The Euro has a fundamental strength score of -1 (on a scale of -10 to +10) over the coming 7 weeks, with a conviction rating of 3 (on a scale of 0 to 10).

The upcoming pivotal event is the ECB Interest Rate Decision on July 23, 2026 where you should watch for indications of a timeline for subsequent rate hikes to address energy-driven price pressures.

WHAT’S GOING ON: These past few weeks, the Eurozone has been dealing with some turbulent geopolitical waters. Energy shocks from the Middle East conflict and the Strait of Hormuz blockade have kept inflation expectations stoked. That prompted the European Central Bank to deliver its first interest rate hike since 2023, lifting the deposit rate to 2.25 percent on June 11. Softer economic indicators across the region including a contraction in German industrial activity and disappointing Q1 GDP growth have tempered longer-term optimism at the institutional level.

LOOKING AHEAD: Over the next seven weeks, the euro’s performance will be heavily shaped by how the de-escalation in the US-Iran conflict plays out. Recent progress toward peace and the drop in crude oil prices should ease near-term import inflation pressures in the euro area. That gives the ECB some breathing room. This shift is also cooling the hawkish rhetoric that backed yesterday’s surprise rate hike.

Traders will be watching closely to see whether President Lagarde’s team drops its newly adopted hawkish bias or signals further tightening at the July 23 policy meeting. The incoming tier-1 economic data will take center stage. Should the upcoming GDP and CPI prints confirm that the soft landing is slipping into stagflation under the residual weight of high energy costs, euro-area yields may contract and drag the currency down.

If retail sales and loans to companies show resilient domestic credit demand instead, the euro could establish a firm baseline. The narrowing yield spread against US Treasuries will continue to favor USD capital repatriation unless the Federal Reserve signals a policy pivot of its own.

CFTC speculative positioning shows a decline in conviction, pointing to G10 investors scaling back their exposure. In these variable conditions, the euro is poised to navigate a range-bound course, highly sensitive to macroeconomic data surprises and central bank policy convergence.

EURO ZONE FUNDAMENTAL ANALYSIS: Moderately Weak Outlook Amid ECB Hike and Growth Softness

My comprehensive research and analysis of the Eurozone’s macroeconomic indicators yields a Fundamental Strength Score of -1 on a scale of -10 to +10, alongside a Conviction level of 3 on a scale of 0 to 10. This fundamental score reflects a delicate balance between conflicting G10 macro forces. On 1 side, the European Central Bank’s hawkish shift—evidenced by yesterday’s surprise 25-basis-point rate hike to 2.25 percent—provides structural support by widening the Eurozone’s yields.

On the other side, weak tier-1 economic data acts as a heavy anchor. Recent GDP growth missed estimates at 0.3 percent year-over-year, and unemployment ticked up to 6.3 percent, signaling that real-economy momentum is cooling under residual energy-cost headwinds. The Euro was kept from a higher score by these clear domestic growth challenges and a narrowing yield spread. Specifically, the German 10-year Bund yield remains significantly lower than US Treasuries, encouraging capital flows to the greenback.

Conversely, the currency was saved from a lower score by sticky core inflation of 2.5 percent and resilient retail sales, which prevented a full-scale economic contraction. My conviction level is capped at a low 3 due to several factors. First, the mathematical mismatch between our negative economic data run-rate and the ECB’s positive, hawkish policy trajectory creates immediate analytical divergence.

Second, the upcoming 7-week calendar is packed with tier-1 calendar risk events, including the July 23 ECB rate decision and crucial late-July GDP and CPI releases, which could easily disrupt our thesis. While speculative positioning remains slightly net long at 3.58 percent of open interest, it shows a decline in institutional confidence. This lack of clear trend alignment limits our predictive certainty, requiring a highly cautious approach to Euro exposure in these volatile seas.

EUROPEAN UNION GOVERNMENT: Navigating Economic Integration and Geopolitical Winds

The European Union’s political and legislative structure operates under a collective leadership model, primarily driven by the European Commission, currently led by President Ursula von der Leyen, whose 2nd term began in late 2024 and is scheduled to run until 2029. Alongside the Commission, the European Council, representing the heads of state of the member nations, and the European Parliament shape the bloc’s statutory mandate.

The EU’s primary mandate centers on fostering economic integration, ensuring the integrity of the single market, and implementing cohesive regulatory policies across its 27 member states. Currently, Brussels is heavily focused on green energy transitions, digital market regulations—such as enforcing the Digital Markets Act—and securing supply-chain independence amid geopolitical instability.

