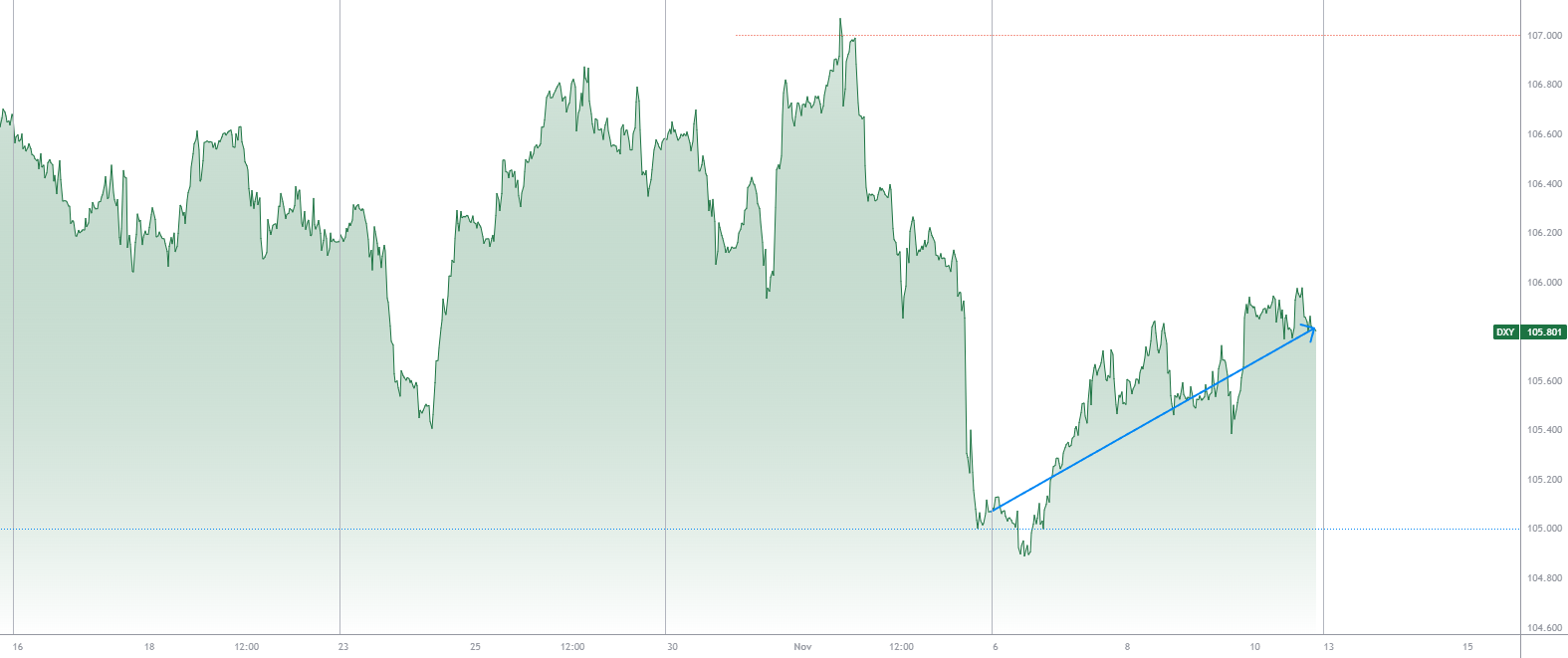

Dollar Recovers Some Ground

CME Group 30-Day Fed Fund futures:

90% in favour of a hold at the December meeting, down from 95% last week

Dollar value last week signals a steady sentiment

The dollar strengthened against other currencies, the US stock market rose slightly, and the yield on US 10Y bonds remained relatively unchanged in week 45 (WN45), suggesting a stable market sentiment.

The steady sentiment was mostly influenced by the Fed reversing some of its previous dovish-sounding rhetoric, as well as mixed corporate earnings results. Investors remain cautious as they await further guidance from the Fed on its future monetary policy plans.

Macroeconomics

The US economy continued to grow strongly in the third quarter of 2023, but there are some signs that it is cooling. Inflation remains elevated, but there are also some signs that it is moderating. Overall, the US economy is in good shape, but there are some risks to the outlook.

The Federal Reserve has a difficult task ahead of it: to bring inflation down to its target without causing a recession. The Biden administration can also play a role in supporting the economy by investing in growth drivers and providing incentives to businesses.

Next week, new readings on CPI, PPI, and Retail Sales are expected to show economic conditions are slowing. This could strengthen the case that the Fed is indeed at the peak rate and undo the desired pushback by the Fed. Paid-subscribers can view the Dollar Trade Plans here.

