US Dollar: Recession Fears, Rate Cut Bets, and Geopolitical Risks

Saturday, September 07, Week 36

The US dollar has experienced significant volatility in recent weeks, driven by a combination of factors including shifting expectations for Federal Reserve rate cuts, mixed economic data, geopolitical tensions, fiscal concerns, and monetary policy.

The Federal Reserve is widely expected to begin cutting interest rates at its September meeting, but the exact timing and magnitude of the cuts remain uncertain.

The Impact of Geopolitical Risks on the US Dollar

The ongoing conflict between Israel and Hezbollah has had substantial ramifications for the Middle Eastern currency markets, affecting both supply and demand dynamics. The disruption of economic activity in the region as a result of the conflict has led to a decrease in exports and an increase in the demand for imports. This imbalance in trade has resulted in the depreciation of currencies within the affected countries. Consequently, investors have shifted their focus towards alternative currencies, perceiving the US dollar as a reliable and stable investment option in the midst of regional instability.

Geopolitical Risks on the Horizon

In the near term, the focus will be on the situation in the Middle East. The conflict between Israel and Hezbollah shows no signs of abating, and the potential for a wider regional conflict remains a significant risk. Any escalation of the conflict could trigger a flight to safety, boosting the US dollar and other safe-haven assets.

The situation in Libya will also be closely watched. The new unity government faces significant challenges in stabilising the country and rebuilding its economy. Any setbacks in this process could lead to renewed conflict, disrupting oil production and exports and impacting global energy prices.

The trade war between the US and China is another key risk to watch. The two countries are expected to continue their negotiations, but the potential for a breakthrough remains uncertain. Any further escalation of the trade war could dampen global economic growth and trigger risk aversion, impacting the US dollar and other financial markets.

In the medium term, the focus will shift to the US presidential election in November. The outcome of the election could have significant implications for US foreign policy and the global geopolitical landscape. A victory for a candidate who favours a more isolationist approach could lead to a weakening of the US dollar and a shift in global power dynamics.

""The conflict between Israel and Hezbollah has the potential to destabilise the entire Middle East, with far-reaching consequences for global energy markets and the global economy. The situation is highly fluid, and the potential for escalation remains high."" - Stratfor Worldview

US Fiscal Policy: A Balancing Act Between Spending and Debt

The US fiscal landscape is characterised by a delicate balancing act between addressing pressing needs and managing a growing budget deficit. The Biden administration's significant investments in infrastructure, clean energy, and social programs, coupled with the ongoing economic recovery, have contributed to a widening deficit. The Fiscal Responsibility Act of 2023, enacted earlier this year, aims to address this issue by enacting roughly $1 trillion in savings over the next decade. However, the long-term sustainability of US public finances remains a concern, particularly as interest rates rise and the cost of servicing the debt increases.

The Congressional Budget Office (CBO) projects that the US budget deficit will average 6.1% of GDP over the next decade, significantly higher than the 50-year average of 3.6%. The CBO also projects that the US national debt will reach 118% of GDP by 2033, the highest level since World War II.

The Impact of Recent Events

In the past month, the US fiscal policy landscape has been relatively quiet, with no major legislative changes or policy announcements. However, the market has been closely monitoring the government's spending and revenue projections, as outlined in the US Treasury's budget for fiscal year 2025, for clues about the long-term sustainability of US public finances.

The recent release of the US second-quarter GDP data, showing an annualised growth rate of 3.0%, has provided some reassurance to markets. However, the weaker-than-expected demand at the 10-year US bond auction on August 7th highlighted the fragility of markets in the aftermath of historical volatility. This event, coupled with the ongoing concerns about the US budget deficit, suggests that fiscal policy will remain a key focus for market participants in the coming months.