The government’s policy path is shaped by navigating the fallout of the Middle East conflict, requiring coordinated fiscal responses to mitigate energy bills for households and supporting defensive naval operations in the Red Sea. However, the lack of centralized fiscal authority means the EU must rely on national governments to implement targeted stimulus, resulting in an uneven economic recovery that complicates joint monetary enforcement.

EUROPEAN CENTRAL BANK: Single inflation-focus maintains hawkish stance after historic hike

The European Central Bank, established in 1998 and headquartered in Frankfurt, Germany, is the monetary authority of the Eurozone. The bank is currently led by President Christine Lagarde, whose 8-year non-renewable term began in November 2019 and is set to conclude in late 2027. Unlike the Federal Reserve’s dual-process system, the ECB operates under a singular primary statutory mandate: price stability, defined precisely as maintaining headline inflation at a 2 percent target over the medium term.

While supporting the general economic policies of the European Union is a secondary objective, the bank’s legal charter forces it to prioritize fighting price pressures above growth and employment metrics. Consequently, Euro-area volatility remains highly sensitive to Consumer Price Index data prints. The ECB’s policy trajectory has entered a critical tightening phase.

On June 11, 2026, the Governing Council delivered a surprise 25 basis point rate hike, lifting the benchmark deposit facility rate to 2.25 percent from 2.00 percent, while adjusting the main refinancing and marginal lending rates to 2.40 percent and 2.65 percent respectively. This historic decision, marking the 1st interest rate increase since 2023, was driven by persistent, energy-fueled inflation pressures linked to the Middle East conflict and the Strait of Hormuz naval blockade.

Although some policymakers advocated for holding rates steady to protect the fragile domestic economy, the hawkish faction prevailed, arguing that runaway energy costs risked de-anchoring long-term inflation expectations. In her press conference, President Lagarde emphasized that the central bank remains entirely data-dependent, navigating without a pre-committed rate path.

While the ECB avoided clear forward guidance, markets immediately interpreted the hike as slightly hawkish, pricing in additional tightening before year-end if energy costs remain elevated. However, the policy outlook remains highly uncertain as geopolitical winds shift. The recent progress toward a US-Iran peace deal has triggered a sharp drop in global crude oil prices, which should eventually ease headline inflation pressures.

This de-escalation complicates the ECB’s hawkish stance; if import costs retreat rapidly, further hikes may be paused to prevent unnecessary demand destruction in interest-rate-sensitive sectors such as construction and retail. Over the coming 7 weeks, the ECB will closely monitor whether the June CPI prints confirm a cooling trend or if wage growth, currently running at 3 percent, continues to support domestic services inflation.

Traders must prepare for a cautious hold at the upcoming July 23 meeting, as the Governing Council watches for the pass-through effects of their latest move. The ECB must steer its policy ship through these turbulent global currents, balancing its commitment to the 2 percent inflation anchor against the risk of choking off a weak economic recovery.

EURO ZONE ECONOMY: Subdued growth under energy cost drag and credit stagnation

The Eurozone economy represents 1 of the largest economic blocs in the world, heavily characterized by industrial manufacturing, services, and trade. The region’s primary industries include automotive manufacturing, chemicals, machinery, and financial services. Among the corporate giants driving this activity are Germany’s Volkswagen and Siemens, France’s TotalEnergies and L’Oreal, and the Netherlands’ ASML, which dominates global semiconductor lithography equipment.

The Eurozone’s economic performance relies extensively on its export-oriented model. Key exports include machinery, motor vehicles, pharmaceuticals, and aircraft, with major global trade partners being the United States, the United Kingdom, China, and Switzerland. Conversely, the bloc is highly dependent on imports of raw materials, specifically crude oil, natural gas, and electronic components, with its primary import partners being China, the United States, and the energy exporters of the Middle East.

This heavy reliance on energy imports makes the domestic economy structurally vulnerable to external commodity price shocks. Recent tier-1 data reveals an economy navigating through patchy, low-momentum seas, severely weighed down by the cumulative impact of high energy costs.