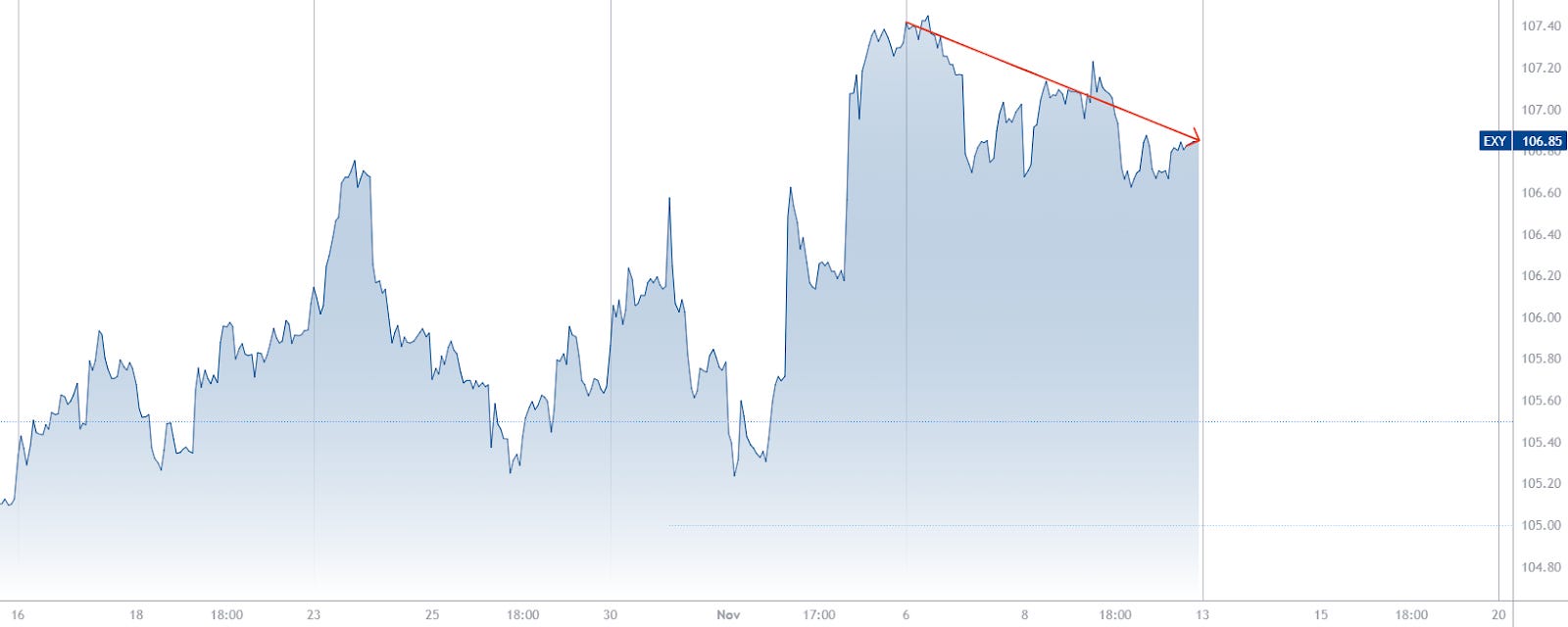

Euro retraces to the downside

Euro value last week signals a bearish sentiment

The euro lost value against a basket of currencies, the German stock market was flat, and the yield on German 10Y bonds rose slightly in week 45 (WN45), indicating a bearish market sentiment.

This bearish mood was mostly influenced by comments from the ECB, who softened its hawkish stance with ECB President Christine Lagarde indicating that a 4% deposit rate should be sufficient to control inflation. This was somewhat countered by ECB official Robert Holzmann who commented about being ready to raise rates, showing that policymakers need to strike a careful balance, likely leading to a wait-and-see approach.

Market expectations suggest the ECB could cut rates by 95 basis points by end-2024, suggesting that investors believe the ECB will eventually become more dovish as the economy slows down.

Macroeconomics

The European Central Bank (ECB) held interest rates steady at 4.5% in October. The eurozone economy shrank 0.1% in Q3 due to high energy prices, supply issues, and the war in Ukraine. Inflation in the eurozone eased to 2.9%, which may soften the ECB’s hawkishness and help to avert a recession.

Next week, new readings on GDP, Economic Sentiment, Balance of Trade, CPI are expected to show a mixed outlook. ECB president Lagarde is scheduled to speak and will be worth monitoring to see if the tone continues to introduce dovish rhetoric regarding future monetary policy. CPI on Friday will be the focus. Paid-subscribers can view the Euro Trade Plans here.