US Economic Fundamentals

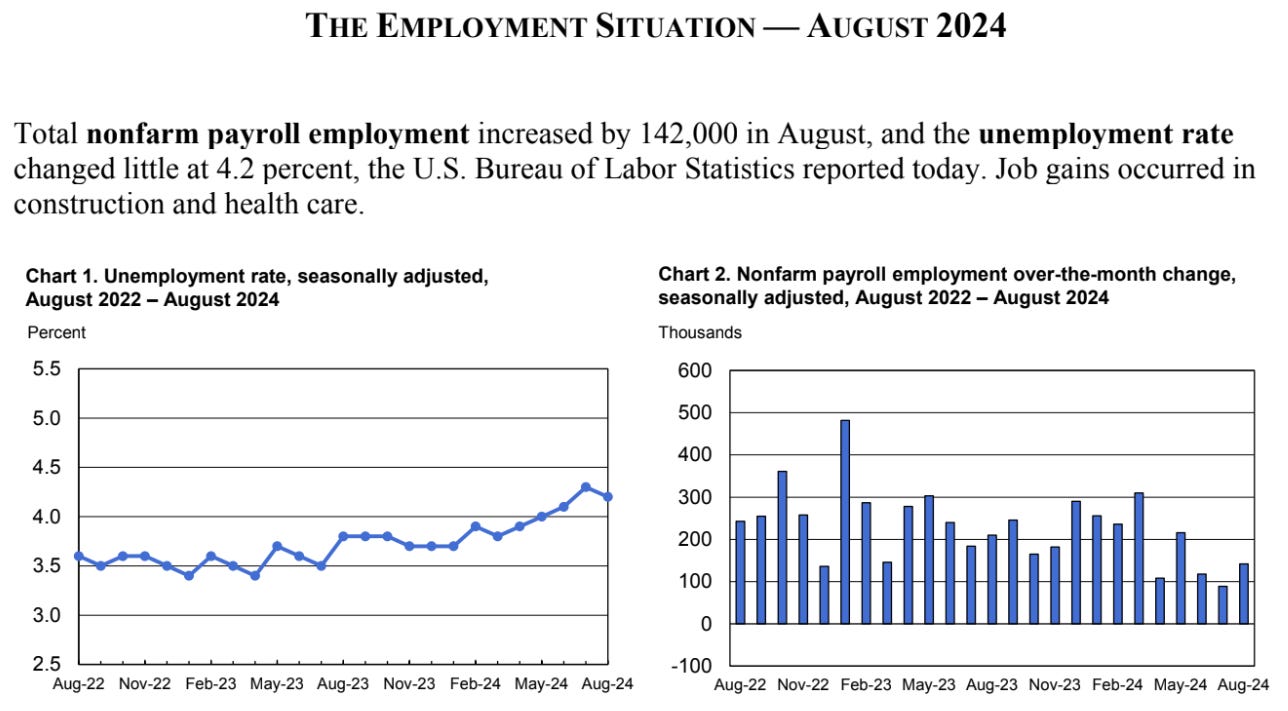

The Employment Situation Report - Bureau of Labor Statistics

In August, the unemployment rate remained at 4.2%, indicating a cooling labour market. Job gains slowed, with the August Non-Farm Payrolls report, published on September 6th, revealing a job creation of 142,000, falling short of market predictions of 160,000. This marked the second consecutive month of job growth below 200,000, suggesting a potential deceleration in labour market growth.

Inflation has shown signs of easing, with the CPI rising 2.9% year-on-year in July, the smallest 12-month increase since March 2021. However, core inflation, which excludes volatile food and energy prices, remained elevated at 3.2% year-on-year in July. The PCE price index, the Fed's preferred inflation gauge, also showed a moderation in inflation, with the headline PCE rising 2.5% year-on-year in July and the core PCE rising 2.6% year-on-year.

The housing market has cooled significantly, with rising mortgage rates and high home prices weighing on affordability. Existing home sales fell for the fourth consecutive month in July, while new home sales rose but remained below their pre-pandemic levels. The Case-Shiller home price index showed that home price growth slowed in June, but prices remained elevated.

Economic Outlook

In the near term, the US jobs report for September and the CPI data for August will provide insights into the health of the labour market and the trajectory of inflation. The trade war between the US and China remains a key factor to watch, as any further escalation could dampen global economic growth and impact financial markets. The potential for a currency board in Libya and the outcome of the US presidential election in November are additional factors that could influence the performance of the US dollar, with potential implications for the currency's strength.

US Monetary Policy: Walking the Path to Rate Cuts

The Federal Reserve is facing a challenging environment as it seeks to balance its dual mandate of maximising employment and maintaining price stability. Inflation, while down from its peak, remains stubbornly high. However, there are strong expectations for a shift towards a more dovish stance in the near-term, with a rate cut widely anticipated at the September FOMC meeting. This expectation is driven by signs of cooling inflation and a moderating labour market.

The Federal Reserve has maintained a restrictive monetary policy stance for over a year, raising interest rates aggressively to combat inflation. The benchmark interest rate in the United States was last recorded at 5.50 percent. However, the recent economic data, particularly the weaker-than-expected July jobs report and the downward revision to non-farm payrolls, has prompted the market to price in a rate cut in September. The market currently expects the Fed Funds Rate to be 5.00 percent by the end of this quarter.

Monetary Policy Developments: The Impact of Recent Events

The most significant monetary policy development in the past month was Chair Powell's speech at the Jackson Hole symposium on August 23rd. In his speech, Powell acknowledged the recent progress on disinflation and the cooling of the labour market. He also signalled that the Fed is prepared to cut interest rates if the economic data warrants it.