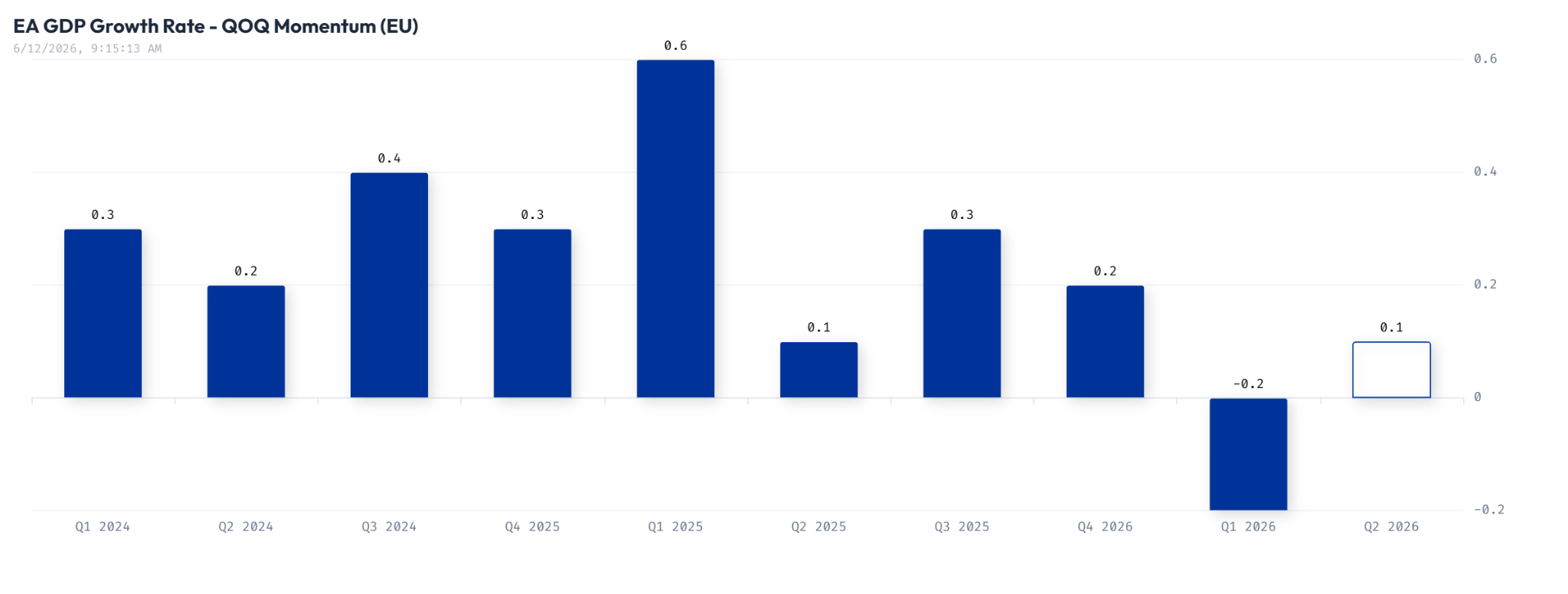

First-quarter GDP growth painted a gloomy picture, expanding by a softer-than-expected 0.3 percent quarter-on-quarter, while a separate reading printed a contraction of negative 0.2 percent, highlighting the uneven recovery across member states. This sluggishness is closely mirrored in industrial production, which fell by a sharp 2.1 percent month-on-month in April as factories struggled with high electricity costs and supply-chain bottlenecks.

The services sector, represented by the HCOB Services PMI, has managed to remain in expansion territory above 50, offering some support to domestic demand, but industrial sentiment remains deeply negative at negative 8, signaling a lack of corporate investment appetite. Consumer activity also shows mixed performance.