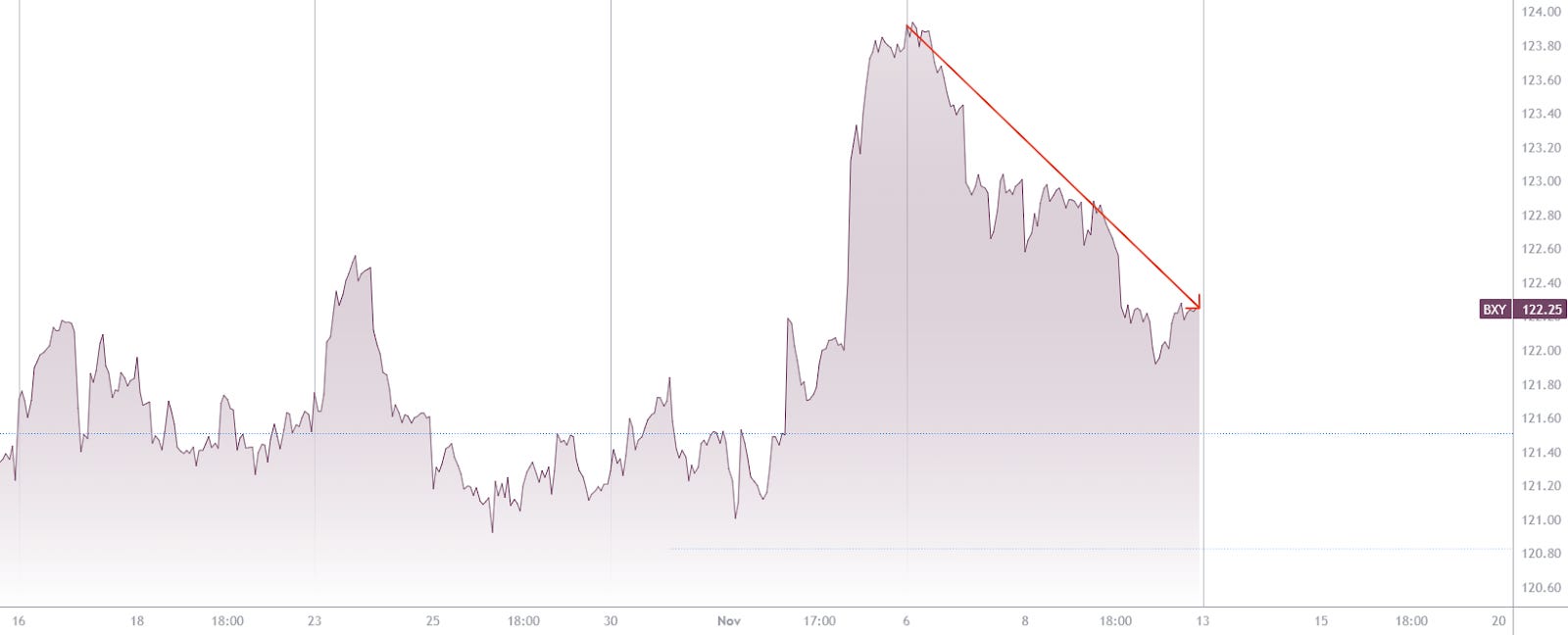

Pound Takes a Tumble

Euro value last week signals a bearish sentiment

The pound weakened against other currencies, the UK stock market fell, and the yield on UK 10Y bonds edged higher in week 45 (WN45), indicating a bearish market sentiment.

This bearish mood was mostly influenced by a worsening UK economic outlook, as higher interest rates weighed on growth despite flat third-quarter GDP, which beat expectations of a contraction.

Macroeconomics

The UK economy is slowing, but inflation remains persistently high. The Bank of England is keeping interest rates high to try to bring inflation down, but this is also slowing growth further.

Retail sales declined in September, and the unemployment rate rose. The Bank of England is expected to keep interest rates unchanged at its next meeting, but rates could rise further if inflation does not come down.

The UK economic outlook is uncertain. The Bank of England expects GDP growth to be only 0.9% in 2023, and to rebound to 1.7% in 2024. However, there are risks to the outlook, including the ongoing war in Ukraine, persistently high inflation, and higher interest rates.

The UK government is facing a difficult task: to support the economy and avoid a recession while also bringing inflation down. The government may need to provide financial assistance to businesses and households, and it may also need to invest in growth drivers such as education and infrastructure.

Next week, new readings on labour, CPI and retail sales are expected to show a mixed outlook. CPI will be of most significance and expected to be slowing so any upside surprises will likely cause some volatility. Paid-subscribers can view the Pound Trade Plans here.

Gavin Pearson

Retail trader since 2008

Specialises in forex G7 currencies

Funded account from the5ers.com

Member of the eToro Popular Investors Program

Regular contributor to FXStreet.com analysis and education pages

Returned 27% in 2022 and 5.8% in 2023 H1

Forex focused

Copy Trading available at eToro

Disclaimer

Past performance is not indicative of future results

Trading involves risk, and you could lose money

-end-