"It will take time, however, for the full effects of our ongoing monetary restraint to be realised, especially on inflation." - Chair Jerome Powell, August 25, 2024, Jackson Hole Economic Symposium

The market reaction to Powell's speech was immediate, with the US dollar weakening and US Treasury yields declining. The market is now pricing in a 100% chance of a rate cut in September, with some analysts even predicting a 50 basis point cut.

The US Macroeconomic Outlook: Navigating Uncertainty

The US macroeconomic outlook is currently characterised by a high degree of uncertainty, with the path ahead heavily dependent on incoming economic data and the Federal Reserve's response to those data. While the economy has shown resilience, with solid consumer spending and a robust labour market, persistent inflation and the lagged effects of the Fed's aggressive tightening cycle pose significant risks.

The Path Ahead

In the upcoming month, the US economy is expected to continue expanding, albeit at a slower pace. The labour market is likely to remain strong, supporting consumer spending. However, inflation is expected to remain elevated, albeit with signs of moderation. The Federal Reserve is widely expected to cut interest rates at its September meeting, but the exact timing and magnitude of the cuts remain uncertain.

The short-term risks to the economic outlook are tilted to the downside. The lagged impact of the Fed's aggressive tightening cycle could begin to weigh more heavily on economic activity, increasing the risk of a recession. Additionally, persistent inflation could erode consumer confidence and further dampen spending. The release of the US jobs report for August on September 6th will be crucial for gauging the health of the labour market and assessing the risk of a recession. This report will be particularly important in light of Chair Powell's comments at Jackson Hole, where he emphasized the importance of the labour market in the Fed's policy decisions.

Key Economic Indicators to Watch

The following economic indicators are key to tracking the macroeconomic outlook for the US dollar in the coming month:

CPI: The August CPI report is scheduled for release on Wednesday, September 11th, Week 36. The market expects a 2.60% year-on-year increase in consumer prices. If the actual result is in line with this forecast, it would suggest that inflation is moderating, potentially supporting the case for a Fed rate cut. Lagging indicator.

PPI: The August PPI report is scheduled for release on Thursday, September 12th, Week 36. The market expects a 0.20% month-over-month increase in producer prices. If the actual result is in line with this forecast, it would suggest that producer price inflation is moderating, potentially supporting the case for a Fed rate cut. Leading indicator.

Retail Sales: The August Retail Sales report is scheduled for release on Tuesday, September 17th, Week 37. The market expects a 0.50% month-over-month increase in retail sales. If the actual result is in line with this forecast, it would suggest that consumer spending remains solid, potentially supporting the view that the US economy is not heading towards a recession. Leading indicator.

Industrial Production: The August Industrial Production report is also scheduled for release on Tuesday, September 17th, Week 37. The market expects a 0.10% month-over-month increase in industrial production. If the actual result is in line with this forecast, it would suggest that the manufacturing sector is stabilising, potentially supporting the view that the US economy is not heading towards a recession. Coincident indicator.

Michigan Consumer Sentiment: The preliminary reading for September's Michigan Consumer Sentiment is scheduled for release on Friday, September 13th, Week 36. The market expects a reading of 68. If the actual result is in line with this forecast, it would suggest that consumer confidence remains relatively stable, potentially supporting the view that the US economy is not heading towards a recession. Leading indicator.

FOMC Meeting: The Federal Open Market Committee (FOMC) will meet on Tuesday and Wednesday, September 17th-18th, Week 37. The market expects the Fed to cut interest rates by 25 basis points. If the Fed cuts rates as expected, it would be the first rate cut since March 2023 and could signal the start of a new easing cycle.

Building Permits: The August Building Permits report is scheduled for release on Wednesday, September 18th, Week 37. The market expects a seasonally adjusted annual rate of 1.65 million building permits. If the actual result is in line with this forecast, it would suggest that the housing market is stabilising, potentially supporting the view that the US economy is not heading towards a recession. Leading indicator.

Housing Starts: The August Housing Starts report is also scheduled for release on Wednesday, September 18th, Week 37. The market expects a seasonally adjusted annual rate of 1.33 million housing starts. If the actual result is in line with this forecast, it would suggest that the housing market is stabilising, potentially supporting the view that the US economy is not heading towards a recession. Leading indicator.

Conclusion

The US dollar is currently navigating a complex and uncertain macroeconomic environment. While the economy has shown resilience, with solid consumer spending and a robust labour market, persistent inflation and the lagged effects of the Fed's aggressive tightening cycle pose significant risks. The Federal Reserve's data-dependent approach to monetary policy, the government's fiscal policies, and the evolution of the geopolitical landscape will continue to shape the trajectory of the US dollar in the coming months and years.

Sources

U.S. Bureau of Economic Analysis (BEA)

Federal Reserve

U.S. Census Bureau

Institute for Supply Management (ISM)

National Association of Home Builders (NAHB)

Standard & Poor's

Trading Economics

Financial Juice

Stratfor Worldview