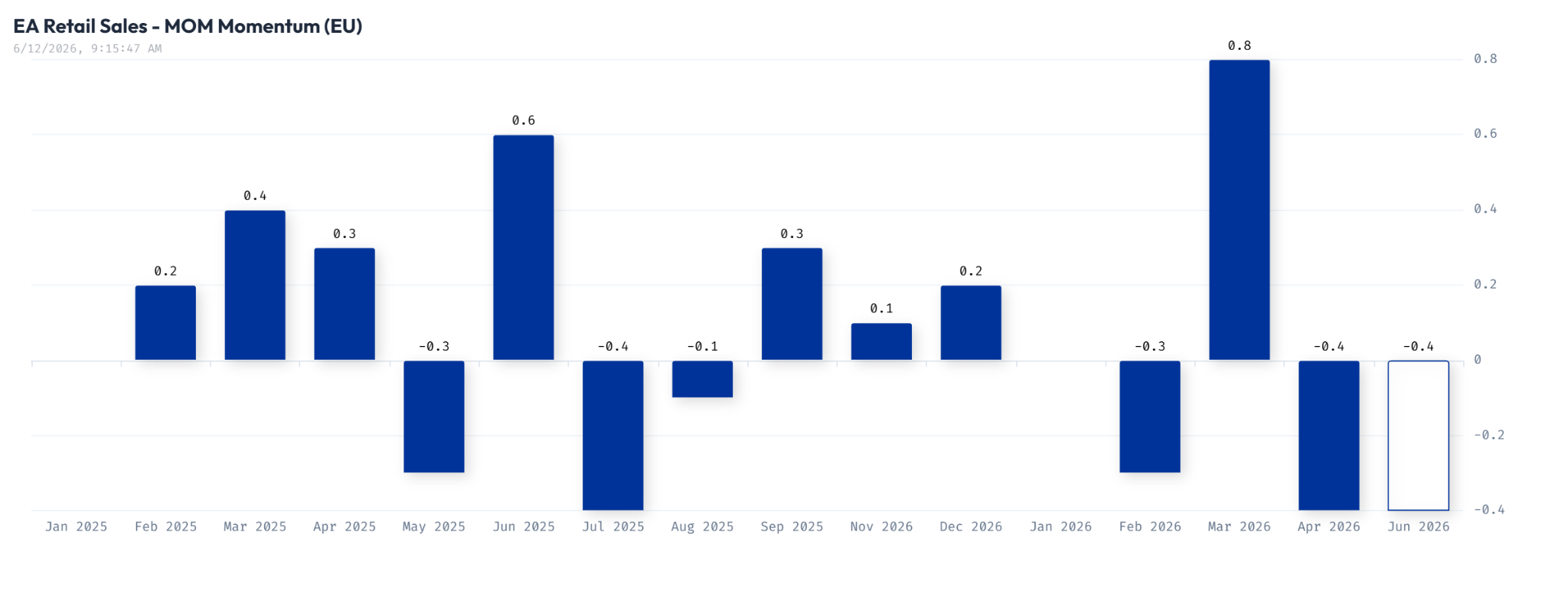

Retail sales grew by 1.2 percent year-on-year in May, beating expectations, but contracted by negative 0.4 percent in the monthly reading, indicating that households are purchasing essential goods while cutting back on discretionary spending. This cautious behavior is driven by cost-of-living pressures and a slightly cooling labor market, with the regional unemployment rate ticking up to 6.3 percent in May from 6.2 percent previously.

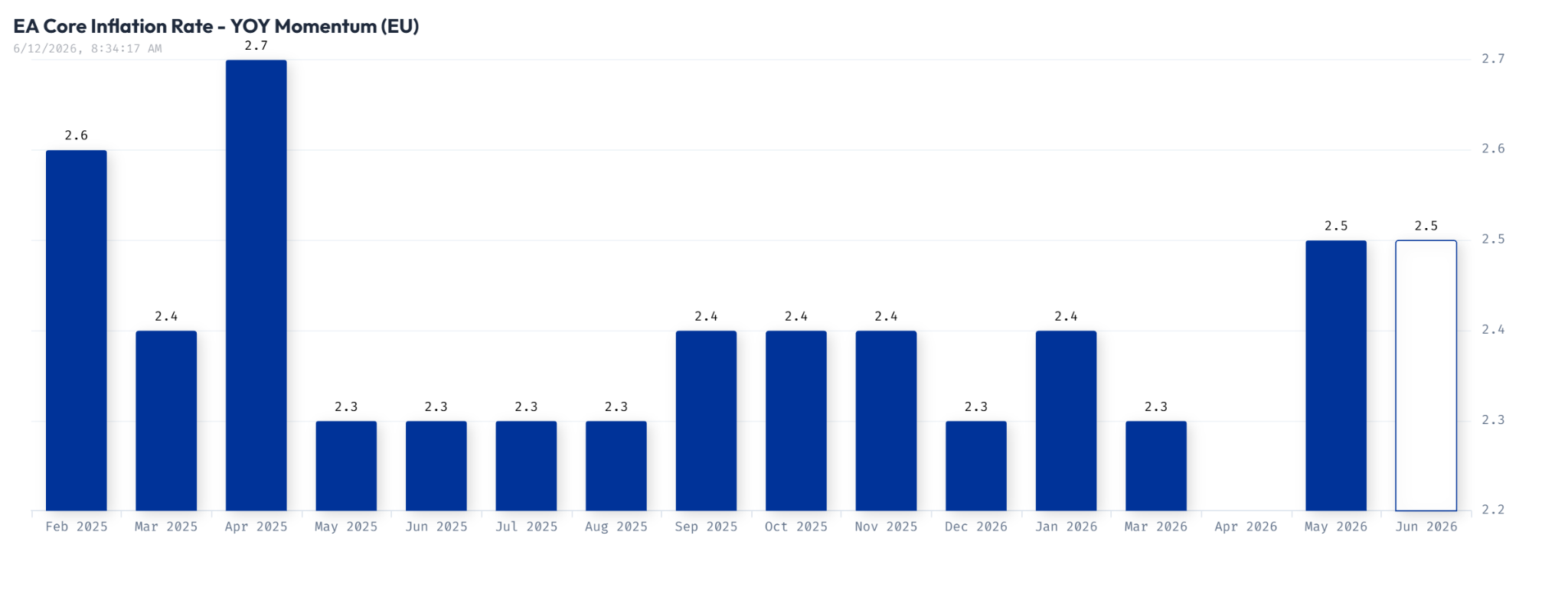

Furthermore, consumer confidence, though recovering slightly, remains depressed at negative 19. Inflationary pressures have proven highly sticky; while headline CPI moderated to 2.6 percent year-on-year in May, core inflation rose to 2.5 percent, driven by services and wage growth of 3 percent.

This persistent inflation forced the ECB to raise rates, which is now expected to weigh on credit creation. Loans to companies and households grew by only 2.9 percent and 3 percent respectively, pointing to credit stagnation. Looking forward, the near-term outlook depends on whether falling oil prices post US-Iran de-escalation can successfully revive industrial activity and lift consumer sentiment, or if high borrowing costs will continue to stall the Eurozone’s economic engine.

EURO ZONE FINANCIAL MARKETS: Debt markets adjust to ECB tightening amid falling stock flows

The financial markets of the Eurozone are highly integrated and represent a core pillar of the global financial system. The primary trading venues are located in Frankfurt (Deutsche Borse), Paris (Euronext Paris), and Amsterdam (Euronext Amsterdam). The benchmark equity indices reflecting regional performance are the Euro Stoxx 50, which tracks 50 blue-chip stocks across the Eurozone, the German DAX, and the French CAC 40.

The sovereign debt market is dominated by the German 10-year government bond (Bund), which serves as the risk-free reference rate and benchmark for European fixed income. Due to the lack of a centralized Eurozone Treasury, peripheral countries like Italy, Spain, and Greece issue their own sovereign debt, with the spread between their yields and the German Bund serving as a key indicator of regional risk sentiment and fiscal cohesion.

The commodity markets are heavily focused on natural gas (traded via the Dutch TTF) and refined petroleum products. Recent performance in Euro-area financial markets has been shaped by the collision of geopolitical tensions and central bank tightening.

Equity markets faced significant headwinds in May and early June, with the German DAX and Euro Stoxx 50 suffering losses as rising oil prices raised inflation fears and squeezed corporate profit margins. However, the sudden de-escalation of US-Iran strikes on June 11 triggered a classic risk-on rotation, prompting a sharp rebound in tech and cyclical shares, while Brent crude and gas prices tumbled.

In the fixed income arena, sovereign yields surged in anticipation of the ECB’s June 11 rate hike. The benchmark German 10-year Bund yield climbed to 3.07 percent before retracing slightly to 3.03 percent following the decision. This has kept the yield spread against US Treasuries wide, with 10-year US paper offering a yield of 4.47 percent, a 144 basis point advantage that continues to drain capital from European debt.

Speculative and commercial positioning, extracted from the CFTC Commitment of Traders data as of May 26, 2026, reveals a cautious and defensive posture. Non-commercial large speculators (hedge funds and CTAs) held 223,055 long contracts and 193,629 short contracts in Euro FX futures, resulting in a net long position of 29,426 contracts.

While speculators remain net long, this represents a significant weekly decline of 4,087 net positions, as shorts grew more rapidly than longs. This net long position of only 3.58 percent of total open interest indicates that institutional conviction is rapidly fading, with funds choosing to flatten their exposure ahead of policy meetings. Conversely, commercial hedgers hold a net short position of 66,535 contracts, indicating that multinational corporations are actively hedging their export revenues against Euro appreciation.

Looking ahead, Eurozone financial markets are expected to remain range-bound. Debt markets will continue to digest the ECB’s hawkish rate path, while equity flows will depend on whether lower energy costs can offset the drag of higher borrowing costs.

Gavin Pearson has been studying the currency markets as a retail trader for twenty years.

Fundamental Analysis pages to bookmark…

DISCLAIMER: This site is informational only, NOT financial advice. Trading involves risk, and you could lose money.